A long put option is the purchase of a put contract that gives the holder the right, but not the obligation, to sell the underlying at the strike price before or at expiration, depending on the contract terms. The buyer pays a premium for that right, and that premium is the main defined loss boundary if the option expires worthless.

Long put option definition: a long put is a bought put option. It can increase in value when the underlying price falls, but the position must fall far enough to overcome the premium paid before the buyer reaches breakeven at expiration.

A long put is an option contract, not stock ownership and not a short stock position. The buyer controls downside exposure through the premium paid, while the payoff depends on the strike price, the underlying price, time remaining, implied volatility, and contract liquidity.

Long Put Option Key Points

- A long put gives the buyer the right to sell the underlying at the strike price.

- The buyer pays an option premium, which is normally the maximum loss before fees and commissions.

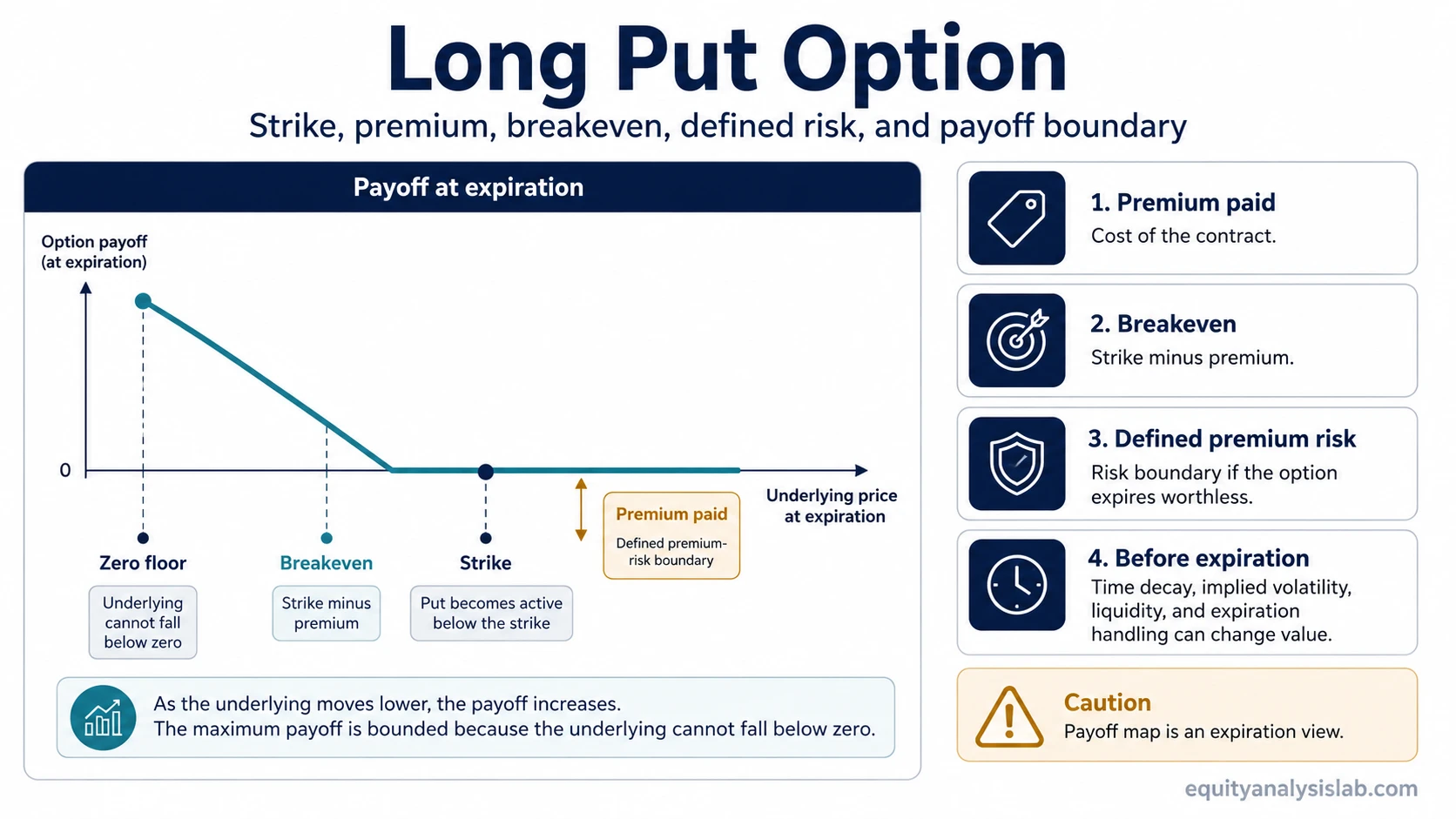

- The breakeven at expiration is the strike price minus the premium paid.

- The payoff improves as the underlying falls below breakeven, but the underlying cannot fall below zero.

- Time decay, implied volatility, liquidity, and expiration handling can change the risk before expiration.

How a Long Put Contract Works

A long put has a simple contract structure: the buyer pays a premium for the right to sell the underlying at a fixed strike price. That right has an expiration date, and the value of the option depends on how the underlying price compares with the strike before the contract expires.

| Input | What it controls | Why it matters |

|---|---|---|

| Underlying price | The market price of the asset tied to the option | Determines whether the put has intrinsic value relative to the strike. |

| Strike price | The price at which the put holder can sell the underlying | Creates the payoff boundary for the contract. |

| Premium paid | The cost of buying the option | Sets the main defined loss and shifts the breakeven lower. |

| Expiration date | The contract deadline | Limits how long the buyer has for the expected move or hedge effect to matter. |

| Implied volatility | The market’s pricing of expected movement | Can raise or lower the option’s value before expiration even if the underlying has not moved enough. |

