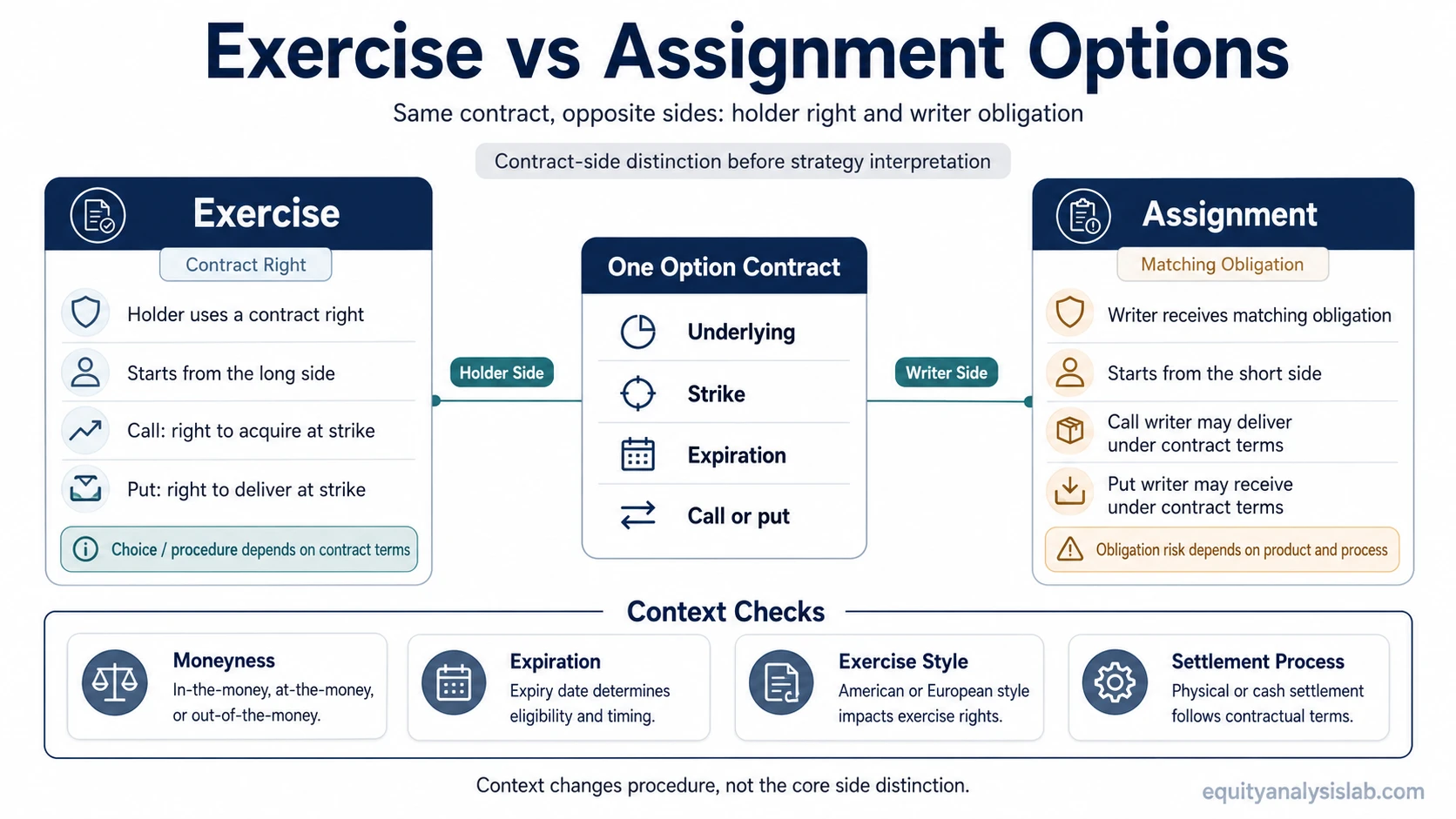

Exercise and assignment can occur around the same option contract, but they describe opposite sides of the contract process. Exercise is the holder’s use of a contract right. Assignment is the writer’s obligation after a holder exercises.

An exercise option begins with what the holder may choose to do with the contract. Assignment begins with what the writer may be required to deliver or receive after that choice is made.

One-sentence distinction: exercise is the option holder using a contractual right; assignment is the option writer being required to fulfill the matching obligation after that right is used.

Key Points

- Exercise belongs to the option holder side: the holder uses the contract right.

- Assignment belongs to the option writer side: the writer receives the matching obligation.

- Calls and puts create different buy, sell, delivery, or settlement consequences.

- Expiration, moneyness, exercise style, product type, and broker procedures can affect the final result.

Exercise vs Assignment Options: The Practical Difference

The practical difference starts with position side. A holder can exercise because the contract gives that side a right. A writer can be assigned because the short side accepted the matching obligation when the option was sold or written.

