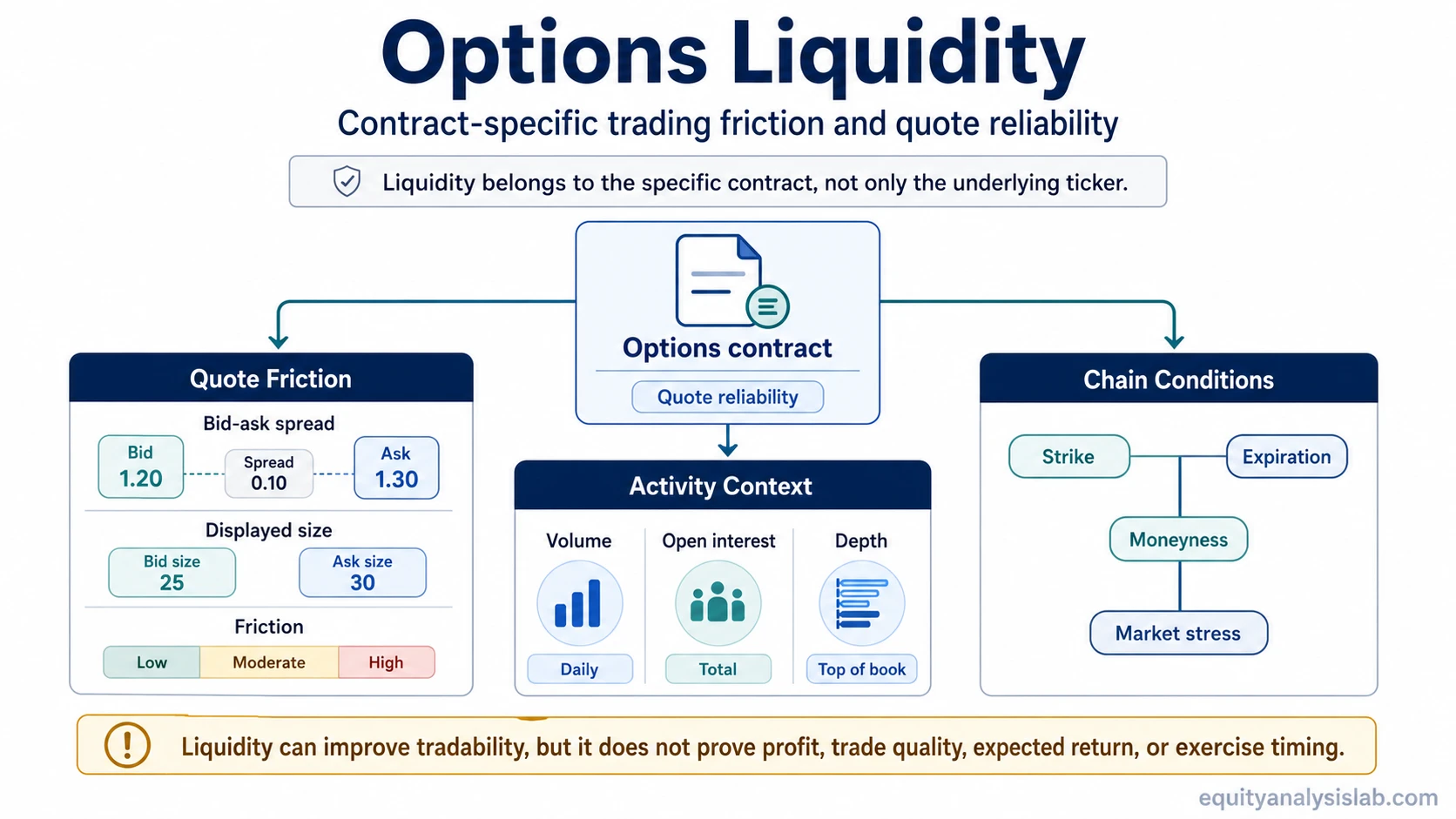

Options liquidity is the ease with which a specific options contract can be bought or sold near its quoted value without a large spread or price impact.

Liquidity is contract-specific. A company or ETF may be widely traded, while one strike, expiration, or option type in its options chain may still have weak depth, a wide bid-ask spread, or limited trading activity.

Definition: Options liquidity describes the tradability of a specific option contract. It is usually judged through bid-ask spread, volume, open interest, displayed size, depth, and how those conditions change across strikes, expirations, moneyness, and market conditions.

Liquidity affects transaction friction and quote reliability. It can make a contract easier or harder to interpret, but it does not make an option profitable, low risk, correctly priced, or suitable for any investor.

Key Points

- Options liquidity describes how easily a specific contract can trade near its quoted value.

- Bid-ask spread, volume, open interest, and displayed size show different parts of liquidity.

- Liquidity can vary by strike price, expiration date, moneyness, and market conditions.

- Liquidity affects transaction friction, not whether an options position is profitable or appropriate.

What Options Liquidity Means in a Contract

An option contract is defined by its underlying security, option type, strike price, and expiration date. Liquidity belongs to that specific contract, not only to the underlying ticker.

This distinction matters because listed options can have uneven activity across the chain. Contracts near commonly watched strikes or active expirations may have tighter markets, while far out-of-the-money, deep in-the-money, or longer-dated contracts may have less visible depth.

Option chain basics help organize these differences by showing how contracts are listed across strikes and expirations. Options liquidity explains whether those listed quotes are likely to represent tradable conditions with reasonable friction.