| Liquidity | The ease of trading the contract near fair value | Wide bid-ask spreads or low open interest can affect the price available to close or adjust exposure. |

The contract is most direct at expiration: if the underlying is below the strike, the put has value equal to the difference between the strike and the underlying price. If the underlying is at or above the strike, the put expires out of the money and the buyer loses the premium paid, excluding fees or commissions.

Long Put Payoff and Breakeven

The breakeven for a long put at expiration is:

Breakeven = strike price − premium paid

Above the strike, the put has no intrinsic value at expiration. Between the strike and breakeven, the put has intrinsic value, but not enough to recover the full premium paid. Below breakeven, the position begins to show a net gain before fees because the intrinsic value exceeds the premium cost.

| Underlying price at expiration | Put status | Result for the long put buyer |

|---|---|---|

| Above the strike | Out of the money | The option expires worthless and the premium is lost. |

| At the strike | At the money | The option has no intrinsic value; the premium remains the loss. |

| Below the strike but above breakeven | In the money | The option has value, but not enough to offset the premium fully. |

| Below breakeven | In the money | The option’s intrinsic value exceeds the premium paid. |

The maximum loss is normally the premium paid, plus any fees or commissions. Profit potential increases as the underlying falls, but it is not unlimited because the underlying price cannot go below zero.

Long Put Example

Use a simple illustrative contract: the underlying is priced at 50, the put strike is 50, and the premium paid is 3. The breakeven at expiration is 47, calculated as 50 minus 3.

If the underlying finishes above 50, the put expires worthless and the buyer loses the 3 premium. If it finishes at 48, the put has 2 of intrinsic value, but that is still less than the 3 premium paid. If it finishes at 44, the put has 6 of intrinsic value, which is 3 above the premium cost before fees.

This example is only a simplified payoff illustration. Before expiration, the option value can also change because of time remaining, implied volatility, and liquidity, even if the underlying price has not reached the expiration breakeven.

A long put can be directionally right and still disappoint if the decline is too small, arrives too late, or is offset by a drop in implied volatility before the position is closed.

