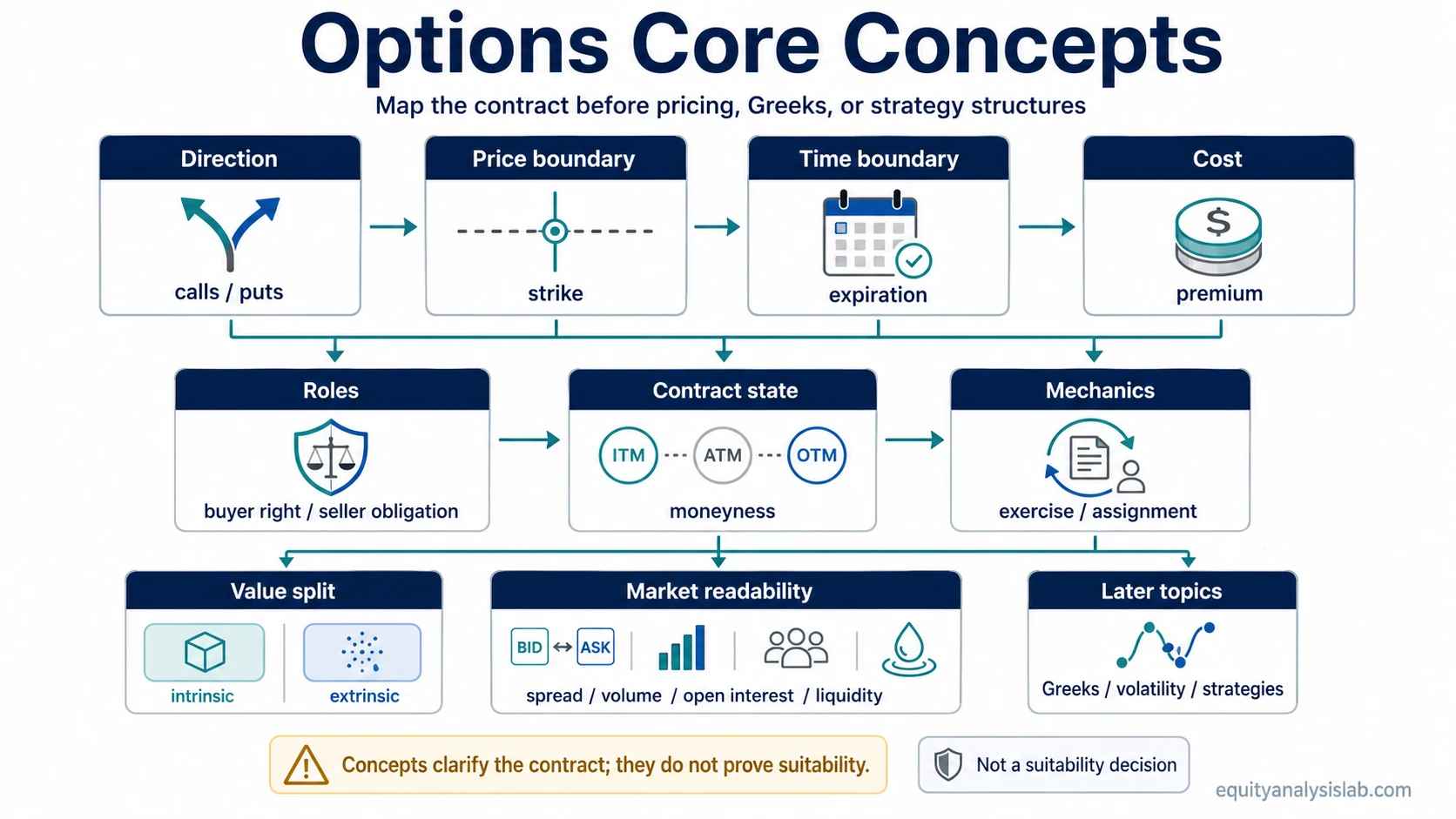

Options core concepts are the contract terms and risk boundaries that define how an option works before pricing models, Greeks, or strategy structures are added. The first layer is not a trade idea. It is the contract map: direction, strike, expiration, premium, rights, obligations, moneyness, exercise, assignment, value composition, and liquidity.

An option gives one side a contractual right and may place an obligation on the other side. A call and a put define the direction of that right. The strike price defines the price boundary. The expiration date defines the time boundary. The premium defines the upfront cost paid by the buyer and received by the seller. Moneyness, exercise, assignment, intrinsic value, extrinsic value, and liquidity then change how the contract is interpreted.

What Options Core Concepts Include

- Direction: calls and puts define whether the contract is built around upside participation or downside participation.

- Price boundary: the strike price defines the contract price at which the right can be exercised.

- Time boundary: expiration defines how long the contract remains valid.

