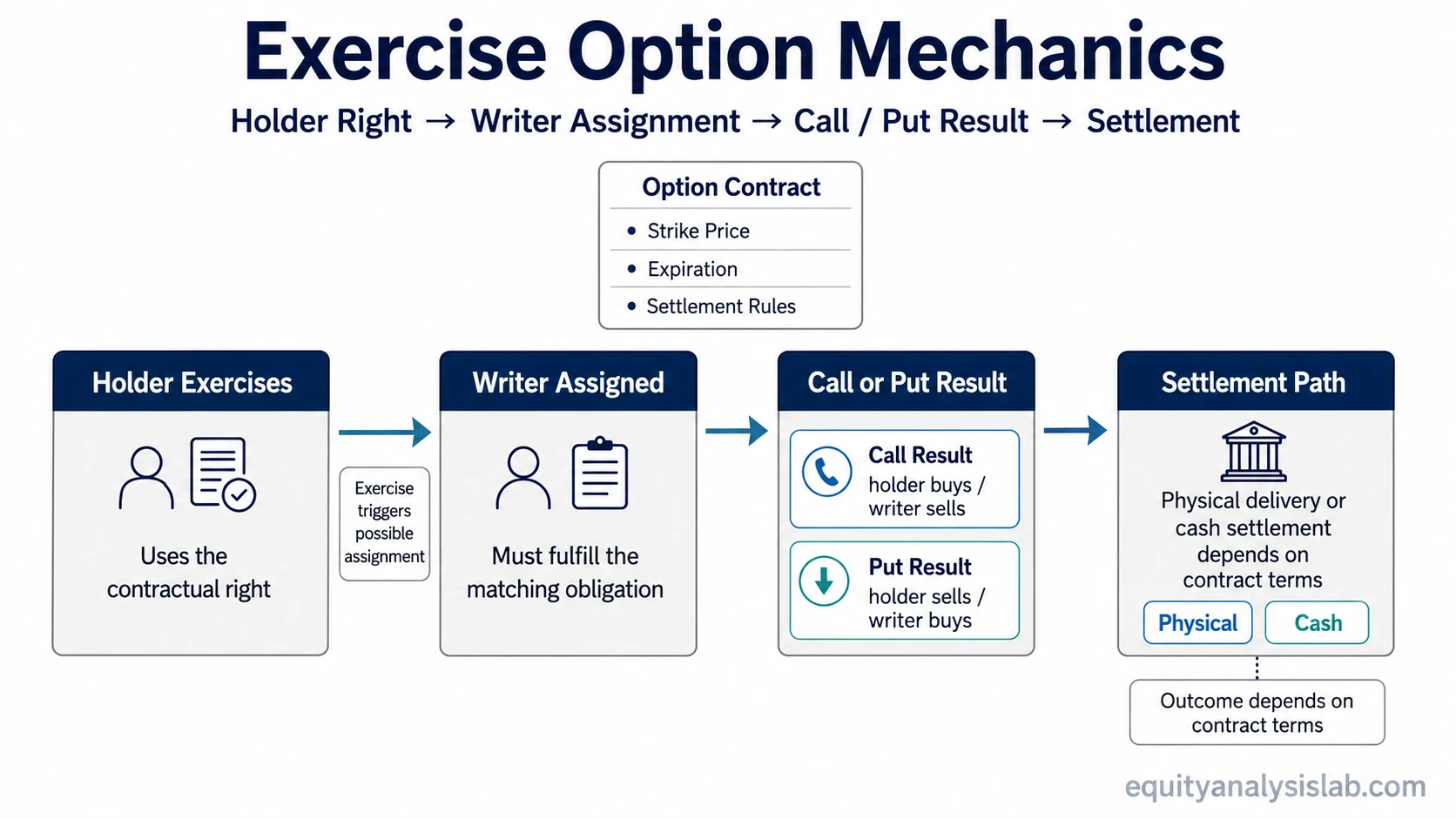

To exercise an option means to use the right inside an option contract. When a call is exercised, the holder uses the contract to buy the underlying asset at the strike price. When a put is exercised, the holder uses the contract to sell the underlying asset at the strike price. The writer can then be assigned and must meet the matching obligation.

Exercise is a contract mechanics event, not a return guarantee or an instruction to act. It changes how the option right is converted into an underlying position, cash settlement, or other settlement outcome based on the contract terms. The useful question is not only whether the contract can be exercised, but what right, obligation, expiration rule, premium value, and settlement method are connected to that exercise.

