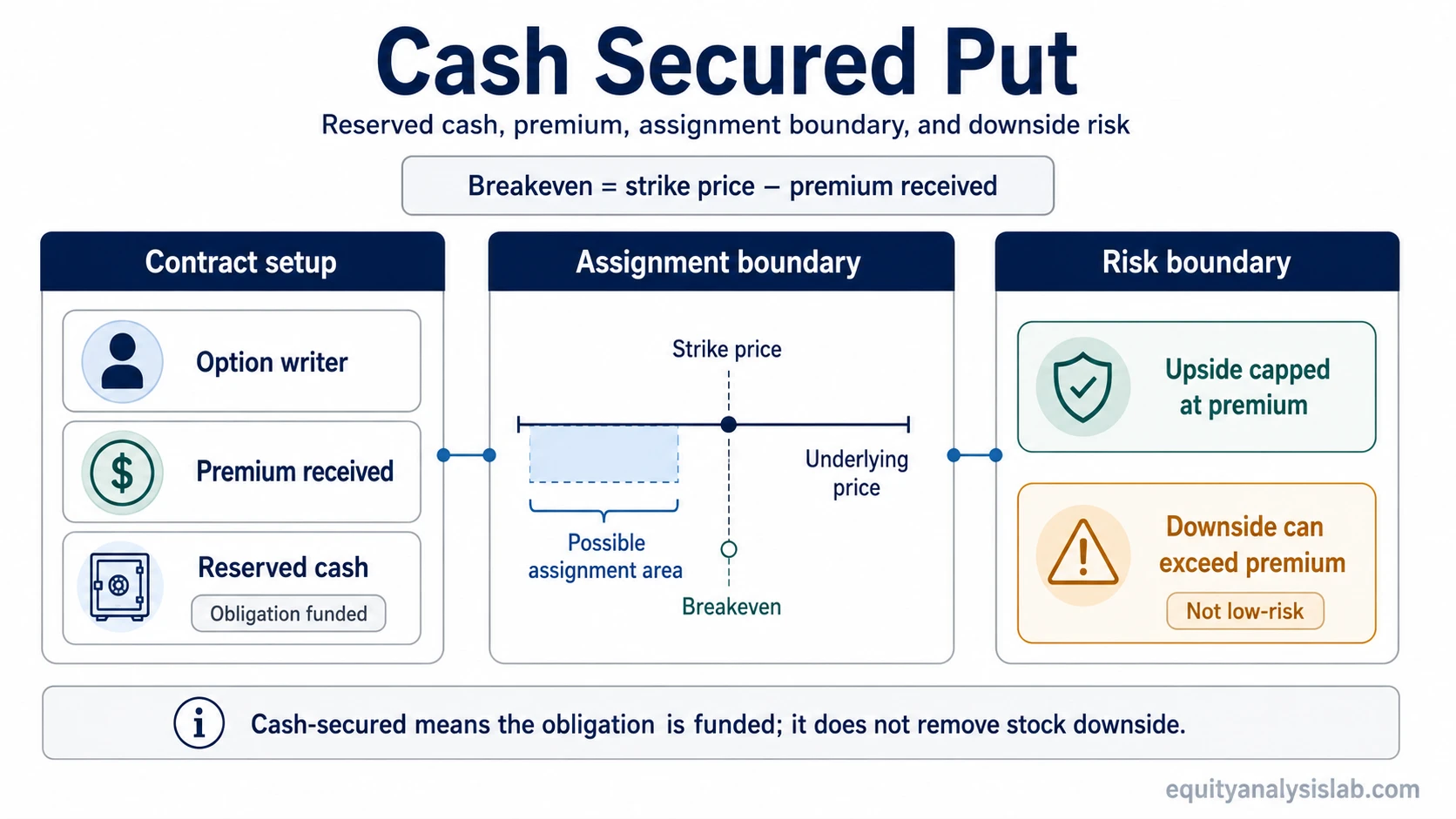

A cash secured put is a short put position where the seller sets aside enough cash to buy the underlying shares at the strike price if assignment occurs. The seller receives an option premium, but the cash reserve does not make the position risk-free.

