A collar option strategy combines an existing stock position with a protective put and a covered call to create a defined downside floor and an upside ceiling around the shares.

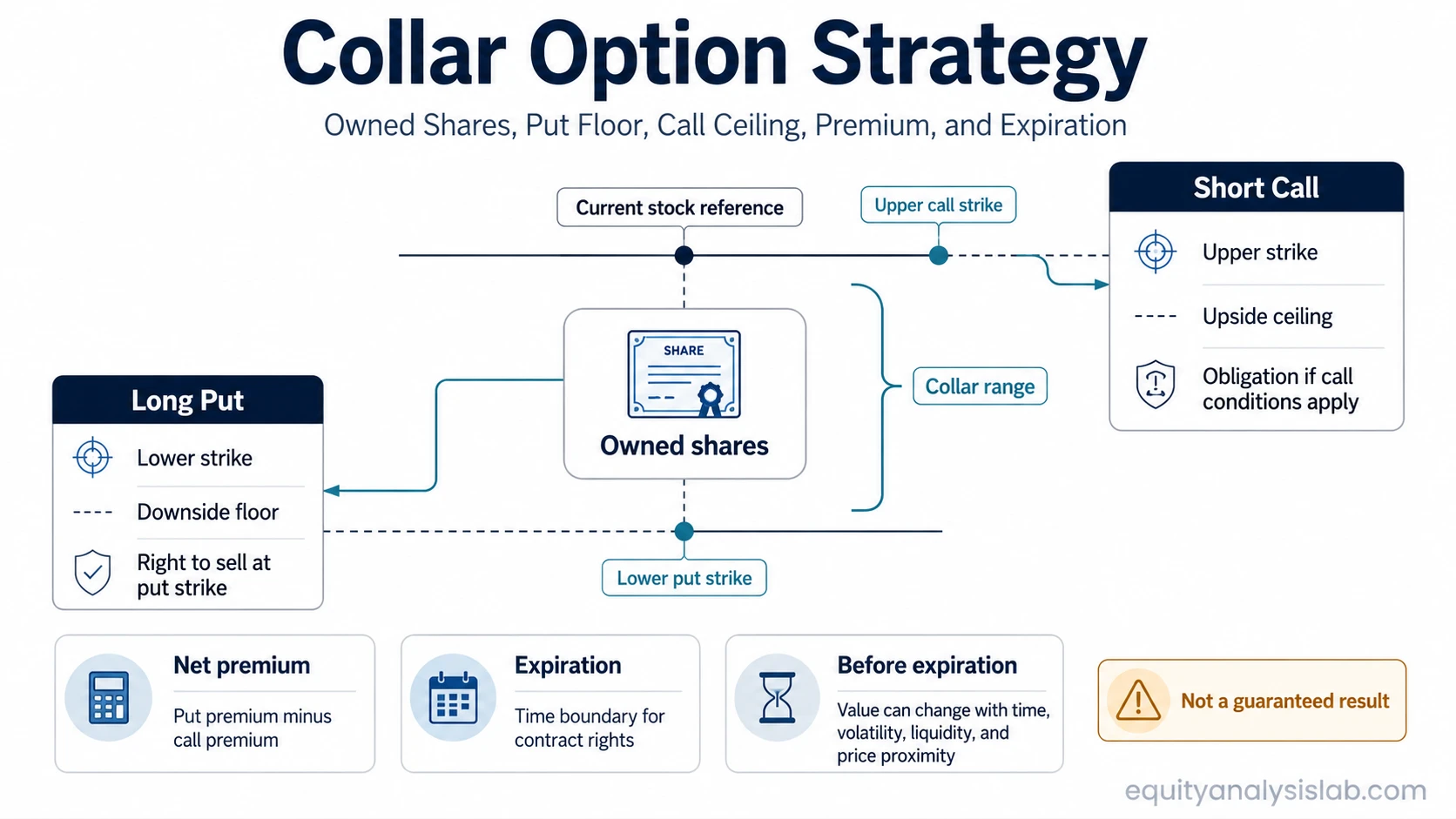

Definition: A collar option strategy is an options structure built around shares already held. The investor owns the shares, buys a put option below the current stock price, and sells a call option above the current stock price, usually with the same expiration date.

The long put creates the lower strike reference because it gives the right to sell shares at the put strike. The short call creates the upper strike reference because it creates an obligation if the stock trades above the call strike. The call premium may offset some or all of the put premium, but the tradeoff is capped upside and contract risk.

A collar can be read as a payoff boundary structure. The visible payoff line at expiration is only one part of the interpretation. Premium balance, time left, implied volatility, liquidity, and assignment or exercise conditions can change how the collar is interpreted before expiration.

