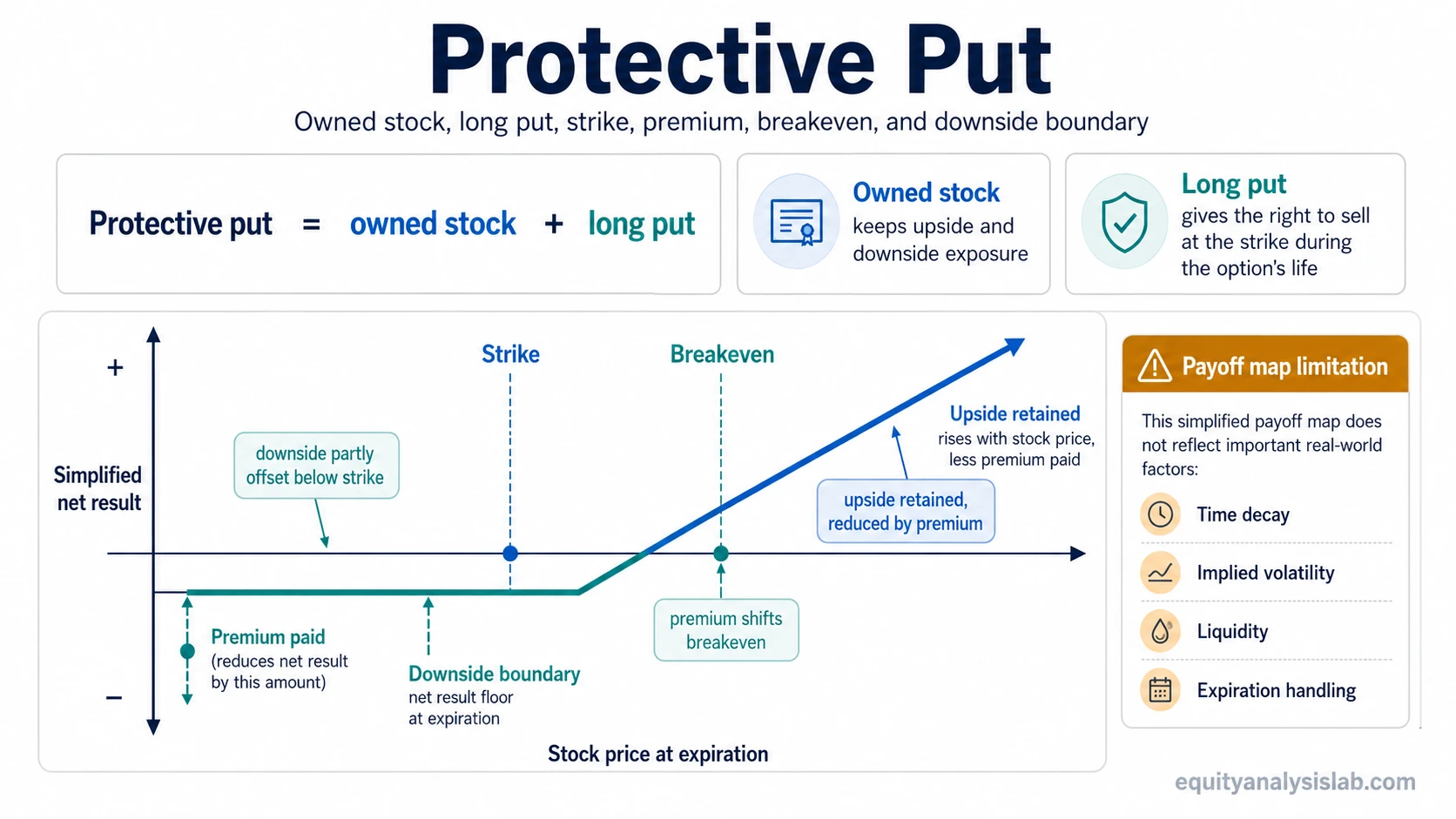

A protective put is an options hedge made by owning the underlying shares and buying a put option on those shares. The stock position keeps upside exposure, while the long put creates a defined downside boundary until the option expires.

Protective put definition: a protective put combines a long stock position with a long put option. The put gives the holder the right, but not the obligation, to sell the shares at the strike price before or at expiration, depending on the option style and contract terms.

The structure is protective because the put can offset part of the stock loss if the underlying price falls below the strike. It is not free protection. The investor pays a premium, and that premium changes the breakeven point, the maximum loss calculation, and the return profile if the stock does not fall.