- Cost and compensation: premium is the price paid by the buyer and received by the seller.

- Rights and obligations: the buyer controls the exercise right, while the seller may face assignment.

- Contract state: moneyness describes whether the contract is in the money, at the money, or out of the money.

- Value composition: intrinsic value and extrinsic value separate current exercise value from time and uncertainty value.

- Market readability: option chains, bid/ask spreads, volume, open interest, and liquidity help show whether the contract is easy or difficult to interpret and transact.

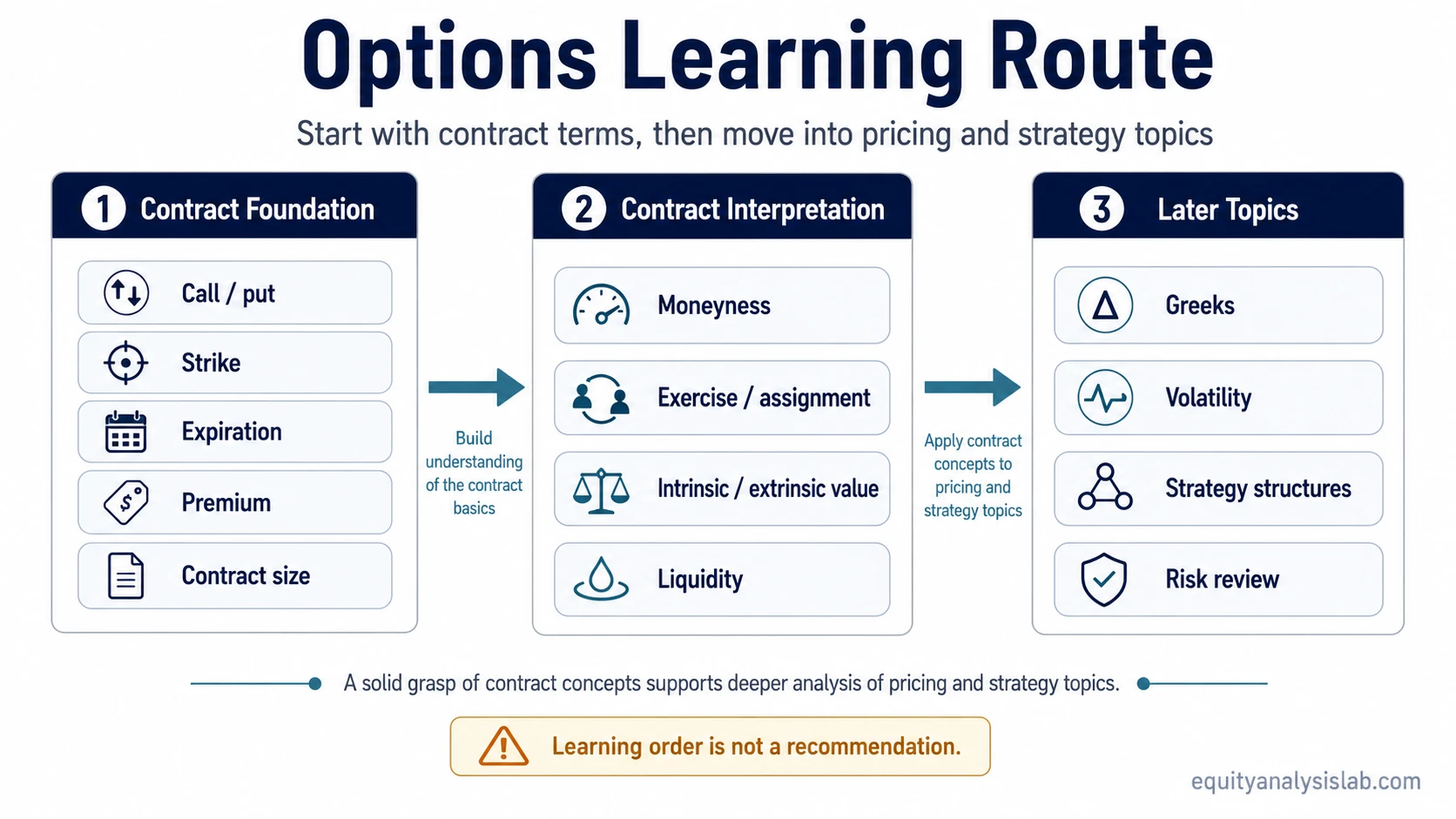

The First Concepts to Learn

A practical learning order starts with the contract itself. Pricing, Greeks, volatility structures, and options strategies are easier to evaluate after the basic contract terms are clear.