A call holder who exercises uses the right to buy the underlying at the strike price. A call writer who is assigned may be required to sell the underlying under the contract terms. A put holder who exercises uses the right to sell the underlying at the strike price. A put writer who is assigned may be required to buy the underlying under the contract terms.

This is why the comparison should be resolved before payoff, strategy, or risk interpretation. The same option contract can create a right for one side and an obligation for the other side.

Exercise vs Assignment Criteria Table

| Criterion | Exercise | Assignment |

|---|---|---|

| Side of the contract | Holder or buyer side | Writer or seller side |

| Who initiates the event | The holder chooses to use the contract right, or the option may be exercised under applicable expiration procedures. | The writer is selected to fulfill the obligation after an exercise occurs. |

| Right or obligation | A contractual right. | A contractual obligation. |

| Call option result | The call holder may buy the underlying at the strike price. | The call writer may have to sell the underlying at the strike price. |

| Put option result | The put holder may sell the underlying at the strike price. | The put writer may have to buy the underlying at the strike price. |

| Expiration role | Exercise can become more relevant near expiration, especially when an option is in the money. | Assignment risk is most visible for short options, but timing can vary by product and exercise style. |

| Main interpretation risk | Assuming exercise is automatically the best or only choice. | Assuming assignment only happens by choice or only at expiration. |

Same Contract, Different Side of the Obligation

Consider a generic call option on a stock with the same underlying, strike, and expiration for both sides of the contract. One investor holds the call. Another investor is short the call because that investor wrote or sold the contract.

If the call holder decides to exercise an option, the holder is using the contract right to buy the stock at the strike price. The holder’s action is exercise because it starts from the buyer side of the contract.

The writer does not “exercise” in that same event. If selected through the clearing and broker process, the writer is assigned and must fulfill the matching delivery obligation under the contract terms. The event is connected to the same option contract, but the label changes because the investor’s side changes.

The same structure works in reverse for puts. A put holder who exercises uses the right to sell at the strike. A put writer who is assigned may be required to buy at the strike.

Why Exercise and Assignment Are Confused

Exercise and option assignment are often confused because they can be connected to the same option chain, strike price, expiration date, and underlying. The confusion comes from treating the contract as one event instead of separating the two sides of the contract.

A second confusion comes from premium. Receiving premium may affect the economics of writing an option, but it does not remove the possibility that the writer may have to fulfill the contract if assignment occurs.

A third confusion comes from moneyness near expiration. An in-the-money option may make exercise or expiration procedures more relevant, but the final result still depends on the contract type, product rules, account instructions, and broker or clearing procedures.

Timing and Product-Type Caveats

Exercise and assignment timing is not identical for every option. American-style options may allow exercise before expiration, while European-style options generally limit exercise to expiration. Physically settled stock or ETF options can also create different practical consequences from cash-settled index options.

Automatic exercise is procedure-dependent. It should not be treated as a universal rule that overrides product terms, broker instructions, account status, transaction costs, or clearing procedures.

For this reason, exercise vs assignment should be read as a contract-side distinction first. Operational details can matter, but they do not change the core split between holder right and writer obligation.

What to Review Before Interpreting Exercise or Assignment Risk

A long option position raises exercise questions. A short option position raises assignment questions.

| Review item | Why it matters |

|---|---|

| Long or short option position | Long holders have contract rights; short writers accept contract obligations. |

| Call or put | Calls and puts create opposite buy/sell consequences for the underlying or settlement value. |

| Strike price versus underlying price | Moneyness affects whether exercise is economically relevant and whether expiration procedures may become important. |

| Expiration date | Exercise and assignment events become more visible as the contract approaches expiration. |

| Exercise style | American-style and European-style contracts can differ in when exercise may occur. |

| Settlement and account requirements | Physical settlement, cash settlement, margin, buying power, and broker rules can affect what happens after exercise or assignment. |

The review should stay mechanical before it becomes strategic. Knowing whether the issue is exercise or assignment helps separate contract rights from contract obligations before any decision about closing, holding, rolling, or exercising is considered.

FAQ

Is assignment the same as exercise?

No. Exercise belongs to the holder side of the contract. Assignment belongs to the writer side after exercise occurs.

Can assignment happen before expiration?

It can for some American-style options, depending on the product, position, and applicable procedures. European-style options generally limit exercise to expiration, so assignment timing can differ by contract type.

Does receiving premium remove assignment risk?

No. Premium is part of the economics of selling an option, but it does not remove the writer’s contractual obligation if assignment occurs.

Does an in-the-money option always have to be exercised?

No. In-the-money status makes exercise more relevant, especially near expiration, but product rules, broker procedures, account instructions, transaction costs, and other factors can affect the final outcome.