Key Points

- A collar combines owned shares, a protective put, and a covered call.

- The put strike creates a downside floor, while the call strike creates an upside ceiling.

- The call premium can reduce the net cost of the put, but it does not remove opportunity cost or contract risk.

- Expiration, implied volatility, liquidity, and assignment or exercise risk affect interpretation before expiration.

- A collar defines a range of outcomes; it does not guarantee a specific investment result.

What Is a Collar Option Strategy?

A collar option strategy is a protective options structure around shares that are already owned. It keeps the stock position at the center, then adds one long put and one short call around that position.

The lower strike is usually the put strike. If the stock falls below that level by expiration, the put can limit downside in mechanical payoff terms, subject to premium, liquidity, exercise, and assignment details. The upper strike is usually the call strike. If the stock rises above that level, the short call can cap further stock participation because the shares can become subject to assignment or call-away mechanics.

This structure differs from a standalone protective put because the call sale changes the upside profile. It also differs from a standalone covered call because the collar includes a long put that defines a lower floor.

How a Collar Combines a Protective Put and Covered Call

The collar has three core parts. Each part changes the payoff map in a different way, so the structure should not be reduced to a single premium number.

| Component | Position in the collar | Contract role | Main interpretation |

|---|---|---|---|

| Owned shares | Long stock position | Creates the underlying exposure | The collar is built around shares already held, not around a standalone option-only position. |

| Long put | Put strike below the stock price in a common collar layout | Creates the lower floor | The put can reduce downside exposure below the put strike, after considering net premium and contract conditions. |

| Short call | Call strike above the stock price in a common collar layout | Creates the upper ceiling | The call premium can offset put cost, but the call can cap upside above the call strike. |

| Expiration | Often the same date for both options | Sets the time limit | The collar’s final payoff is usually read at expiration, while interim value can move with time and volatility. |

A standard collar often uses one put and one call with the same expiration because that makes the lower and upper references easier to compare. Longer-dated options can change the time exposure, which is why expiration structure should be separated from the collar definition itself. Longer-dated contracts such as LEAPS raise a separate time-horizon question rather than changing the basic collar mechanics.

Collar Payoff Boundary: Floor, Ceiling, Premium, and Expiration

The payoff range comes from the relationship between the stock price, put strike, call strike, and net premium. The put strike defines the lower contract reference. The call strike defines the upper contract reference. The net premium adjusts the economic result, but it does not remove the floor-and-ceiling structure.

| Payoff item | How it is read | Why it matters |

|---|---|---|

| Downside floor | Usually linked to the long put strike | The put can limit further downside below its strike in expiration payoff terms, before costs and practical frictions are considered. |

| Upside ceiling | Usually linked to the short call strike | The call can cap participation above its strike because the shares can become subject to assignment or call-away mechanics. |

| Net premium | Put premium paid minus call premium received | A debit collar has a net cost; a credit collar receives net premium; a near-zero-cost collar still has opportunity cost and risk. |

| Breakeven reference | Stock cost basis adjusted by net premium | The premium balance changes the economic reference point even when the strike references stay fixed. |

| Maximum gain | Generally limited above the call strike, adjusted for cost basis and net premium | The short call prevents the position from behaving like uncapped long stock above the call strike. |

| Maximum loss | Generally limited below the put strike, adjusted for cost basis and net premium | The put can define the lower payoff reference, but the realized result still depends on contract handling and market conditions. |

| Expiration | The date when the option rights and obligations end | The final payoff range becomes clearest at expiration, while interim values can change before then. |

A zero-cost collar means the call premium approximately offsets the put premium at entry. That phrase should not be read as costless protection. The investor gives up upside above the call strike, faces assignment risk, and may still be affected by spreads, liquidity, and taxes depending on the account and jurisdiction.

What Investors Can Observe Before Interpreting a Collar

The observable inputs matter because the same expiration payoff shape can have different risk meaning before expiration. A collar with wide spreads, little open interest, short time remaining, or a call strike near the stock price does not behave the same as a cleaner structure with more time and tighter markets.

| Observable input | What to check | Interpretation risk |

|---|---|---|

| Underlying stock price | Where the stock trades relative to the put and call strikes | The closer price moves to either strike, the more the collar behaves around that contract reference. |

| Stock position and cost basis | Share quantity and adjusted reference cost | The payoff math depends on the stock position being hedged and the premium adjustment. |

| Put strike | Distance between current price and lower strike | A lower put strike leaves more downside before the floor begins to matter. |

| Call strike | Distance between current price and upper strike | A lower call strike may create a tighter upside ceiling. |

| Put and call premiums | Net debit, net credit, or near-zero premium balance | Premium affects breakeven and opportunity cost, not just cash paid or received at entry. |

| Expiration date | Time remaining on both option contracts | Shorter time can make assignment, exercise, and price proximity more important. |

| Implied volatility | Whether premiums are elevated or compressed | Higher implied volatility can raise both put cost and call premium, changing the premium offset. |

| Liquidity | Bid-ask spread, open interest, and trading activity | Wide spreads can make the theoretical payoff less representative of practical execution value. |

| Assignment and exercise conditions | Whether either option is near or beyond its strike, especially near expiration | Rights and obligations become more active concerns when the stock trades near the contract references. |

