Options work as contracts that give the buyer a right and create a potential writer obligation around an underlying asset, strike price, expiration date, premium, and contract type.

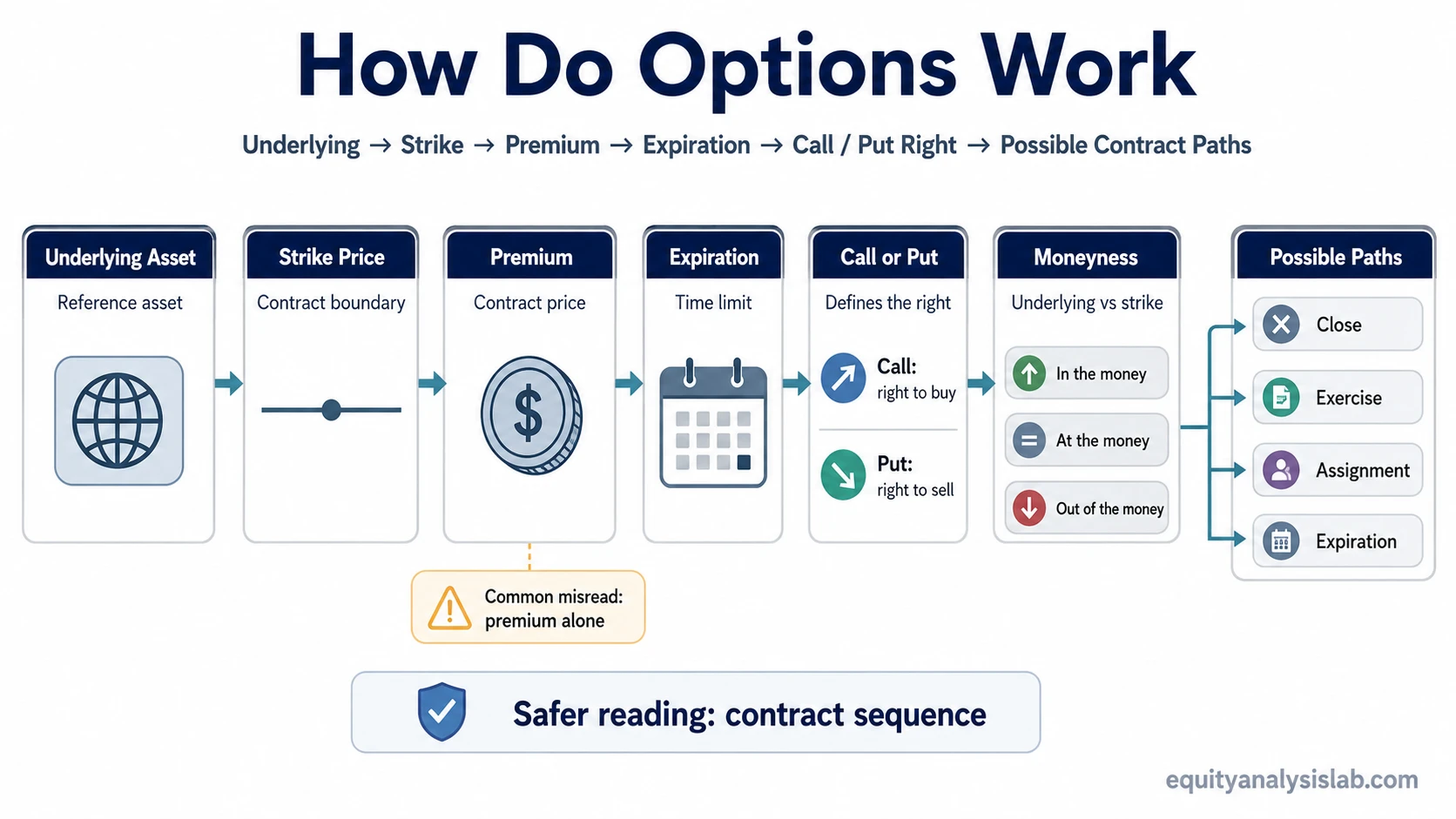

In sequence, the underlying sets the reference asset, the strike sets the contract boundary, the premium sets the contract cost, expiration sets the time limit, and call or put type defines the right.

The common misread is that an option is simply a cheaper way to control stock exposure. The safer interpretation is narrower: an option changes the exposure into a conditional contract. The result is shaped by where the underlying trades relative to the strike, how much premium was paid or received, how much time remains, whether volatility changes, and what happens before or at expiration.

