A lazy portfolio is a low-maintenance investment portfolio built around a small number of broad holdings and a simple review rule. Its usefulness depends less on the label and more on what the holdings actually create: asset mix, overlap, concentration, rebalancing behavior, time-horizon fit, and risk-capacity fit.

The structure is meant to reduce unnecessary activity, not remove judgment. A simple portfolio still needs checks for what it owns, how much each part controls, whether different funds repeat the same exposure, and whether drift has changed the investor’s intended risk profile.

What a lazy portfolio is

Definition: A lazy portfolio is a simple portfolio structure that uses a limited number of broad funds or asset classes and relies on periodic review rather than frequent security selection.

Many versions use broad market funds, including an index ETF, bond exposure, international equity exposure, or other diversified building blocks.

The word lazy describes the maintenance style, not the quality of the portfolio. A portfolio can be simple and still poorly matched to the investor if the exposures, weights, accounts, or review rules are not clear.

Why lazy does not mean unchecked

Low-maintenance structure can reduce decision fatigue because the investor does not need to constantly search for new securities. That does not mean the portfolio can be ignored. The main question is whether the simple structure still matches the job it was built to do.

The same three holdings can behave differently depending on account placement, tax constraints, cash needs, time horizon, and risk capacity. A portfolio that looks calm on a fund-count basis may still carry concentrated equity exposure, repeated sector exposure, or more volatility than the investor can practically tolerate.