The structure is called cash secured because the possible purchase obligation is backed by cash rather than left uncovered. The key terms are the put option sold, the strike price, the expiration date, the premium received, and the possible assignment obligation if the option is exercised.

Definition: A cash secured put is a put option sold by an investor who keeps enough cash available to purchase the underlying shares at the strike price if assigned. The position lets the seller receive premium, but its main risk is that the seller may end up owning shares whose market value has fallen below the effective purchase price.

Key points about a cash secured put

- A cash secured put is a seller-side put structure backed by reserved cash.

- The seller receives a premium, but may be assigned and required to buy shares at the strike price.

- Breakeven is usually calculated as strike price minus premium received, before commissions, fees, taxes, or financing effects.

- Maximum gain is limited to the premium received if the option expires out of the money.

- Downside risk can remain large if the underlying stock falls sharply below the breakeven level.

What a cash secured put includes

A cash secured put has two parts: the short put contract and the cash reserve behind it. The put seller receives premium for taking on the obligation to buy shares at the strike price if assignment occurs.

| Component | What it means | Why it matters |

|---|---|---|

| Put seller / writer | The investor who sells the put contract and receives the premium. | This side carries the possible obligation to buy the shares if assigned. |

| Cash reserve | Cash set aside to cover the potential share purchase at the strike price. | It covers the purchase obligation but does not protect against a falling share price after assignment. |

| Strike price | The price at which the seller may have to buy the shares. | It defines the assignment price and is central to the breakeven calculation. |

| Expiration | The date when the option contract expires if it has not already been exercised or closed. | Time remaining affects option value, assignment risk, and how much uncertainty remains. |

| Premium | The amount received for selling the put. | It is the seller’s maximum potential gain, but only a partial cushion against losses. |

| Assignment | The event where the seller is required to buy the underlying shares at the strike price. | Assignment turns the option obligation into stock ownership at the contract price. |

How a cash secured put works

The seller writes a put option and receives premium. In exchange, the seller accepts the possibility of buying the underlying shares at the strike price if the option is assigned. The reserved cash is there to fund that potential purchase.

If the stock stays above the strike price through expiration, the put will usually expire out of the money, and the seller keeps the premium. If the stock falls below the strike price, assignment becomes more likely, and the seller may have to buy shares for more than their market value at that time.

This is why a cash secured put is related to a short put structure. The difference is not the put obligation itself; it is the presence of cash reserved to cover that possible obligation.

Payoff, breakeven, and downside boundary

The payoff of a cash secured put depends on the relationship between the stock price, the strike price, and the premium received. The premium improves the effective purchase price, but it does not eliminate the downside if the stock falls much further.

| Outcome area | Contract result | Economic interpretation |

|---|---|---|

| Stock price above strike at expiration | The put usually expires out of the money. | The seller generally keeps the premium as the maximum gain, before costs and taxes. |

| Stock price below strike at expiration | The put may be assigned. | The seller may have to buy shares at the strike even if the market price is lower. |

| Breakeven area | Breakeven is commonly strike price minus premium received. | Below that level, the premium no longer offsets the decline, before costs and taxes. |

| Maximum gain | Limited to the premium received. | The upside is capped because the seller does not participate in stock gains beyond the premium. |

| Downside boundary | Losses can grow as the stock falls below breakeven. | The risk can resemble owning the stock from the effective cost basis, with large downside if the stock collapses. |

The simplified breakeven formula is:

Breakeven = strike price − premium received

This formula is a simplified educational version. Actual results can differ after commissions, fees, taxes, early exercise, liquidity, and execution prices.