What Is an Exercise Option?

To exercise an option means to use the contractual right attached to the option. The right belongs to the option holder. The obligation belongs to the option writer if the writer is assigned. That separation is central to how options work mechanically, because an option is not only a price quote on a screen. It is a contract with defined rights, deadlines, and possible settlement consequences.

The core components are the underlying asset, strike price, expiration date, option type, exercise style, and settlement method. The strike price sets the contract price used if exercise occurs. The expiration date sets the deadline. The option type determines whether the right is to buy or sell. The settlement method determines whether the result involves shares, cash, or another contract-defined settlement process.

Definition: Exercising an option is the holder’s use of the contract right to buy or sell the underlying asset at the strike price, or to receive the contract-defined settlement value where cash settlement applies.

| Component | Role in exercise |

|---|---|

| Holder right | Determines who can choose to use the option contract. |

| Writer obligation | Determines what the short side may have to fulfill if assignment occurs. |

| Strike price | Sets the contract price used for the buy, sell, or settlement calculation. |

| Expiration | Sets the deadline for the exercisable right and related expiration rules. |

| Premium value | Separates immediate exercise value from the option’s remaining market value. |

| Settlement method | Determines whether the result is physical delivery, sale, purchase, or cash settlement. |

What Happens When an Option Is Exercised?

After exercise, the option right is converted into the result defined by the contract. For a physically settled equity option, that usually means the underlying shares are bought or sold at the strike price. For a cash-settled contract, the outcome is normally a cash adjustment based on the settlement rules rather than delivery of shares.

The option writer is on the other side of that process. If assignment occurs, the writer must fulfill the matching obligation. A short call writer may have to deliver or sell the underlying according to the contract terms. A short put writer may have to buy or receive the underlying according to the contract terms. If the contract is cash-settled, the assigned obligation is handled through the relevant cash settlement process.

The exact operational path depends on the contract, clearing process, broker, account permissions, and market rules. For an investor, the main concept is simpler: exercise turns an option right into the contract’s settlement result, while assignment turns the writer’s short option exposure into a required obligation.

Call Exercise vs Put Exercise

A call option gives the holder the right to buy the underlying at the strike price. A put gives the holder the right to sell the underlying at the strike price. The writer’s position is the mirror image of that right if assignment occurs.

| Position or event | Contract effect | Investor interpretation |

|---|---|---|

| Long call exercise | The holder buys the underlying at the strike price. | The option right becomes long exposure to the underlying or a contract-defined settlement result. |

| Long put exercise | The holder sells the underlying at the strike price. | The option right becomes a sale or settlement result based on the contract terms. |

| Short call assignment | The writer must meet the call obligation. | The writer may have to sell or deliver the underlying, or settle in cash if the contract requires cash settlement. |

| Short put assignment | The writer must meet the put obligation. | The writer may have to buy or receive the underlying, or settle in cash if the contract requires cash settlement. |

This table describes mechanics only. It does not determine whether exercising, selling, closing, holding, or allowing expiration rules to apply is economically preferable in a specific account or market condition.

Exercise vs Assignment

Exercise and assignment are connected, but they are not the same event from the same side of the contract. Exercise is initiated from the holder side. Assignment is the writer-side consequence when a short option is selected to fulfill the exercised contract obligation.

| Term | Who it applies to | Meaning |

|---|---|---|

| Exercise | Option holder | The holder uses the option right attached to a call or put. |

| Assignment | Option writer | The writer is required to fulfill the matching contract obligation. |

| Settlement | Both sides | The contract outcome is completed through share delivery, purchase, sale, or cash settlement depending on the contract. |

The distinction matters because the holder controls whether an exercisable right is used within the contract rules, while the writer accepts assignment risk when holding a short option position. A writer cannot treat assignment as separate from the original short option obligation.

Moneyness, Premium, and Exercise Value

Moneyness describes the relationship between the underlying price and the strike price. A contract can be in the money, at the money, or out of the money. Exercise is most directly connected to contracts with intrinsic value, but moneyness alone does not answer every economic question.

For a call, intrinsic value exists when the underlying price is above the strike price. For a put, intrinsic value exists when the underlying price is below the strike price. An in-the-money relationship means the contract has intrinsic value before considering transaction costs, liquidity, taxes, or account-specific effects.

An option’s market price can include more than intrinsic value. Time remaining, volatility expectations, liquidity, interest rates, dividends, and supply-demand conditions can contribute to the market value. That is why the market price paid or received for the contract can differ from the value that would be captured by exercising it immediately.