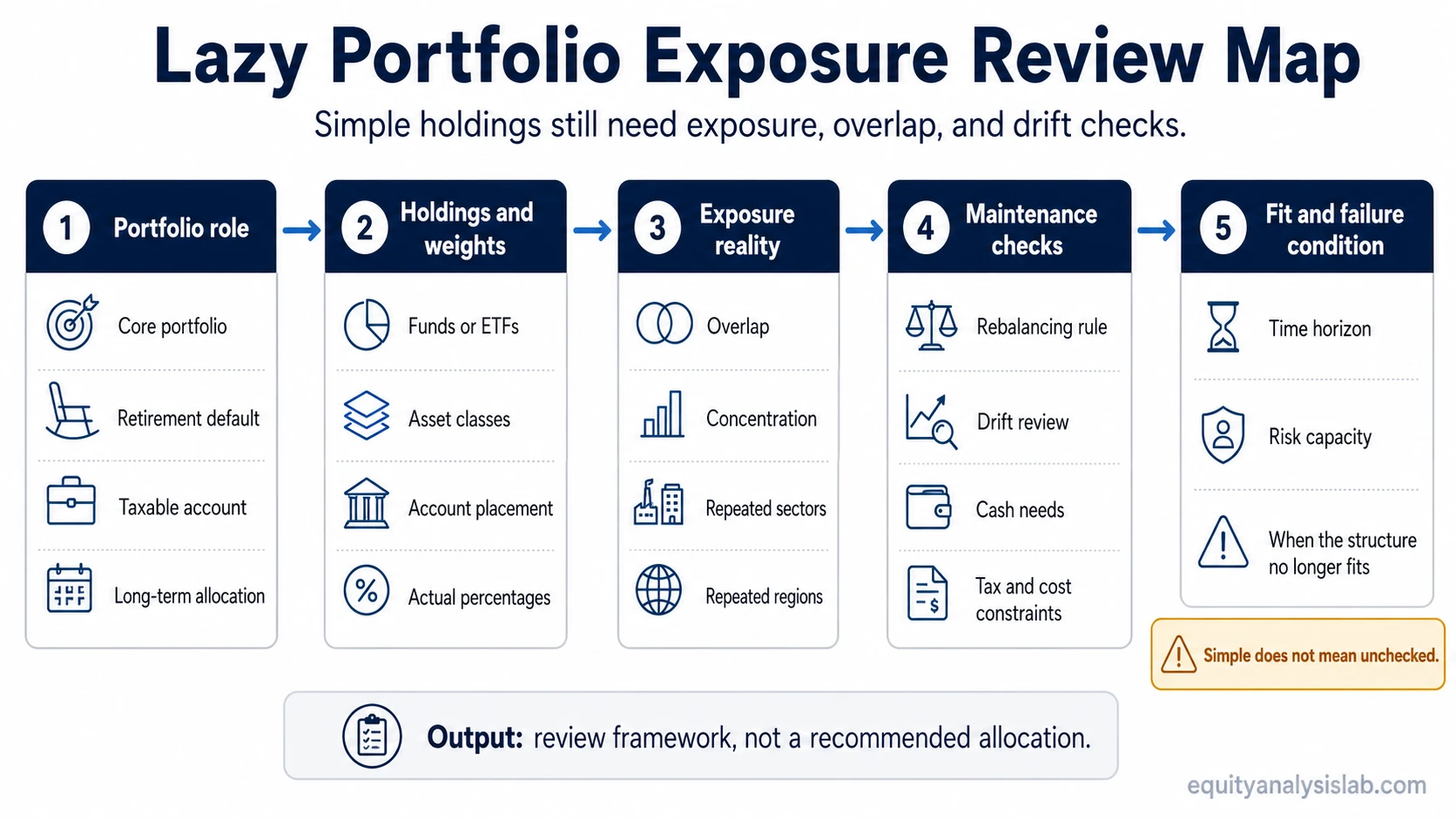

The lazy portfolio review sequence

A lazy portfolio works best as a review sequence rather than as a fixed model allocation. The sequence starts with the portfolio’s intended role, then checks whether the actual holdings and weights still support that role.

| Review area | What to check | Why it matters | What can go wrong |

|---|---|---|---|

| Intended role | Core portfolio, satellite sleeve, retirement default, or taxable account structure | The same fund mix can serve different jobs | A lazy structure may be used where a more specific objective is needed |

| Holdings | Funds, ETFs, asset classes, and accounts | The labels do not show full exposure | Multiple funds may own similar securities |

| Weights | Percent of each holding and asset class | Portfolio behavior follows weights, not names | A small number of funds can still create concentration |

| Overlap | Shared holdings, shared factors, repeated regions, or repeated sectors | Diversification can be overstated | Two different ETFs can behave similarly |

| Rebalancing rule | Calendar review or threshold review | Simplicity still needs maintenance | Drift can change risk exposure |

| Time horizon | When capital may be needed | Long-term structure may not fit short-term need | Volatility may exceed usable risk capacity |

| Failure condition | What would make the structure unsuitable | Prevents blind maintenance | The portfolio can remain simple but no longer fit the investor |

Holdings, weights, and exposure reality

The first practical check is whether the portfolio’s actual exposure matches its intended asset allocation. A lazy portfolio may use only a few holdings, but each holding can contain hundreds or thousands of securities. The portfolio’s real behavior comes from the weighted mix of those underlying exposures.

A simple fund list is therefore not enough. The investor needs to know how much of the portfolio is in equities, bonds, cash, international markets, domestic markets, sectors, factors, and any concentrated sleeves. A small holding may not matter much. A repeated exposure across several funds can matter more than the fund names suggest.

Example: simple holdings can still overlap

Consider a portfolio with three funds: a broad U.S. equity fund, a global equity fund, and a balanced fund that also owns U.S. stocks and bonds. On the surface, the portfolio looks simple because it has only three holdings. After looking through the funds, the investor may find that U.S. large-cap stocks appear in more than one place.

That does not automatically make the portfolio wrong. It shifts the question from fund count to exposure count: what does the combined portfolio actually own, and in what weight?

Overlap and concentration risk

Overlap appears when different funds hold similar securities, sectors, factors, or regions. This can make a lazy portfolio look more diversified than it really is. A portfolio with several funds may still depend heavily on the same equity market, sector group, company size, or style factor.

Diversification is stronger when exposures behave differently for understandable reasons. It is weaker when the portfolio only appears diversified because the holdings have different names. Each holding should add a distinct role rather than simply repeat an exposure already present elsewhere.