Definition: An option is a contract whose value and outcome are shaped by the underlying asset, the strike price, the expiration date, the premium, and whether the contract is a call or a put.

Key Points

- An option buyer has a right, not an obligation, under the contract terms.

- An option writer receives premium but can take on an obligation if the contract is exercised and assigned.

- Calls and puts create different rights and obligations around buying or selling the underlying.

- Premium, strike price, expiration, time, volatility, and liquidity all affect interpretation.

- A payoff boundary is useful, but it does not capture every market friction or contract end-state.

The Misread: Options Are Not Just Cheaper Stock Exposure

An option can require less upfront cash than buying or shorting the underlying shares, but that does not make the exposure simpler. The premium can decay, volatility can change, liquidity can widen or narrow, and expiration can turn a flexible position into a contract boundary.

Misread: The premium is the whole story because it is the amount paid for the contract.

Safer interpretation: Premium is only one part of the mechanics. The contract also has a strike, expiration, type, moneyness, liquidity profile, and possible exercise or assignment path.

The distinction is especially important when comparing a simple long option with a written option. A long option buyer may have a defined premium at risk in a simple long call or long put, while the writer can face a different obligation profile if the contract is assigned.

The Basic Option Contract Terms

Each option contract is built from a small set of terms. These terms work together rather than separately, which is why reading only the strike price or premium can give an incomplete picture.

| Contract term | What it controls | Why it changes the result |

|---|---|---|

| Underlying asset | The stock, ETF, index, or other reference asset tied to the option | The option value moves from the relationship between the contract terms and the underlying price. |

| Strike price | The contract price at which the underlying may be bought or sold if exercised | The strike creates the key boundary for moneyness and payoff classification. |

| Expiration date | The date when the contract reaches its contractual end point | Time remaining affects option value and determines when the contract must be resolved. |

| Premium | The price paid by the buyer and received by the writer | Premium affects breakeven math and reflects time, volatility, and other pricing inputs. |

| Call or put | The type of right created by the contract | A call relates to buying the underlying; a put relates to selling the underlying. |

| Contract size | The quantity of underlying exposure represented by the contract | Many standard listed equity options represent 100 shares, although contract specifications should always be checked. |

Buyer Rights and Writer Obligations

The buyer and writer are on different sides of the contract. The buyer pays the premium for a right. The writer receives the premium and accepts a potential obligation if the contract is exercised and assigned.

That difference prevents a common risk mistake. A simple long option has a different risk boundary from a short option. The buyer’s premium can define the maximum loss for a simple long call or long put, but the writer’s exposure is shaped by contract type, underlying movement, collateral, exercise style, and assignment mechanics.

When the writer is assigned, assignment turns the contract obligation into a required contract outcome according to the terms of the option.

How Calls and Puts Work Differently

Calls and puts use the same contract building blocks, but the direction of the right is different. A call is linked to buying the underlying at the strike. A put is linked to selling the underlying at the strike.

| Contract type | Buyer right | Writer obligation if assigned | Basic strike relationship |

|---|---|---|---|

| Call option | Right to buy the underlying at the strike price | Potential obligation to sell the underlying at the strike price | Creates positive intrinsic exposure for the buyer when the underlying is above the strike, while the full result still depends on premium and contract path. |

| Put option | Right to sell the underlying at the strike price | Potential obligation to buy the underlying at the strike price | Creates positive intrinsic exposure for the buyer when the underlying is below the strike, while the full result still depends on premium and contract path. |

The call or put label alone is not enough. The contract still needs the strike, premium, expiration, and market context to explain how the result may unfold.

How Premium, Strike Price, and Expiration Shape the Result

The strike price defines the contract boundary. The premium defines the price of the contract. Expiration defines the time limit. These three terms interact, which is why an option can move differently from the underlying asset.

Moneyness describes where the underlying price sits relative to the strike. A call is in the money when the underlying is above the strike, while a put is in the money when the underlying is below the strike. At the money means the underlying is near the strike. Out of the money means the strike relationship has no immediate exercise value.

The portion of option value that comes directly from the favorable strike relationship is intrinsic value in options. Any remaining value usually reflects time, expected movement, volatility, rates, dividends where relevant, and market pricing conditions.

Interpretation note: A contract can be directionally correct and still produce a disappointing result if premium, time decay, volatility change, and transaction conditions overwhelm the simple directional move.

What Happens Before or At Expiration

An option contract does not have only one possible ending. Closing an option before expiration is different from exercising it: closing offsets the market position, while exercise uses the contract right under the option terms.