This observable-inputs view is useful because the collar is not only a final payoff diagram. Time decay, volatility changes, and price movement toward either strike can change how the structure is valued before the options expire.

Simple Collar Option Strategy Example

An investor owns 100 shares at a reference price of 100. A collar is added with a long 95 put and a short 110 call using the same expiration. The put premium is 3 and the call premium received is 2, so the net premium cost is 1 before commissions, fees, and spread effects.

Example mechanics: The 95 put defines a lower expiration reference because it gives the right to sell at 95. The 110 call defines an upper expiration reference because shares may be subject to assignment or call-away mechanics above 110. The net premium cost of 1 adjusts the economic result, so the collar is not evaluated only by the two strike prices.

Before expiration, the same collar can be interpreted differently if the stock trades close to either strike because time value, volatility, liquidity, and assignment conditions become more relevant near the contract references.

If the stock is below 95 at expiration, the put can define the lower payoff reference, adjusted for the original stock reference and net premium. If the stock is above 110 at expiration, the short call can define the upper payoff reference. If the stock remains between the two strikes, the shares remain inside the collar range, while the net option premium still affects the result.

This example is mechanical and illustrative only. Actual outcomes can differ because commissions, bid-ask spreads, early assignment, exercise decisions, tax treatment, and contract handling can affect the realized result.

Collar Strategy Risks and Limitations

A collar can define a downside and upside range, but it should not be read as a guarantee. The structure reduces some downside exposure below the put strike while giving up stock participation above the call strike.

Key limitation: The premium offset is not the same as free protection. A call premium can help pay for the put, but the call also creates an upper ceiling and possible assignment obligation.

| Common mistake | Why it is incomplete | Cleaner interpretation |

|---|---|---|

| Calling the collar risk-free protection | The collar still has opportunity cost, premiums, spreads, and contract obligations. | Read it as a defined payoff range, not as a guaranteed outcome. |

| Focusing only on the put | The short call changes the upside and assignment profile. | Read the put and call together with the stock position. |

| Ignoring expiration | The structure can behave differently before expiration than it does on an expiration payoff chart. | Separate final payoff from interim value, time decay, and volatility effects. |

| Assuming the call premium eliminates all cost | Reduced cash outlay can come with capped upside and assignment risk. | Compare premium savings with the economic value given up above the call strike. |

| Ignoring liquidity | Wide spreads can change the practical value of opening, closing, or adjusting contracts. | Treat liquidity as an observable input, not as a minor detail. |

Tax treatment can also matter, but it is jurisdiction-specific and account-specific. Without a verified tax source and jurisdiction, tax language should remain a general caution rather than a rule.

Collar vs Nearby Option Structures

A collar can look similar to nearby option structures because it contains familiar components. The difference is that all three parts work together: owned shares, a long put, and a short call.

| Structure | Core parts | Main difference from a collar |

|---|---|---|

| Collar | Owned shares + long put + short call | Defines both a lower floor and an upper ceiling around an existing stock position. |

| Covered call | Owned shares + short call | Includes the upside ceiling from the short call, but does not add the protective put floor. |

| Protective put | Owned shares + long put | Includes the lower floor, but does not use a short call to offset premium or cap upside. |

| Cash-secured put | Short put backed by cash | A cash-secured put is a different short-put obligation structure, not a stock position protected by a long put and capped by a short call. |

The practical distinction is that a collar starts with stock ownership and adds both a lower and upper contract reference. Nearby structures explain individual legs or different obligations, but the collar’s identity comes from the combined floor-and-ceiling design.

FAQ

Why does a collar cap upside?

A collar caps upside because the short call creates an obligation above the call strike. If the stock rises beyond that strike, the shares may be subject to assignment or call-away mechanics, or the call position may need to be addressed.

Is a zero-cost collar actually free?

No. A zero-cost collar usually means the call premium roughly offsets the put premium. It can still involve capped upside, spreads, assignment risk, and opportunity cost.

How is a collar different from a protective put?

A protective put combines stock ownership with a long put. A collar adds a short call, which can reduce net premium cost but also creates an upside ceiling.