Rebalancing rules and drift

A lazy portfolio usually needs a simple maintenance rule. That rule may be calendar-based, threshold-based, or tied to cash flows. The goal is not to trade often. The goal is to prevent the portfolio from drifting so far that it no longer matches the intended allocation.

Rebalancing matters because market movement changes weights. If equity exposure rises from the intended allocation after a strong market period, the portfolio may carry more risk than planned. If bond or cash exposure rises after defensive activity, the portfolio may become less growth-oriented than intended.

The rule should be simple enough to follow and specific enough to prevent neglect. A vague intention to “check occasionally” can turn a low-maintenance framework into an unmanaged portfolio.

When a lazy portfolio framework weakens

The framework can weaken even when the holdings are low cost, diversified in name, and easy to maintain. The structure becomes less reliable when the investor cannot explain the role of each holding, when several funds repeat the same exposure, or when the rebalancing rule is unclear.

- Hidden overlap: Different funds may hold similar securities or factors, which can make diversification look stronger than it is.

- False diversification: More funds do not automatically mean more distinct exposure.

- Backtest overfit: Historical comparisons can describe past behavior, but they do not prove that one allocation will remain superior.

- Rebalancing neglect: A portfolio can drift away from its intended risk level if no review rule is followed.

- Risk-capacity mismatch: A portfolio may be logically built but still too volatile for the investor’s actual time horizon or cash needs.

Lazy portfolio vs related portfolio structures

A lazy portfolio is a maintenance framework. A three-fund portfolio is one possible simple structure inside that broader idea. ETF portfolio implementation is the process of selecting and organizing the actual funds used to express the allocation.

| Structure | Main idea | Review focus | Common confusion |

|---|---|---|---|

| Lazy portfolio | Low-maintenance portfolio structure | Exposure, overlap, weights, drift, and fit | Assuming simple means automatically suitable |

| Three-fund portfolio | A specific simple allocation pattern | Domestic equity, international equity, and bond exposure | Treating one structure as the only lazy portfolio format |

| ETF portfolio implementation | Using ETFs to express the chosen allocation | Fund selection, costs, tax placement, overlap, and account structure | Choosing funds before defining the portfolio role |

Practical lazy portfolio review checklist

A lazy portfolio review can stay simple if the questions are clear. Start with whether the portfolio still matches the intended role before focusing on individual funds.

- What job is this portfolio meant to do?

- Which holdings create the actual asset mix?

- What percentage of the portfolio does each holding control?

- Where do holdings overlap across securities, regions, sectors, or factors?

- Has market movement changed the intended allocation?

- What rebalancing rule decides when review becomes action?

- Does the portfolio still fit the investor’s time horizon and risk capacity?

- What condition would make the structure unsuitable?

The checklist protects the main advantage of a lazy portfolio: fewer moving parts. It also prevents the main weakness: assuming that fewer moving parts remove the need for review.

Where the lazy portfolio fits in portfolio construction

A lazy portfolio sits between broad allocation design and fund-level implementation. The allocation defines the intended exposure. The holdings express that exposure. The review rule keeps the structure from drifting into something different.

For an investor using ETFs, the stronger sequence is to define the intended role, map the real exposure, check overlap, and then decide whether the implementation remains simple enough to maintain.

Lazy portfolio FAQ

Is a lazy portfolio the same as a three-fund portfolio?

No. A three-fund portfolio is one common simple structure. A lazy portfolio is the broader idea of using a low-maintenance allocation and a simple review rule.

Does a lazy portfolio need rebalancing?

Usually, yes. The rule can be simple, but the portfolio still needs a way to check whether market movement has changed the intended weights.

Can a lazy portfolio still be concentrated?

Yes. Concentration can appear when multiple funds repeat similar holdings, sectors, regions, or factors. The number of funds does not prove diversification by itself.

Does a backtest prove which lazy portfolio is best?

No. A backtest can show how an allocation behaved in a historical period, but it cannot prove future suitability or remove the need to check risk capacity, time horizon, and exposure fit.