Depending on the position, contract terms, and market conditions, an option may be closed, exercised, assigned, or allowed to expire.

| Possible path | What it means | Boundary to understand |

|---|---|---|

| Closed before expiration | The position is offset before the contract reaches expiration. | The result is based on the option’s market price at closing, not only final expiration value. |

| Exercised | The holder uses the contract right under the option terms. | Exercise mechanics vary with contract type and exercise style. |

| Assigned | The writer is matched with the exercised contract obligation. | The writer’s obligation depends on whether the contract is a call or a put. |

| Expires | The contract reaches expiration without remaining exercise value or without further action. | Expiration removes the remaining time value and resolves the contract boundary. |

Expiration and assignment are not afterthoughts. They are part of the mechanics map because they describe how a contract can move from price exposure into a final contractual state.

A Simple Hypothetical Options Example

A stock trades at $50. A call option has a $55 strike, a $2 premium, and a future expiration date. The buyer pays $2 for the right to buy the stock at $55 before or at expiration, depending on contract style. The writer receives the $2 premium and accepts the potential obligation attached to the contract.

If the stock remains below $55 at expiration, the call has no intrinsic value at that boundary. If the stock is near $55, the strike relationship may be close, but the premium still matters. If the stock is above $55, the call can have intrinsic value, but the buyer’s full result still depends on the premium paid and any closing or exercise path.

If the stock rises only slightly above the strike, the call may have intrinsic value while still failing to overcome the premium and transaction frictions. That weak case is why strike relationship and final economic result should not be treated as the same thing.

Diagnostic reading: The $55 strike explains the contract boundary, but the $2 premium changes the economic result. The example also excludes changes in volatility, liquidity, transaction costs, exercise style, and any decision to close the option before expiration.

The Common Mistake: Treating the Premium as the Whole Risk Story

Premium is visible and easy to remember, so it often becomes the entire mental model. That creates two problems. First, a simple long option’s premium risk does not describe the writer’s risk. Second, a payoff diagram at expiration does not show every path the option can take before that date.

Common mistake: Reading a low premium as low risk without checking strike distance, time remaining, volatility, liquidity, and the buyer-writer boundary.

Better check: Start with the contract terms, then separate simple long-option premium risk from writer obligations and market conditions.

A payoff chart can clarify the expiration boundary, but it is a simplified map. The path before expiration can still be affected by volatility changes, bid-ask spreads, early exercise rules where applicable, and the ability to exit or adjust the position.

When the Mechanics Become Harder to Interpret

The basic contract terms are stable, but interpretation becomes harder when the option market itself is thin, volatile, or expensive relative to the expected movement. Wide spreads, low trading activity, and limited depth can make a theoretical contract value harder to realize in practice.

Option market liquidity matters because the option price a model implies and the price available in the market may not match cleanly for smaller or less active contracts.

Limitation: Contract mechanics explain the rights, obligations, and payoff boundaries, but they do not guarantee that a position can be entered, exited, or valued at an ideal theoretical price.

Volatility can also change the reading. A higher premium may reflect greater expected movement, but it also raises the cost of exposure for the buyer. A lower premium may look cheaper, but it may reflect less time, lower expected movement, or weaker market demand for that contract.

How Options Mechanics Connect

The cleanest way to read an option is as a sequence rather than as a single term. The underlying asset sets the reference point. The strike creates the contract boundary. The premium prices the exposure. Expiration creates the time limit. The call or put type defines the right. Exercise and assignment describe possible end-state mechanics.

Mechanics sequence: underlying asset → strike price → premium → expiration → call or put right → moneyness → possible close, exercise, assignment, or expiration.

The contract terms describe how the instrument works; they do not decide whether any option position fits a specific investor, portfolio, time horizon, or risk boundary.

FAQ

How do options work in simple terms?

Options work by creating a contract right for the buyer and a potential obligation for the writer. The result depends on the underlying asset, strike price, premium, expiration date, and whether the option is a call or a put.

Is buying an option the same as buying the stock?

No. Buying an option gives contract exposure to the underlying, not ownership of the underlying shares by itself. Ownership can occur only through specific exercise or assignment mechanics, depending on the contract and position.

Why does the premium matter in an option contract?

The premium is the price of the option contract. It affects the buyer’s cost, the writer’s compensation, and the economic result after comparing the underlying price, strike price, time remaining, and expiration boundary.

What can happen to an option at expiration?

An option may expire without value, be exercised, result in assignment for the writer, or have been closed before expiration. The possible path depends on the position, contract type, moneyness, and contract terms.