Key Points About a Protective Put

- A protective put requires an owned underlying position plus a long put option.

- The strike price marks the level where the put begins to provide direct downside value at expiration.

- The premium is the cost of the hedge and usually lowers the net return if the stock rises or stays flat.

- The breakeven depends on the stock cost basis plus the put premium when the stock and put are entered together.

- The hedge is temporary because the put has an expiration date and can lose value through time decay.

What Is a Protective Put?

A protective put is an options structure, not a standalone bearish bet. The defining feature is that the investor already owns, or simultaneously buys, the underlying shares and then buys a put option to limit part of the downside risk.

The long put creates a contractual right to sell at the strike price. If the stock falls below that strike, the put can increase in value and offset some of the decline in the shares. If the stock rises, the investor still owns the shares, but the put premium remains a cost that reduces the net result.

A protective put is therefore different from a standalone long put. A long put can be used without owning the stock. A protective put specifically attaches the put right to an existing or simultaneous long stock position.

How a Protective Put Works

The structure starts with two legs: the underlying shares and the put option. The shares provide participation if the stock rises. The put provides a potential exit price if the stock falls below the strike during the option’s life or at expiration, depending on the contract terms.

| Component | Role in the structure | Why it matters |

|---|---|---|

| Owned underlying | The investor holds the stock or other optionable underlying. | The position still participates in upside and downside movement. |

| Long put | The investor buys the right to sell the underlying at the strike. | The put creates the downside boundary if the underlying falls far enough. |

| Strike price | The price at which the put holder can sell the underlying. | The strike determines where the hedge begins to matter most at expiration. |

| Premium | The cost paid for the put option. | The premium reduces the net result and moves the breakeven level. |

| Expiration | The date when the option protection ends. | The hedge is temporary; after expiration, the put no longer protects the position. |

| Contract multiplier | The number of shares controlled by one option contract. | The hedge size must match the share exposure to avoid under- or over-hedging. |

The hedge does not remove all risk. It changes the shape of the risk. The investor gives up the premium in exchange for a defined contractual selling right during the option’s life.

Protective Put Payoff and Breakeven

At expiration, the payoff depends on the stock price relative to the strike and the premium paid. The put has the most obvious value when the stock finishes below the strike. Above the strike, the put may expire worthless, but the investor still owns the stock.

| Stock price at expiration | Put outcome | Protective put interpretation |

|---|---|---|

| Below the strike | The put is in the money. | The put can offset stock losses by giving the holder the right to sell at the strike. |

| Near the strike | The put may have limited or no intrinsic value. | The hedge may reduce some downside, but the premium still affects the net result. |

| Above the breakeven | The put usually expires worthless. | The stock gain can exceed the premium cost, leaving a positive net result. |

For a married-put style entry, where the stock and put are bought at the same time, the simplified breakeven is:

Breakeven = stock purchase price + put premium

For an investor who already owns the stock, breakeven depends on the original cost basis and how the hedge premium is being measured. A put bought long after the stock purchase does not change the original purchase price, but it does change the economics of the hedged position from that point forward.

A simplified maximum loss at expiration is often described as:

Simplified per-share maximum loss at expiration = stock cost basis − put strike + put premium

This formula assumes the put hedge matches the share position and ignores commissions, taxes, early exercise details, dividend effects, and execution friction. It is useful for understanding the structure, not for replacing contract-specific analysis.

Protective Put Example

Suppose an investor owns shares bought at $50 and buys a put with a $45 strike for a $2 premium. In this simplified example, the breakeven for a simultaneous stock-plus-put entry would be $52.

| Expiration scenario | What happens | Simplified interpretation |

|---|---|---|

| Stock falls to $35 | The $45 put has intrinsic value. | The investor can use the put right to reduce the damage from the stock decline. |

| Stock ends near $45 | The hedge is near its strike boundary. | The premium still matters, so the position may lose money even if the put helped. |

| Stock rises to $60 | The put likely expires worthless. | The stock upside remains, but the $2 premium reduces the net gain. |

The hedge is not designed to create profit by itself; it changes how downside risk is shaped during the option’s life.

What the Payoff Map Does Not Show

A simple payoff map is useful because it shows the expiration boundary: downside is partly offset below the strike, upside remains open above the stock cost, and the premium shifts the net result. But a payoff map can hide several real option behaviors.

