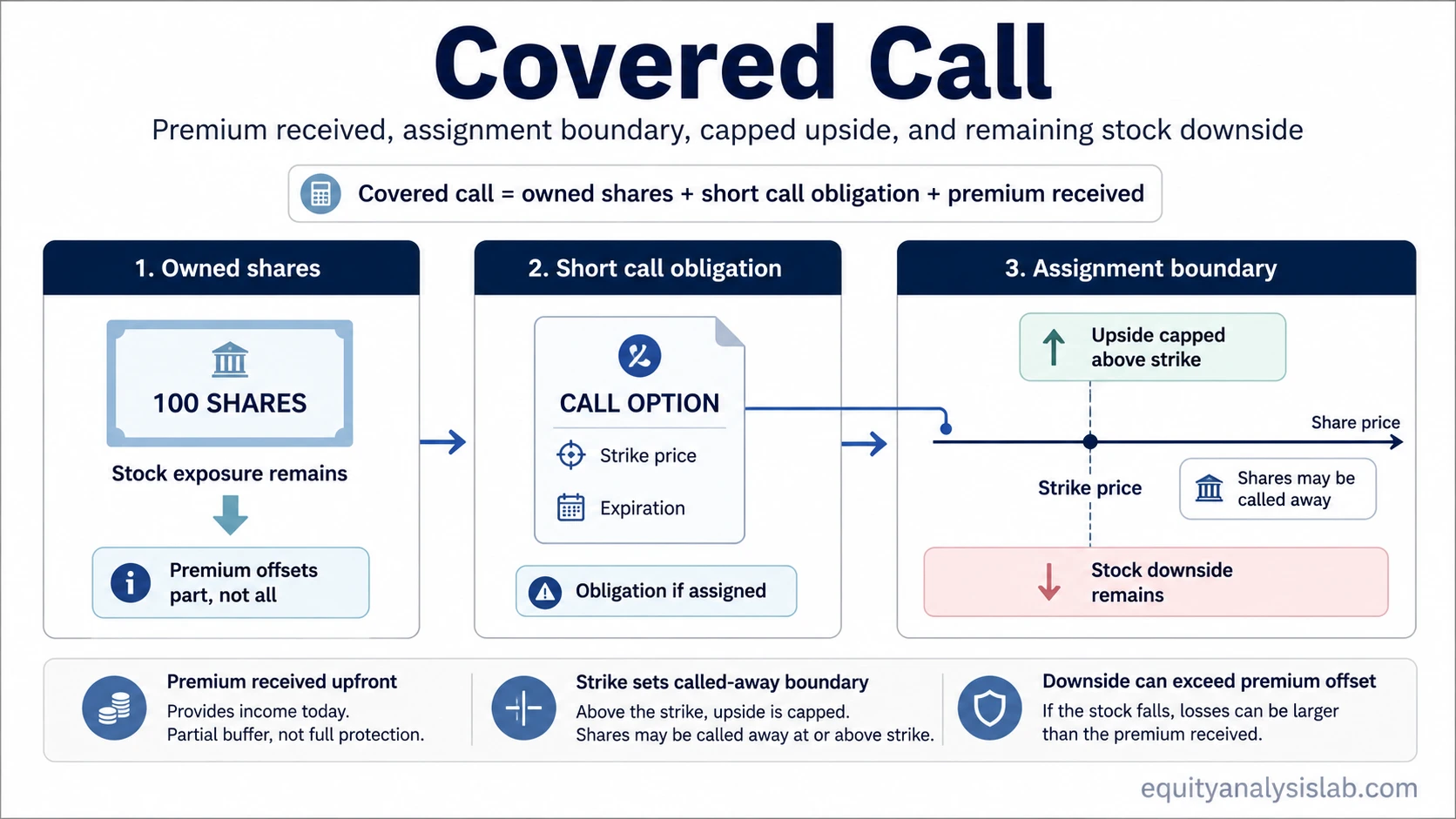

A covered call combines stock ownership with a short call option. The investor receives option premium, but the position still has capped upside above the strike price, possible assignment that can call shares away, and remaining downside exposure from the shares.

In a standard covered call on equity options, the investor owns 100 shares and sells one call option against those shares. The call buyer has the right to buy the shares at the strike price before or at expiration, while the covered call seller has the obligation to deliver shares if assignment occurs.

Definition: A covered call is an options position made from owned shares plus a short call option on those shares. The premium received changes the payoff boundary, but it does not remove the risk of owning the stock.

Key Points

- A covered call combines owned shares with a short call option.

- The premium received is a partial payoff offset, not full downside protection.

- Upside is capped above the strike price because assignment can require selling the shares.

- The investor still carries stock downside if the share price falls.

- Covered-call interpretation depends on the contract boundary: shares owned, strike, expiration, premium, and assignment terms.

Covered Call Contract Boundary

The contract boundary separates the stock position from the short-call obligation. Premium is only one part of that structure.

| Component | Role in a covered call | Risk boundary created |

|---|---|---|

| Own shares | The investor already holds the underlying stock. | Stock downside remains if the share price declines. |

| Sell call | The investor sells a call option against the owned shares. | The call seller takes on an obligation if assignment occurs. |

| Receive premium | The option premium is received upfront. | The premium offsets part of the share-price risk but does not eliminate it. |

| Strike price | The strike sets the price at which shares may be called away. | Upside above the strike is limited because the shares may need to be sold at the strike. |

| Expiration | The option has a defined expiration date. | The obligation exists during the life of the option and may still matter before expiration. |

| Assignment | If assigned, the investor delivers shares at the strike price. | The position can lose further stock upside after shares are called away. |

| Downside exposure | The investor continues to own the stock unless assignment removes the shares. | A large share-price decline can exceed the premium received. |

The seller’s obligation is different from the right held by a long call buyer. The buyer controls whether to exercise the right, while the covered call seller must be prepared for assignment if the option is exercised.