Limitation: Exercise can capture intrinsic value, but it can also give up remaining extrinsic value if the option could have been sold or closed for more than its immediate exercise value. That is a mechanics issue, not a universal rule that exercise is good or bad.

Why Exercise Can Differ From Selling or Closing

Exercising an option uses the contract right. Selling or closing the option exits the option position in the market. These actions can lead to different economic results because the option itself may still trade with extrinsic value.

For example, assume a call has a strike price of 50 and the underlying trades at 56. The call has 6 of intrinsic value. If the option still trades for 7 because time value and volatility expectations remain, immediate exercise would capture the intrinsic relationship but may give up the extra 1 of market value. This simplified example excludes commissions, fees, taxes, liquidity, and account restrictions.

Common mistake: Treating exercise as automatically better because an option is in the money. The better mechanical comparison is between exercise value, current option market value, settlement rules, remaining time value, and the investor’s exposure after the event.

Expiration, Automatic Exercise, and Exercise Style

Expiration is the deadline after which the option no longer provides an exercisable right. At expiration, in-the-money options may be subject to automatic exercise or exercise-by-exception rules, depending on the market, contract, broker, and clearing rules. Investors should treat these rules as contract and account mechanics, not as a universal outcome that applies identically across every option.

Exercise style also matters. American-style options can generally be exercised before expiration, subject to contract rules. European-style options are generally exercisable only at expiration. This distinction affects timing mechanics, assignment risk, and the way early exercise can or cannot occur.

Settlement method is another boundary. Physical settlement can result in delivery, purchase, or sale of the underlying. Cash settlement results in a cash adjustment rather than direct delivery of the underlying asset. Index options, equity options, ETF options, and other contracts can differ, so the contract specifications matter.

Early Exercise and Common Misunderstandings

Early exercise means using an exercisable option right before expiration. It is most relevant for American-style options. It can appear in contexts involving deep in-the-money contracts, dividend timing, financing considerations, settlement needs, or limited liquidity, but those contexts do not create a general rule that early exercise is preferable.

The common misunderstanding is to focus only on the strike price and ignore the option’s remaining market value. A contract may be in the money and still have extrinsic value. If that value can be realized by selling or closing the option, immediate exercise may not represent the same economic outcome.

Another misunderstanding is to ignore the writer side. A holder’s exercise decision can create assignment for a writer. Assignment can change share exposure, cash requirements, settlement obligations, and account risk. That is why exercise mechanics should be understood together with assignment mechanics rather than as a one-sided event.

How Investors Should Interpret Exercise Mechanics

Exercise mechanics show how an option contract can become a share position, sale obligation, purchase obligation, or cash settlement. The process changes exposure. It does not prove that the underlying asset is attractive, that the contract was priced well, or that the investor improved the outcome by exercising.

A useful interpretation separates four questions. First, what right does the holder have? Second, what obligation can the writer face? Third, what happens at expiration or under the contract’s exercise style? Fourth, how does premium value compare with immediate exercise value?

Investor-use boundary: Exercise option mechanics help explain rights, obligations, expiration, assignment, and settlement. They do not replace contract review, broker-specific rules, tax analysis, liquidity assessment, or personal suitability review.

FAQ

What does it mean to exercise an option?

To exercise an option means to use the right inside the contract. A call holder uses the right to buy the underlying at the strike price. A put holder uses the right to sell the underlying at the strike price. Cash-settled contracts use the contract’s cash settlement rules instead of share delivery.

Is exercise the same as assignment?

No. Exercise applies to the option holder using the contract right. Assignment applies to the option writer being required to fulfill the matching obligation. They are connected events from opposite sides of the option contract.

What happens when a call option is exercised?

When a call option is exercised, the holder uses the right to buy the underlying at the strike price, or receives the contract-defined cash settlement if the contract is cash-settled. The assigned call writer must meet the corresponding obligation.

What happens when a put option is exercised?

When a put option is exercised, the holder uses the right to sell the underlying at the strike price, or receives the contract-defined cash settlement if the contract is cash-settled. The assigned put writer must meet the corresponding obligation.

Is exercising always better than selling the option?

No. Exercising uses the contract right, while selling or closing exits the option position in the market. If the option still has extrinsic value, selling or closing may produce a different result than immediate exercise. The comparison depends on contract terms, market value, liquidity, costs, taxes, and account rules.