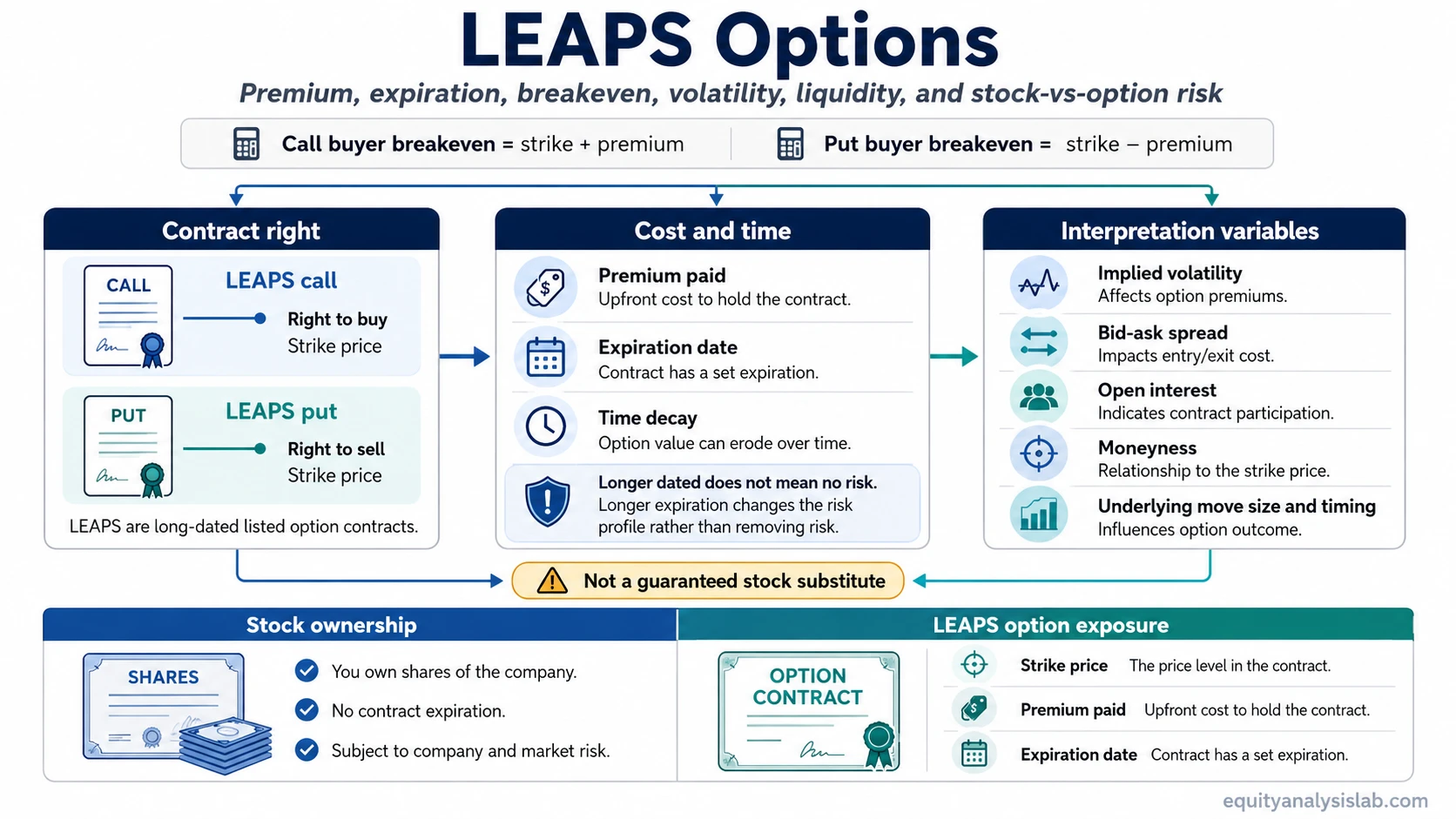

LEAPS options are long-dated call or put option contracts that give the holder option exposure for a longer period than standard listed options. They can be used to express equity exposure or hedge equity exposure, but they are still options: they have a strike price, an expiration date, a premium, and contract-specific risks.