Why Time Decay and Implied Volatility Matter

A long put has time value before expiration. That time value can decline as expiration approaches, especially if the underlying price does not move far enough or quickly enough. This is the time decay problem for the buyer: being directionally right eventually may not be enough if the contract loses too much time value first.

Implied volatility can also change the option’s price before expiration. Higher implied volatility can make puts more expensive because the market is pricing a wider expected range. Lower implied volatility can reduce a put’s value even if the underlying price is still near the original level.

Important distinction: the expiration payoff formula is clean, but the live option price can be less clean. Premium, time remaining, implied volatility, and market liquidity all influence the value before expiration.

At the market-indicator level, put demand is often summarized differently through the put call ratio, but that indicator should not be confused with the payoff mechanics of one long put contract.

Expiration, Exercise, and Assignment Boundary

A long put can be closed, exercised, or allowed to expire depending on the contract, broker rules, account permissions, and the holder’s decision. If a put expires out of the money, it normally expires worthless. If it expires in the money, exercise or automatic exercise rules may create consequences tied to selling the underlying at the strike price.

This is why expiration handling matters. A payoff diagram shows the economic boundary, but it does not fully explain operational details such as exercise thresholds, assignment mechanics on the other side of the contract, or whether an account has the shares or permissions needed for the resulting position.

What a Payoff Chart Does Not Show

A long put payoff chart is useful because it shows the strike, breakeven, maximum loss, and downside payoff shape at expiration. It is incomplete because it does not show the path taken before expiration.

- Liquidity: a wide bid-ask spread can make the contract harder to trade near theoretical value.

- Time decay: the option can lose value as expiration approaches if the expected move does not develop.

- Implied volatility: changes in volatility expectations can raise or lower the option price before expiration.

- Expiration handling: in-the-money contracts can create exercise or position consequences depending on account rules.

- Fees and commissions: small examples can look cleaner than real account outcomes after costs.

Long Put vs Nearby Option Structures

A long put is often confused with other options structures because several of them involve downside exposure, premium, or put contracts. The difference is the role of the contract in the position.

| Concept | Main structure | Core distinction |

|---|---|---|

| Protective put | Owned shares plus a bought put | Uses a put to define downside risk around an existing stock position. |

| Long call | Bought call option | Uses premium to seek upside exposure instead of downside payoff exposure. |

| Short put | Sold put option | The seller receives premium but takes on obligation if assigned. |

| Cash-secured put | Short put backed by cash | Combines a put-selling obligation with reserved cash for potential share purchase. |

| Short stock | Borrowed shares sold short | Creates direct short exposure rather than a defined-premium option position. |

The cleanest way to separate them is to ask what is owned, what is sold, and where the obligation sits. A long put buyer owns a contractual right. A short put seller accepts a contractual obligation.

When a Long Put Is In the Money or Out of the Money

A put is in the money when the underlying price is below the strike price. It is out of the money when the underlying price is above the strike price. That label describes intrinsic value, not whether the full position is profitable after premium.

This distinction matters because a long put can be in the money and still lose money overall if the intrinsic value is smaller than the premium paid. The breakeven line, not only the strike line, determines whether the expiration payoff has overcome the original cost.

Common Misunderstanding

A long put does not automatically become profitable just because the underlying price falls. The decline must be large enough, and occur within the contract’s time window, to overcome the premium paid and any trading costs.

Another common misunderstanding is treating the maximum loss boundary as if the position has no risk. The loss may be defined, but losing the full premium is still a real outcome if the contract expires worthless.

Related Concepts

To understand the contract itself, start with the put option. To understand cost and breakeven, focus on option premium. To compare downside structures, use protective put, short put, and cash-secured put as separate contract roles rather than interchangeable labels.

FAQ

What is the maximum loss on a long put?

The maximum loss is normally the premium paid for the put, plus any fees or commissions, if the option expires worthless.

Can a long put profit be unlimited?

No. A long put payoff can increase as the underlying falls, but the underlying price cannot fall below zero, so the profit potential is bounded by that lower limit.