Why cash-secured does not mean low-risk

The word cash-secured describes how the obligation is funded. It does not describe the quality of the underlying stock, the size of the possible loss, or whether the option premium is attractive enough for the risk being accepted.

Main limitation: Premium reduces the effective purchase price, but it does not stop the stock from falling below that level. If assignment occurs and the stock keeps declining, the seller can face losses even though the put was fully cash secured.

Assignment is also not automatically a favorable outcome. It may be acceptable only in a scenario where the seller is willing and able to own the shares at the effective cost basis. Even then, the final result depends on the future value of the stock, not just on the fact that premium was received.

A simple cash secured put example

A simple illustration is a put sold with a $50 strike price and $2 of premium received. The simplified breakeven is $48 before costs. If the option is assigned, the seller may have to buy the shares at $50, while the premium reduces the effective cost basis to $48.

If the stock is above $50 at expiration, the put may expire without assignment, and the premium is the seller’s maximum gain. If the stock falls to $42, the $2 premium does not remove the loss. The seller may own shares with a market value well below the effective cost basis.

This example is illustrative only. It does not represent a real company, a real market event, or a recommendation to use the structure.

How a cash secured put differs from related put concepts

A cash secured put sits inside the broader put-option family, but it should not be confused with buyer-side put positions or hedging structures.

| Concept | Main role | Boundary with a cash secured put |

|---|---|---|

| Cash secured put | Seller-side put backed by reserved cash. | The seller receives premium and may be assigned to buy shares. |

| long put | Buyer-side put position. | The buyer pays premium for downside exposure, rather than receiving premium and accepting assignment risk. |

| protective put | Hedging structure used with an existing long stock position. | A protective put position is used to limit downside on shares already owned; a cash secured put can create a future share purchase obligation. |

| Naked put | Short put without full cash backing. | The put obligation may be similar, but the funding and margin context differs. |

A covered call can sometimes be compared with a cash secured put because both can express a willingness to own or sell shares around a price level. That comparison should remain separate from the core definition because a cash secured put is still a put-selling structure, not a covered-call position.

Common mistakes with cash secured puts

Mistake 1: Treating premium as guaranteed income. Premium is received upfront, but the final economic result depends on assignment, stock movement, execution costs, and the effective cost basis.

Mistake 2: Treating collateral as protection from loss. Cash collateral funds the potential purchase. It does not hedge the value of the shares after assignment.

Mistake 3: Ignoring liquidity and bid-ask spreads. A quoted option price may not be easy to realize if the contract has weak liquidity, wide spreads, or limited displayed size.

Mistake 4: Ignoring volatility and time value. Option premium can change as implied volatility, time to expiration, and the underlying price change. A premium that looks attractive in isolation may be compensating for higher uncertainty.

Mistake 5: Assuming assignment timing is fully predictable. Assignment risk can depend on option moneyness, expiration, dividends, liquidity, and holder behavior. The seller should not treat assignment as a perfectly controlled event.

When the structure is being interpreted correctly

A cash secured put is best understood as a contract structure with defined terms, not as a promise of safe yield. The useful questions are whether the strike, premium, expiration, assignment obligation, liquidity, and downside risk are being read together.

The phrase cash-secured answers only one question: whether cash is available for possible assignment. It does not answer whether the underlying shares are attractive, whether the premium is sufficient, whether the risk is appropriate, or whether the position belongs in a portfolio.

FAQ

What is a cash secured put?

A cash secured put is a short put backed by enough reserved cash to buy the underlying shares at the strike price if assignment occurs. The seller receives premium but accepts a possible purchase obligation.

What is the breakeven on a cash secured put?

The simplified breakeven is the strike price minus the premium received, before commissions, fees, taxes, and other costs. If the stock falls below that level, losses can exceed the premium received.

Is a cash secured put risk-free?

No. Cash-secured means cash is reserved for possible assignment. It does not mean the stock cannot fall, that assignment will be favorable, or that the premium removes downside risk.