Definition: LEAPS stands for Long-Term Equity Anticipation Securities. In practical options language, LEAPS are long-dated listed options on stocks or ETFs. A LEAPS call gives the holder the right to buy the underlying at the strike price, while a LEAPS put gives the holder the right to sell the underlying at the strike price.

The longer expiration gives the contract more time, but it does not make the option a lower-risk version of owning the underlying shares. It shifts the risk profile into premium cost, time decay, implied volatility, liquidity, and the size and timing of the underlying move.

Key Points

- LEAPS options are long-dated call or put contracts tied to an underlying stock or ETF.

- A LEAPS call gives the right to buy; a LEAPS put gives the right to sell.

- The buyer’s maximum loss is generally the premium paid, but that premium can still be substantial.

- Longer expiration usually slows time decay compared with short-dated options, but it does not eliminate decay.

- Implied volatility changes can affect the option even when the underlying moves in the expected direction.

- Liquidity depends on the specific contract, including strike, expiration, bid-ask spread, and open interest.

How LEAPS Options Work

A LEAPS contract has the same basic parts as other listed options. The difference is the longer expiration. That longer life changes how the premium is priced and how the contract reacts to time, volatility, and movement in the underlying security.

A long-dated option may feel closer to stock exposure because it can remain open for a longer period, but it is not stock ownership. The holder does not own the underlying shares unless the option is exercised and shares are delivered under the contract terms.

| Contract element | What it means | Interpretation limit |

|---|---|---|

| Underlying | The stock or ETF connected to the option contract. | A favorable move in the underlying does not guarantee a favorable option result. |

| Strike price | The price at which the holder has the right to buy or sell. | Strike selection changes premium, sensitivity, and breakeven. |

| Expiration | The date after which the option no longer has value or rights. | More time can reduce urgency, but expiration risk still remains. |

| Premium | The price paid by the buyer and received by the seller. | A higher premium requires a larger favorable move before the position becomes economically attractive. |

| Implied volatility | The market’s pricing of expected future movement. | Falling implied volatility can reduce option value even if the underlying moves favorably. |

| Liquidity | The ease of entering or exiting a specific contract. | Thin open interest or wide bid-ask spreads can make the contract harder to trade efficiently. |

| Exercise / assignment | The contract rights and obligations connected to converting the option into an underlying share transaction. | Exercise and assignment mechanics depend on the contract and position structure; they should not be treated as automatic investment decisions. |

LEAPS Calls vs LEAPS Puts

LEAPS calls and LEAPS puts use the same long-dated option structure, but the contract right points in opposite directions.

| Type | Contract right | Basic risk boundary for the buyer | Common interpretation |

|---|---|---|---|

| LEAPS call | Right to buy the underlying at the strike price. | Premium paid can be lost if the contract does not retain value by expiration. | Long-dated upside exposure, not direct stock ownership. |

| LEAPS put | Right to sell the underlying at the strike price. | Premium paid can be lost if the contract does not retain value by expiration. | Long-dated downside exposure or hedge exposure, not guaranteed protection. |

For a buyer, the cleanest generic boundary is premium paid. For a seller, the risk depends on the full position structure, collateral, assignment obligation, and whether the option is covered, cash-secured, or uncovered.

LEAPS vs Stock

LEAPS can create exposure with less upfront capital than buying shares outright, but the tradeoff is expiration, premium risk, and sensitivity to option pricing variables. Direction alone does not settle the choice between stock exposure and option exposure.

| Feature | Stock ownership | LEAPS option exposure |

|---|---|---|

| Ownership | Represents ownership of shares. | Represents a contract right, not share ownership. |

| Capital outlay | Usually requires paying the share price. | Requires paying the option premium. |

| Expiration | No expiration date for the share position itself. | Expires on a fixed date. |

| Dividends and voting | Shareholders may receive dividends and voting rights when applicable. | Option holders generally do not receive shareholder rights unless shares are acquired through exercise. |

| Maximum loss for buyer | The share value can decline substantially, potentially to zero. | The premium paid can be lost. |

| Volatility sensitivity | Share value is not priced directly through implied volatility. | Option value can change when implied volatility changes. |

| Liquidity | Depends on the underlying market. | Depends on the exact strike, expiration, spread, and open interest. |

Premium, Breakeven, Time Decay, and Volatility

The premium is central to LEAPS risk. A longer expiration usually means more time value, which can make the contract more expensive than a shorter-dated option. That extra time can be useful, but it also raises the amount that must be recovered before the position becomes economically favorable.

