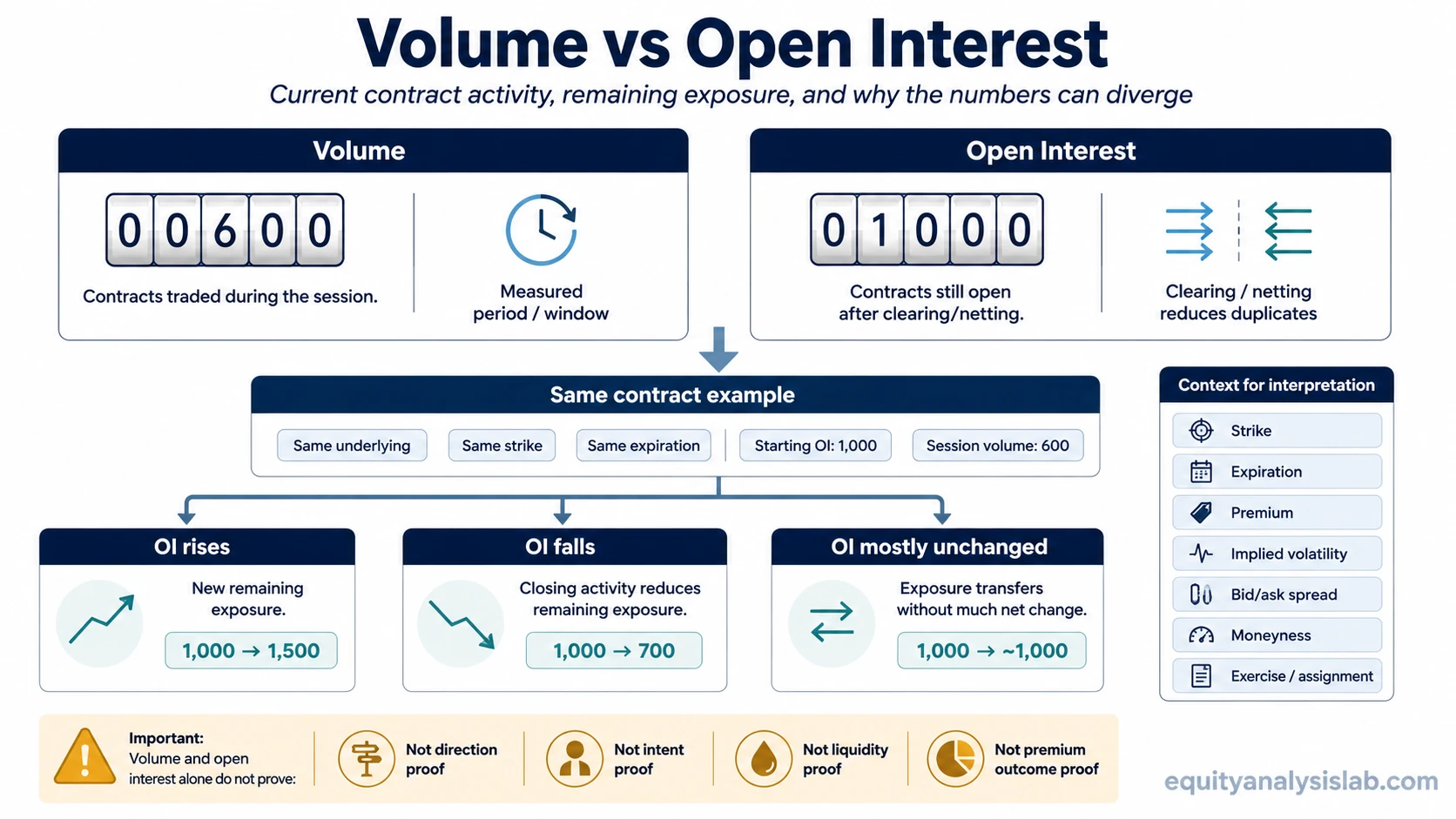

Options volume shows how many contracts traded during a session or measured period. Open interest shows how many contracts remain open after opening and closing activity has been netted. Volume is activity; open interest is remaining exposure.

The two numbers often sit next to each other on the same option-chain row, but they answer different questions. A contract can trade heavily while open interest rises, falls, or barely changes, depending on whether the day’s trades create new positions, close existing positions, or transfer exposure between participants.

Key Points

- Volume counts contracts traded during the measured period.

- Open interest counts contracts that remain open after clearing and netting.

- High volume does not prove that new exposure was created.

- High open interest does not reveal whether traders are bullish, bearish, hedged, or speculative.

- Both numbers need contract context: strike, expiration, premium, bid/ask spread, moneyness, implied volatility, and exercise or assignment boundaries.

The Core Difference: Activity vs Remaining Exposure

Options volume is the number of option contracts traded during a session or other measured period. It resets with the measurement window.

Open interest is the number of contracts that remain open after positions have been opened, closed, exercised, assigned, expired, or otherwise netted through clearing.

Volume is closer to a transaction count. Open interest is closer to a remaining-exposure count. The same contract can have high volume because new traders entered, existing traders exited, or ownership of exposure changed hands.

