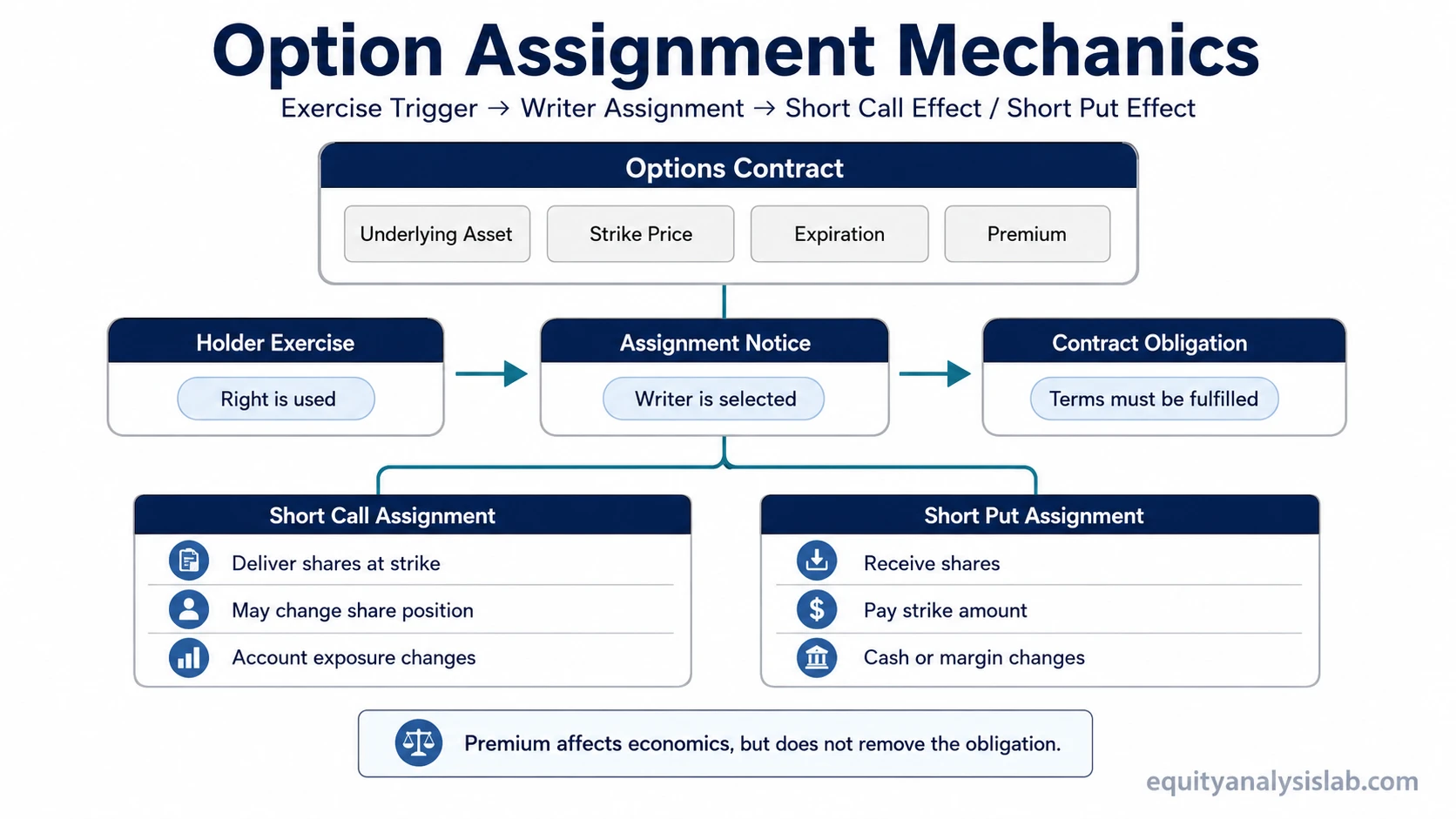

Option assignment is the seller-side obligation that occurs when an option holder exercises a contract. The buyer chooses whether to exercise; the assigned seller must fulfill the contract terms. For a short call, that usually means delivering or selling shares at the strike price. For a short put, it usually means buying shares at the strike price.

Key Points

- Option assignment applies to the option seller after the buyer exercises.

- Assignment creates a contract obligation, not a new choice for the seller.

- Short calls and short puts create different stock and cash effects.

- Premium received is part of the economics, but it does not remove assignment exposure.

- Assignment timing can be uncertain, especially for American-style options before expiration.

What Is Option Assignment?

Option assignment means an option seller is selected to fulfill the obligation created by an exercised options contract. The assigned seller must follow the contract terms for the underlying asset, strike price, expiration, and option type.

Assignment belongs to the obligation side of an options contract. The holder of a call option or put option owns a right. The seller, also called the writer, has a conditional obligation if the holder uses that right.

The important boundary is that assignment is a contract event, not a forecast or strategy signal. Once assignment occurs, the account may receive or lose shares, use cash, create a stock position, or close an existing position depending on the contract and account position.

How Option Assignment Works

Assignment starts with exercise. An option holder submits an exercise instruction, or exercise occurs according to the relevant contract and brokerage process. The assignment process then identifies one or more sellers who must satisfy the contract obligation.

For standard listed equity options, one contract typically represents 100 shares. That multiplier matters because assignment is not based only on the premium received. It can create a stock transaction tied to the full contract size.

The observable inputs are the contract type, the underlying asset, the strike price, the expiration date, the premium, the option style, and whether an exercise notice or exercise-related trigger has occurred. Those inputs define the boundary of the obligation, but they do not make assignment timing perfectly predictable.