Generic buyer mechanics: For a call buyer, breakeven at expiration is commonly described as strike price plus premium paid. For a put buyer, breakeven at expiration is commonly described as strike price minus premium paid. These formulas simplify the contract economics and do not account for every real-world factor such as spreads, commissions, early exercise considerations, or changing implied volatility before expiration.

Time decay is usually slower for longer-dated options than for short-dated options, especially far from expiration, but it still exists. As expiration approaches, time value can erode more visibly if the underlying move has not been large enough or fast enough.

Implied volatility can create a second source of disappointment. A stock or ETF can move in a favorable direction while the LEAPS contract gains less than expected if implied volatility falls, the move is too small relative to the premium, or the contract remains far from intrinsic value.

Liquidity is also contract-specific. A widely followed underlying can still have a particular LEAPS strike or expiration with a wide bid-ask spread, limited open interest, or poor exit flexibility.

LEAPS Observables and Interpretation Limits

A LEAPS contract should be read through several observable variables at the same time. No single variable explains the full risk profile.

| Observable | What to check | What it cannot prove alone |

|---|---|---|

| Underlying price | Whether the stock or ETF is moving toward or away from the strike. | It cannot prove the option will gain enough after premium, time, and volatility effects. |

| Moneyness | Whether the option is in the money, at the money, or out of the money. | It cannot show whether the premium is attractive or whether liquidity is acceptable. |

| Time to expiration | How much time remains for the underlying move to develop. | It cannot remove the possibility that the thesis develops too slowly. |

| Premium | How much capital is at risk for the buyer. | It cannot show whether the option is cheap or expensive without volatility and scenario context. |

| Implied volatility | How much expected movement is already priced into the contract. | It cannot predict the direction of the underlying security. |

| Delta | How sensitive the option may be to a move in the underlying. | It cannot eliminate premium, volatility, or liquidity risk. |

| Open interest and spread | Whether the exact contract appears liquid enough for practical execution. | It cannot guarantee a clean entry or exit at the displayed price. |

Simple LEAPS Options Example

A stock advances over several months, but the move is gradual and smaller than the premium embedded in a long-dated call. At the same time, implied volatility falls because the market begins pricing less future movement. The underlying has moved in the expected direction, yet the option result can still disappoint because the contract needed a larger move, a faster move, or more favorable volatility conditions.

The same logic can affect long-dated puts. A decline in the underlying may not be enough if the premium was high, the move arrives late, or volatility changes reduce the option’s remaining value. LEAPS analysis therefore separates the market view from the option contract used to express that view.

Common Mistakes With LEAPS Options

Mistake: Treating long expiration as the same thing as low risk. More time changes how risk appears through premium, decay, volatility, and liquidity. It does not make the contract safe by itself.

Limitation: Direction is only one part of the contract. Premium paid, time remaining, implied volatility, moneyness, and contract liquidity can all change the result.

Deep in-the-money, at-the-money, and out-of-the-money LEAPS can behave very differently. A deeper in-the-money contract may track the underlying more closely, while an out-of-the-money contract may depend more heavily on a large move before expiration. That distinction is mechanical; it should not be converted into a universal rule for which contract is best.

Related Options Structures

A cash-secured put differs from a LEAPS put because the cash-secured structure centers on a short put obligation backed by reserved cash.

A collar structure combines option legs around an existing position to define a different hedge and upside boundary.

A covered call obligation involves owned shares and a short call, so its risk and assignment boundary differ from simply holding a long-dated call or put.

FAQ

What are LEAPS options?

LEAPS options are long-dated listed call or put option contracts. They give the holder a contract right tied to a strike price and expiration date, but they do not create stock ownership by themselves.

Are LEAPS options the same as owning stock?

No. Stock ownership represents ownership of shares. A LEAPS option is a contract right with an expiration date, premium cost, and option-pricing risks such as time decay and implied volatility changes.

Can a LEAPS option lose value if the stock moves in the expected direction?

Yes. The move may be too small, too slow, or offset by falling implied volatility. Bid-ask spreads and contract liquidity can also affect the practical result.

What is the main risk for a LEAPS buyer?

The buyer can lose the premium paid if the contract does not retain value by expiration or cannot be exited at a favorable enough price before expiration.