An option-chain row may show the underlying, strike, expiration, option type, premium, volume, and open interest, but it does not show every reason behind the trades or whether the exposure is directional, hedged, spread-based, or closing activity.

Volume vs Open Interest Comparison

| Metric | What it measures | When it updates | What it can show | What it cannot prove |

|---|---|---|---|---|

| Options volume | Contracts traded during the measured period | During the session or reporting window | Current activity in a specific contract | Whether trades opened new exposure, closed old exposure, or carried bullish or bearish intent |

| Open interest | Contracts still open after clearing and netting | After positions are processed and updated by the relevant data source | Remaining exposure in a specific contract | Who holds the exposure, why it exists, whether it is hedged, or whether the contract is easy to trade at a fair spread |

How Volume and Open Interest Can Move Differently

Volume rises whenever contracts trade. Open interest changes only when the net number of open contracts changes after opening and closing activity is processed.

If new buyers and new sellers create new contracts, open interest can rise. If existing holders close positions, open interest can fall. If exposure transfers between participants without changing the number of contracts that remain open, open interest may stay mostly unchanged even when volume is high.

This is why volume can be higher than open interest on a given day. A contract with modest open interest can trade many times during the session, especially if the same exposure changes hands repeatedly or if traders open and close positions within the same period.

Same Contract, Different Interpretation

Consider one call option on the same underlying, same strike, and same expiration. The contract begins the day with 1,000 contracts of open interest and trades 600 contracts during the session.

| End-of-day open interest result | Possible interpretation | What volume alone missed |

|---|---|---|

| Open interest rises from 1,000 to 1,500 | Much of the day’s trading likely created additional remaining exposure. | The 600 contracts of volume did not all disappear after the session; a large portion remained open. |

| Open interest falls from 1,000 to 700 | A meaningful part of the activity may have closed existing positions. | High volume did not mean new exposure increased. It may have reflected exits or position reduction. |

| Open interest stays near 1,000 | Contracts traded, but remaining exposure did not materially change. | The session was active, but activity and net exposure were different readings. |

The same 600 contracts of volume can support very different readings once open interest is updated. The useful comparison is activity versus the later change in remaining exposure, not volume by itself.

What Volume and Open Interest Can and Cannot Tell You

Volume can show that attention or activity increased in a contract. It does not identify opening trades, closing trades, hedges, spreads, or repeated intraday turnover.

Open interest can show that exposure remains open in a contract. It does not identify who holds the exposure, whether the position is directional, whether it is paired with stock, or whether it belongs to a multi-leg option structure.

Misuse warning: high volume is not a bullish or bearish proof, and high open interest is not the same as easy execution. A contract can show large open interest and still have a wide bid/ask spread, limited depth, unfavorable moneyness, short expiration risk, or assignment and exercise considerations that change the practical interpretation.

How to Read Volume and Open Interest in an Option Chain

Start with the contract row. Identify the underlying, option type, strike, and expiration before interpreting volume or open interest. A weekly out-of-the-money contract and a longer-dated near-the-money contract can show similar activity but carry very different premium behavior and risk boundaries.

Next, compare today’s volume with the existing open interest and the later change in open interest. If volume is high and open interest rises, remaining exposure may have expanded. If volume is high and open interest falls, closing activity may have dominated. If open interest barely changes, the trading may have been active without a meaningful change in net exposure.

Then check the bid/ask spread, premium, implied volatility, and moneyness. Volume and open interest can make a contract look active, but the tradable price may still be affected by spread width, volatility assumptions, time to expiration, and distance from the strike.

Finally, keep exercise and assignment boundaries in view. Open contracts can disappear through closing trades, expiration, exercise, or assignment, so a change in open interest is not always a clean directional message.

Common Mistakes When Comparing Volume and Open Interest

- Calling high volume new positioning: high volume may include closing trades or intraday turnover.

- Calling high volume bullish or bearish: the option chain does not reveal intent by volume alone.

- Calling high open interest liquidity: open interest can support context, but spread and depth still matter.

- Ignoring contract terms: strike, expiration, option type, moneyness, premium, and implied volatility change the meaning of the same metric.

- Ignoring netting: open interest reflects what remains open after processing, not every trade that occurred during the session.

Related Option Pricing and Liquidity Concepts

For liquidity context, volume and open interest should be read alongside options liquidity, because participation numbers do not replace spread, depth, and tradable-price checks.

For pricing context, Black-Scholes model assumptions and implied volatility help explain why active contracts can still behave differently from their raw activity numbers.

FAQ

Can options volume be higher than open interest?

Yes. Volume counts contracts traded during the measured period, while open interest counts contracts that remain open after clearing and netting. The same contract can trade many times during a session even if the number of remaining open contracts is smaller.

Does high open interest mean an option is liquid?

High open interest can suggest that a contract has existing participation, but it does not guarantee easy execution. Bid/ask spread, displayed size, market depth, expiration, and moneyness still affect liquidity.

Does high volume show whether traders are bullish or bearish?

No. High volume shows activity, not intent. The trades may be opening, closing, hedged, spread-based, speculative, or part of a larger position that is not visible from volume alone.

Why can open interest fall after a high-volume day?

Open interest can fall when much of the trading closes existing positions. A high-volume day can therefore reduce remaining exposure instead of increasing it.