Assignment vs Exercise

Assignment and exercise option mechanics describe opposite sides of the same contract event. Exercise is the buyer-side action. Assignment is the seller-side obligation that can follow that action.

| Concept | Who It Applies To | What It Means | Main Effect |

|---|---|---|---|

| Exercise | Option buyer or holder | The holder uses the contractual right | Creates a transaction request under the contract terms |

| Assignment | Option seller or writer | The seller is selected to fulfill the obligation | Creates a delivery, purchase, sale, or cash/account effect |

This distinction prevents a common misunderstanding. A seller does not “exercise” the short option. The seller is assigned after the holder exercises or after an exercise-related process applies.

Short Call Assignment

Short call assignment occurs when a call seller is assigned after the call holder exercises. The seller must deliver or sell the underlying shares at the strike price, subject to the contract terms and account position.

If the seller already owns the shares, as in a covered call, assignment may remove those shares from the account in exchange for the strike price. If the seller does not own the shares, the result may involve a short stock position or another broker-specific account effect.

Key distinction: A short call creates a potential obligation to deliver or sell the underlying. The premium received does not cancel that delivery obligation if assignment occurs.

Short Put Assignment

Short put assignment occurs when a put seller is assigned after the put holder exercises. The seller must buy the underlying shares at the strike price, subject to the contract terms and account position.

For an investor, this can create a new long stock position and require enough account cash or margin capacity to support the purchase. The economic result depends on the strike price, premium, share price, transaction costs, and the account’s broader position.

Key distinction: A short put creates a potential obligation to buy the underlying. The seller cannot treat the received premium as protection against the full purchase obligation.

Short Call vs Short Put Assignment

| Short Option | Assignment Obligation | Typical Account Effect | Main Risk Area |

|---|---|---|---|

| Short call | Deliver or sell the underlying at the strike price | Shares may be removed, sold, or a short stock exposure may result | Upside move in the underlying and share delivery exposure |

| Short put | Buy the underlying at the strike price | Cash or margin may be used to purchase shares | Downside move in the underlying and purchase obligation |

The difference is mechanical, not a prediction. Short call assignment and short put assignment both come from the same contract logic: the buyer has a right, and the seller has the matching obligation.

What Can Trigger Assignment?

Assignment depends on exercise. The option holder may exercise because the contract is economically useful, because expiration processing applies, or because other contract-specific factors make exercise relevant. For American-style options, exercise may be possible before expiration. For European-style options, exercise is generally limited to expiration.

Moneyness can influence the likelihood of exercise, especially when an in-the-money option has economic value to the holder. Dividends, interest rates, remaining time value, liquidity, contract style, and broker or clearing procedures can all affect how assignment risk is experienced by the seller.

Limitation: Assignment should not be reduced to “in the money equals assigned.” Moneyness and intrinsic value matter, but assignment is still tied to actual exercise and the mechanics of the option contract.

What Changes After Assignment?

After assignment, the short option obligation turns into an account-level result. The specific result depends on the contract type, account holdings, cash balance, margin rules, and broker processing.

| Input | Why It Matters |

|---|---|

| Option type | Determines whether the obligation is to buy or sell the underlying |

| Strike price | Sets the transaction price used in assignment |

| Contract size | Determines the number of shares or units involved |

| Account position | Determines whether assignment removes shares, creates shares, uses cash, or creates another exposure |

| Option style | Affects whether early exercise and early assignment can occur |

Premium Does Not Remove Assignment Risk

Option sellers receive premium when they sell an option, but the premium is not a shield against assignment. It is part of the position’s economics. The obligation remains attached to the short option until the position is closed, expires, or is otherwise resolved.

This matters because a small premium can be attached to a much larger notional obligation. A standard equity option contract can involve 100 shares, so assignment can create a larger stock or cash impact than the premium alone suggests.

Common mistake: Treating premium as if it fully compensates for assignment exposure can understate the account effect of a short call or short put.

Assignment and Investor Decision Process

For investor education, assignment is best understood as a contract mechanics issue before it is treated as a portfolio question. The first task is to identify the option type, contract size, strike price, expiration, account position, and possible exercise conditions.

Only after the mechanics are clear can the investor evaluate the position’s role, risk, liquidity needs, tax considerations, and fit within a broader portfolio. Those portfolio questions are separate from the definition of assignment itself.

Assignment also connects to broader options concepts such as expiration timing, moneyness, intrinsic value, and the stock position created or removed when the contract is fulfilled.

Common Misunderstandings About Assignment

| Misunderstanding | More Accurate View |

|---|---|

| The seller chooses assignment | The buyer exercises; the seller may be assigned to fulfill the obligation |

| Assignment only matters at expiration | Early assignment may occur for American-style options |

| Premium removes assignment exposure | Premium affects economics but does not cancel the contractual obligation |

| All in-the-money options are assigned immediately | Moneyness matters, but exercise and assignment mechanics still control the event |

FAQ

What does option assignment mean?

Option assignment means an option seller is selected to fulfill the obligation created when an option holder exercises. For a short call, that may require delivering or selling shares. For a short put, that may require buying shares.

Is assignment the same as exercise?

No. Exercise is the buyer-side action of using the option right. Assignment is the seller-side obligation that can follow exercise.

Can a call option be assigned?

A short call can be assigned if the call holder exercises and the seller is selected to fulfill the obligation. The assigned seller may need to deliver or sell shares at the strike price.

Can assignment happen before expiration?

For American-style options, assignment may occur before expiration if early exercise occurs. Assignment timing is not guaranteed by moneyness alone.

Does premium protect the seller from assignment?

No. Premium affects the economics of the position, but it does not remove the seller’s contractual obligation if assignment occurs.