| Learning step | Concepts | What they control | Where to go next |

|---|---|---|---|

| 1. Direction | Call and put | The side of market movement the contract is designed around. | Call option and put option |

| 2. Price boundary | Strike price | The contract price used to determine exercise value. | Strike price |

| 3. Time boundary | Expiration date | The last date the contract can retain its contractual right. | Expiration date |

| 4. Cost | Option premium | The price paid to enter the contract as a buyer, and received by the seller. | Option premium |

| 5. Contract state | Moneyness | Whether the contract currently has exercise value, is near the strike, or has no current exercise value. | In the money option and out of the money option |

| 6. Exercise mechanics | Exercise and assignment | How the buyer’s right can become an action and how the seller’s obligation can be triggered. | Exercise option and assignment |

| 7. Value split | Intrinsic and extrinsic value | The difference between current exercise value and remaining time or uncertainty value. | Intrinsic value options and extrinsic value |

| 8. Market readability | Option chain and liquidity | Whether quotes, spreads, volume, and open interest make the contract easier to evaluate. | Option chain basics and options liquidity |

What Each Options Concept Changes in the Contract

Each core concept changes a different part of the same contract. Keeping those roles separate reduces confusion between payoff shape, time exposure, assignment risk, pricing sensitivity, and market liquidity.

| Contract function | Core concept | What changes | Common confusion to avoid |

|---|---|---|---|

| Direction | Call or put | Defines whether the right is linked to buying the underlying or selling the underlying at the strike. | A call or put is not a complete strategy by itself. |

| Price boundary | Strike price | Defines the contract price used for exercise and moneyness. | The strike is not a forecast or target price. |

| Time boundary | Expiration date | Defines when the contract right ends. | More time can change premium, but it does not remove uncertainty. |

| Cost | Premium | Defines the amount exchanged for the option contract. | Premium is not the same as total portfolio risk in every structure. |

| Rights and obligations | Buyer and seller roles | Defines who holds the exercise right and who may face assignment. | Buying an option and selling an option create different risk profiles. |

| Contract state | Moneyness | Defines whether the option is in the money, at the money, or out of the money. | Moneyness can change before expiration as the underlying price changes. |

| Exercise mechanics | Exercise and assignment | Defines how the contract can turn into an underlying position or obligation. | Exercise and assignment are related, but they are not the same action. |

| Value composition | Intrinsic and extrinsic value | Separates current exercise value from remaining time, uncertainty, and volatility-related value. | A contract can have premium even when it has no intrinsic value. |

| Market readability | Liquidity and option chain data | Shows whether the contract has usable quotes, volume, open interest, and spread conditions. | A listed contract is not automatically easy to trade or evaluate. |

Calls and Puts Set the Direction

A call option gives the buyer the right to buy the underlying at the strike price, while a put option gives the buyer the right to sell the underlying at the strike price. That difference defines the directional shape of the contract, but it does not decide whether the contract is attractive, safe, or appropriate.

The next question is not only whether the contract is a call or a put. The strike, expiration, premium, moneyness, liquidity, and seller obligation all change the contract’s risk and interpretation.

Options Contract Terms

The basic contract terms define the option before any strategy language is added. The underlying is the asset referenced by the contract. The strike price is the exercise price. The expiration date is the time boundary. The premium is the price of the option. Contract size defines how much underlying exposure the contract represents.

| Term | Plain meaning | Why it matters |

|---|---|---|

| Underlying | The asset the option contract references. | The option’s value is linked to the underlying asset’s price and conditions. |

| Strike price | The price used for the exercise right. | It defines the contract’s price boundary and moneyness. |

| Expiration date | The date when the contract right ends. | It limits how long the contract can retain time value. |

| Premium | The price paid for the option. | It reflects cost, compensation, time, volatility expectations, and contract demand. |

| Contract size | The amount of underlying exposure represented by one contract. | It affects how contract movement translates into position exposure. |

Rights, Obligations, Exercise, and Assignment

The buyer of an option owns a right. The seller of an option accepts an obligation that can matter if assignment occurs. That buyer-seller split is one of the most important differences between simply reading an option chain and understanding the contract’s risk boundary.

Exercise is the buyer using the contractual right. Assignment is the seller being required to fulfill the matching obligation. The distinction is easier to compare through exercise vs assignment options when the same contract is viewed from both sides.

Moneyness and Value Composition

Moneyness describes the relationship between the underlying price and the strike price. An in-the-money contract has current exercise value. An out-of-the-money contract does not have current exercise value. At-the-money contracts sit near the strike and can be especially sensitive to price movement, time, and volatility assumptions.

Intrinsic value and extrinsic value explain why moneyness does not tell the whole story. Intrinsic value is the contract’s current exercise value. Extrinsic value is the remaining premium beyond intrinsic value, often connected to time, uncertainty, volatility expectations, and supply-demand conditions in the option market.

The distinction becomes clearer in intrinsic value vs extrinsic value, where the same premium can be separated into exercise value and remaining contract value.