How Options Liquidity Is Measured

No single metric proves that an option is liquid. The most useful reading comes from combining quote width, trading activity, outstanding contracts, displayed size, and chain context.

| Liquidity metric | What it shows | What it does not prove |

|---|---|---|

| Bid-ask spread | The gap between the quoted buying price and quoted selling price. | A tight spread does not guarantee a perfect or risk-free transaction. |

| Volume | How many contracts have traded during the current session. | High daily volume does not prove that every strike or expiration has strong depth. |

| Open interest | How many contracts remain open from previous trading activity. | High open interest does not guarantee tight spreads or easy execution at the displayed quote. |

| Bid and ask size | The displayed number of contracts available at quoted bid and ask prices. | Displayed size can change and may not represent deep liquidity beyond the best quote. |

| Market depth | How much trading interest exists beyond the best bid and ask. | Depth can weaken during volatility, news, or fast-moving markets. |

| Underlying liquidity | The trading activity and depth in the stock or ETF linked to the option. | A liquid underlying does not make every option contract in the chain liquid. |

| Strike and expiration activity | Where trading interest is concentrated across the option chain. | Activity in one part of the chain does not automatically transfer to less active contracts. |

Why Bid-Ask Spread Matters

The bid-ask spread is often the clearest visible sign of liquidity friction. A narrower spread usually means the quoted market is tighter, while a wider spread can make the displayed option price less useful as an estimate of executable value.

This connects directly to option premium. The quoted premium may look precise, but the spread around that quote can change the practical cost of entering, adjusting, or closing a position.

Quote visibility and executable value are not the same thing. A quote can appear on the screen even when the gap between bid and ask is wide, displayed size is shallow, or conditions are changing quickly.

Example: One contract may show a narrow spread with meaningful displayed size on both sides of the market. Another contract may show a much wider spread with only small displayed size. Both contracts have visible quotes, but the second contract has more liquidity friction because the quoted value may be harder to treat as a realistic transaction reference.

Volume vs Open Interest in Liquidity

Volume and open interest are related, but they measure different things. Volume measures current-session trading activity. Open interest measures contracts that remain open after prior trading activity.

High volume can show that a contract is actively trading today. High open interest can show that a contract has accumulated participation over time. Neither measure, by itself, proves that the current bid-ask spread is tight or that the displayed quote has enough depth.

Volume vs open interest is especially important when a contract has a large outstanding base but weak current quote quality, or when a contract trades actively for one session without durable participation.

How Strike, Expiration, and Moneyness Affect Liquidity

Options liquidity often clusters unevenly. Contracts near active strikes and commonly traded expirations may attract more participation than contracts far away from current price or farther out on the expiration calendar.

Moneyness can also affect liquidity. At-the-money contracts often attract more attention because they sit close to the current underlying price, while far out-of-the-money or deep in-the-money contracts may have wider spreads or thinner displayed size. This is a tendency, not a universal rule.

Liquidity can also change when volatility changes. Rising uncertainty can widen spreads and reduce displayed depth because market participants may become less willing to quote tightly. Implied volatility affects option pricing, while liquidity affects how realistic the quoted market may be for a specific contract.

What Illiquid Options Can Change

Illiquid options can make the quoted premium harder to interpret. A wide spread may mean the midpoint, last price, or displayed quote gives an incomplete picture of the contract’s practical trading value.

Weak liquidity can also affect flexibility. If displayed depth is shallow or spreads widen, adjusting or exiting a position may involve more friction than the original quote suggested.

These risks become more visible when markets move quickly. Liquidity that looked acceptable under calm conditions can become weaker when volatility rises, the underlying price gaps, or fewer participants are willing to quote near the prior market.

Common Mistake: Treating One Metric as Proof

Common mistake: Reading high volume or high open interest as proof that an option contract is easy to trade at a fair quoted value.

The stronger reading is metric-based but not metric-dependent. Volume, open interest, spread, size, depth, strike activity, expiration activity, and market conditions all describe different parts of liquidity.

A contract can have notable open interest but still show a wide spread. Another contract can show strong volume during one session but have weaker depth later. Liquidity is more useful when the observable metrics point in the same direction.

Options Liquidity Is Not Trade Quality

Limitation: Options liquidity affects transaction friction and interpretation quality. It does not determine expected return, net profit, safety, strategy quality, or whether a contract should be exercised.

A liquid option can still be overpriced, risky, or unsuitable for an investor’s objective. An illiquid option can have an interesting theoretical price but still create practical friction through wide spreads and shallow depth.

Liquidity also does not decide contract rights or obligations. The distinction between exercise and assignment belongs to contract structure, while liquidity describes how the listed contract trades in the market.

Related Options Concepts

Several nearby concepts help separate liquidity from pricing, contract layout, quote interpretation, and contract obligations.

| Concept | How it connects to options liquidity |

|---|---|

| Option premium | Shows the quoted contract price that liquidity friction can make harder to interpret. |

| Option chain basics | Shows where strike, expiration, bid, ask, volume, and open interest appear together. |

| Open interest | Explains outstanding contracts, one of the main context metrics for liquidity. |

| Volume vs open interest | Separates current trading activity from contracts that remain open. |

| Implied volatility | Explains the volatility input in option pricing, which can interact with spread conditions. |

FAQ

Is open interest the same as volume?

No. Volume measures contracts traded during the current session. Open interest measures contracts that remain open from previous trading activity.

Can an option have visible quotes but still be illiquid?

Yes. A contract can show bid and ask quotes while still having a wide spread, shallow displayed size, weak depth, or rapidly changing quote conditions.

Does high liquidity mean an option is a good trade?

No. Liquidity can reduce friction and make quotes easier to interpret, but it does not prove expected return, safety, valuation quality, or suitability.