How a Covered Call Changes the Payoff

A covered call changes the stock payoff by adding premium and giving up some upside. The premium improves the outcome by the amount received, but gains above the strike are capped because the shares can be called away.

In simplified terms, the upside boundary is shaped by the strike price plus premium received, while downside remains tied to the stock decline after the premium offset.

| Stock outcome at expiration | Covered call effect | Main interpretation |

|---|---|---|

| Stock finishes below the strike | The call may expire without assignment. | The investor keeps the shares and the premium, while stock downside or upside depends on the share move. |

| Stock finishes above the strike | Assignment becomes more likely. | The shares may be sold at the strike, so upside above the strike is not fully retained. |

| Stock falls sharply | The premium offsets only part of the loss. | The investor can still lose money because the stock decline can exceed the premium received. |

The basic payoff logic is simple: premium received improves the starting point, the strike price sets the assignment boundary, and the stock position still drives most of the downside risk.

Limitation: Premium is a payoff adjustment, not a guarantee. A covered call can still underperform plain stock ownership if the stock rises far above the strike, and it can still lose money if the stock falls more than the premium received.

Covered Call Example

An investor owns 100 shares at $50 and sells one call option with a $55 strike for a $2 premium per share. The simplified example excludes commissions, taxes, bid-ask spread, early assignment details, and changes in option value before expiration.

Example setup: 100 shares are owned, one call is sold, the strike is $55, and $2 per share is received as premium. The premium reduces the effective stock exposure by $2 per share, but the position still depends on where the stock finishes relative to the strike.

| Expiration scenario | What happens | Payoff boundary |

|---|---|---|

| Stock at $52 | The call is below the $55 strike and may expire without assignment. | The investor keeps the premium and still owns shares, with the stock outcome shaped by the move from $50 to $52. |

| Stock at $60 | The call is above the $55 strike and assignment may require selling shares at $55. | The premium is retained, but upside beyond the strike is capped by the short call obligation. |

| Stock at $42 | The call may expire without assignment, but the shares have declined sharply. | The $2 premium offsets only part of the $8 share-price decline from $50 to $42. |

The numbers are illustrative only and do not recommend using a covered call. They separate the three main outcomes: shares remain below the strike, shares rise above the strike, or the stock loss exceeds the premium offset.

Clean, Weak, and Invalid Covered Call Interpretations

A covered call is easiest to understand when the premium, assignment boundary, and stock exposure are kept separate. Confusion usually starts when the premium is treated as if it changes every risk in the position.

| Interpretation quality | How it reads the position | Why it matters |

|---|---|---|

| Clean | The investor understands the owned shares, the short call obligation, the strike, the premium, and the assignment boundary. | The position is read as a capped-upside stock position with premium received. |

| Weak | The premium is treated as if it provides full protection against a stock decline. | The investor may underestimate how much downside remains in the shares. |

| Invalid | The covered call is framed as guaranteed income or low-risk stock ownership. | The description ignores capped upside, assignment risk, and the possibility that stock losses exceed premium received. |

Common mistake: The premium is received upfront, but the investor still owns the stock risk unless assignment removes the shares. Treating the premium as complete protection can make the downside look smaller than it really is.

Covered Call vs Nearby Option Structures

A covered call starts with owned shares and adds a short call. A cash-secured put starts from the opposite obligation: the investor sells a put and keeps cash available for a possible share purchase at the strike price.

A covered call also differs from a collar strategy, because a collar adds a protective put to define more of the downside boundary. A covered call by itself caps upside but does not add that put-based downside hedge.

Practical distinction: Covered calls, cash-secured puts, collars, and long calls all use option contracts, but they assign different rights, obligations, and risk boundaries. The covered call is defined by owned shares plus a short call, not by premium alone.

Covered Call Risks and Limits

A central covered call risk is that the investor still owns the stock downside while giving up some upside above the strike. The premium can improve the outcome by a limited amount, but it cannot prevent a large stock decline from creating a loss.

- Capped upside: If the stock rises far above the strike, the shares may be called away at the strike.

- Remaining downside: A falling share price can produce losses larger than the premium received.

- Assignment risk: Assignment can require the investor to sell the shares under the option contract terms.

- Early assignment nuance: Some contracts may be assigned before expiration, so expiration is not the only relevant date.

- Changing option value: Before expiration, the short call’s value can change with stock price, time, implied volatility, and liquidity conditions.

Covered-call analysis should stay focused on the contract terms and the stock exposure. Tax treatment, account rules, and brokerage execution details require separate review and are not part of the simplified payoff explanation.

FAQ

What is a covered call?

A covered call is an options position made from owned shares plus a short call option on those shares. The investor receives premium but accepts capped upside and possible assignment.

Can a covered call lose money?

Yes. A covered call can lose money if the stock falls by more than the premium received. The premium offsets part of the decline, but it does not remove stock downside exposure.

What happens if the stock rises above the strike price?

If the stock rises above the strike price, assignment becomes more likely. The investor may have to sell the shares at the strike, which caps further upside beyond that boundary.

Is the premium from a covered call guaranteed profit?

No. The premium is received upfront, but the total position can still lose money if the stock declines enough. Premium should be read as a partial payoff offset, not guaranteed profit.

How many shares does one covered call usually cover?

For standard listed equity options, one option contract usually represents 100 shares. Contract terms can vary, so the contract specification should be checked before relying on that convention.