Option Chains and Liquidity Observables

An option chain organizes available contracts by expiration, strike, call side, put side, bid, ask, volume, open interest, and related quote data. The chain does not make a contract good or bad. It makes the contract visible enough to compare.

Liquidity matters because two contracts with similar strikes and expirations can behave differently if one has a wide bid/ask spread, low volume, or limited open interest. A thin contract may be harder to value cleanly or exit efficiently, even when the basic contract terms look simple.

| Observable | What it helps check | Limitation |

|---|---|---|

| Bid/ask spread | How wide the quoted buying and selling prices are. | A narrow spread can change quickly when conditions move. |

| Volume | How much trading activity has occurred over the measured period. | Volume can be temporary and does not guarantee future liquidity. |

| Open interest | How many contracts remain open. | Open interest does not show whether the next trade will be easy or cheap. |

| Expiration list | Which time boundaries are available. | Longer or shorter expirations change premium and risk exposure. |

| Strike list | Which price boundaries are available. | Nearby strikes can have very different premiums and liquidity. |

A Simple Route Example

Suppose two contracts reference the same underlying and both expire on the same date. One is a call with a strike near the current underlying price. The other is a put with a strike far below the current price. The first difference is direction: call versus put. The second difference is moneyness: near the strike versus far out of the money. The third difference is premium: the farther contract may look cheaper, but the lower price does not explain the probability, liquidity, time exposure, or assignment mechanics by itself.

A stronger read compares the contract terms in order: direction, strike, expiration, premium, moneyness, value composition, and liquidity. Only after that does it make sense to move into Greeks, volatility, or strategy structure.

How to Move Into Deeper Options Topics

Once the contract terms are clear, the next layer depends on the question being asked. A pricing question belongs with premium, intrinsic value, extrinsic value, volatility, and Greeks. A rights-and-obligations question belongs with exercise, assignment, and seller exposure. A chain-reading question belongs with liquidity, spread, volume, open interest, and expiration/strike comparison.

| If the question is about… | Start with… | Then compare… |

|---|---|---|

| How the contract direction works | Calls and puts | Strike, expiration, and premium |

| Whether the option has current exercise value | Moneyness | In the money vs out of the money |

| Why the option still has value before expiration | Intrinsic and extrinsic value | Premium, time remaining, and volatility exposure |

| How the contract can become an underlying position | Exercise and assignment | Buyer rights and seller obligations |

| How to read available contracts | Option chain basics | Bid/ask spread, volume, open interest, strike, and expiration |

| How basic contract terms fit together | How options work | Options basics |

What Options Core Concepts Do Not Decide

Core concepts make an option contract understandable, but they do not make an options position safe, suitable, or attractive. A contract can be simple and still carry meaningful risk. A low premium can still expire worthless. A high premium can still be justified by time, volatility, or demand. An in-the-money contract can still lose value if time, volatility, or the underlying price moves against the position.

| Concept | Useful for | What it does not prove |

|---|---|---|

| Premium | Understanding contract cost and compensation. | It does not prove the contract is cheap, expensive, safe, or suitable. |

| Expiration | Understanding the time boundary. | It does not remove path dependence or timing risk. |

| Moneyness | Understanding current relationship to the strike. | It does not predict where the underlying will finish. |

| Exercise | Understanding the buyer’s contractual right. | It does not mean exercise is always economically preferable to closing or holding. |

| Assignment | Understanding the seller’s potential obligation. | It does not occur in every contract, but it must be understood before selling options. |

| Liquidity | Understanding quote quality and market depth. | It does not guarantee stable spreads or easy execution in every market condition. |

| Greeks | Understanding sensitivity to price, time, volatility, and rates. | They do not replace the basic contract terms or guarantee an outcome. |

What Comes After the Core Concepts

After the core contract mechanics are clear, pricing and Greeks can explain sensitivity, while strategy pages can explain how multiple contracts are combined. That later layer should not replace the basics. A spread, hedge, or volatility structure still depends on the same building blocks: option type, strike, expiration, premium, moneyness, exercise, assignment, value composition, and liquidity.

FAQ

Which options concept should I learn first?

Start with calls and puts, then learn strike price, expiration date, option premium, and moneyness. Those concepts define the contract before pricing, Greeks, or strategies are added.

Is option premium the maximum risk?

For a simple purchased option, the premium is the upfront amount paid for the contract. That does not make premium a complete risk measure across all options structures, especially positions that involve selling options, multi-leg structures, margin, liquidity limits, or assignment obligations.

Do I need Greeks before learning calls and puts?

No. Greeks are easier to understand after the contract terms are clear. Calls, puts, strike, expiration, premium, moneyness, exercise, assignment, intrinsic value, extrinsic value, and liquidity should come first.