Payoff map limitation: a protective put payoff diagram usually shows expiration math. It does not fully show time decay, implied volatility changes, bid-ask spreads, early exercise choices, dividend effects, tax treatment, or what happens if the investor adjusts the hedge before expiration.

| Real-world factor | Why it matters | Common mistake |

|---|---|---|

| Time decay | The put can lose value as expiration approaches if the stock does not fall enough. | Assuming the hedge keeps the same value while time passes. |

| Implied volatility | Higher implied volatility can make puts more expensive; falling implied volatility can reduce option value. | Looking only at the strike and ignoring the price paid for the hedge. |

| Liquidity | Wide bid-ask spreads can increase practical hedge cost. | Treating theoretical option value as the same as executable value. |

| Expiration handling | The investor must understand what happens if the put is in the money, out of the money, or near the strike. | Waiting until expiration without understanding exercise and assignment mechanics. |

| Repeated hedge cost | Buying new puts repeatedly can become expensive over time. | Viewing each hedge in isolation instead of measuring cumulative premium cost. |

This is the main reason the structure should not be described as guaranteed safety. It can define a downside right for a period, but the premium, timing, volatility, and execution conditions decide how useful that right is in practice.

Expiration, Exercise, and Assignment

The holder of the protective put owns the right to exercise the put. That is different from being assigned on a short option. Assignment risk belongs to the party that is short the option, not to the investor who bought the protective put.

If the put is in the money near expiration, the investor may need to decide whether to exercise, sell the option, or allow the contract process to proceed according to broker and clearing rules. The correct handling depends on the option terms, account setup, dividend timing, and the investor’s objective.

If the put expires out of the money, the option may expire worthless. In that case, the investor still owns the stock, but the premium paid for the put becomes the cost of having carried the hedge.

Protective Put vs Nearby Option Structures

Protective puts are often confused with nearby option structures because several of them involve puts, stock ownership, or downside risk. The clearest distinction is whether the investor owns the stock, owns a put right, or has sold an option obligation.

| Structure | Main position | Key distinction |

|---|---|---|

| Protective put | Owned stock plus long put | Buys a downside selling right while keeping stock upside exposure. |

| Long put | Long put only, unless paired with another position | Can be a standalone bearish or hedging option; it does not require owned shares. |

| Married put | Stock and put bought together | Usually refers to buying the stock and put at the same time. |

| Collar | Owned stock, long put, and short call | Uses a short call to help offset put cost, but caps upside above the call strike. |

| Cash-secured put | Short put backed by cash | Creates an obligation to buy shares if assigned; it does not hedge an existing long stock position. |

A short put and a covered call also involve option obligations, but they are not protective puts. A protective put owns the downside right; it does not sell an obligation to someone else.

Protective Put vs Stop-Loss Order

A stop-loss order and a protective put can both be used to manage downside, but they work differently. A stop order attempts to trigger a sale when a price level is reached. A protective put is an option contract that gives the holder the right to sell at the strike during the option’s life.

The difference matters during gaps, fast markets, and volatile conditions. A stop order may execute at a different price than expected, while a put has its own premium cost, expiration date, and liquidity conditions. Neither tool removes the need to understand the position’s actual risk.

Common Protective Put Mistakes

A protective put can make risk look cleaner than it is if the investor focuses only on the strike. The strike is important, but the hedge also depends on premium, time remaining, volatility, and whether the contract size matches the stock exposure.

Common mistake: treating the put strike as a guaranteed final loss number without including the premium. The premium is part of the position economics, so the protected floor and the breakeven are not the same thing.

Another common mistake is assuming that buying a put after a large stock decline creates the same risk profile as buying it earlier. When implied volatility is high, the put may be expensive. In that case, the hedge may still limit further downside, but the cost can make the overall position less attractive.

FAQ

Does a protective put limit loss?

A protective put can limit part of the downside by giving the holder the right to sell at the strike price. The premium still counts as a cost, so the position is not loss-free.

Is a protective put the same as a long put?

No. A long put is the option leg itself. A protective put is a combined structure that pairs owned shares with a long put on those shares.

What is the breakeven for a protective put?

For a simultaneous stock-plus-put entry, the simplified breakeven is the stock purchase price plus the put premium. For an existing stock position, the breakeven depends on the original cost basis and how the hedge cost is measured.

What happens if the put expires worthless?

If the put expires worthless, the investor still owns the stock, but the premium paid for the put becomes the cost of the temporary hedge.

How is a protective put different from a collar?

A protective put owns stock and buys a put. A collar also adds a short call, which can reduce hedge cost but caps upside above the call strike.