A long call option is not simply a cheaper version of owning the underlying stock. It is a contract position where the buyer pays a premium for the right, but not the obligation, to buy shares at a fixed strike price before expiration.

The contract can benefit from a rising underlying price, but the result depends on more than the stock moving higher. Premium paid, time remaining, implied volatility, strike price, and the expiration point all affect whether the position has value and whether that value is enough to offset the original cost.

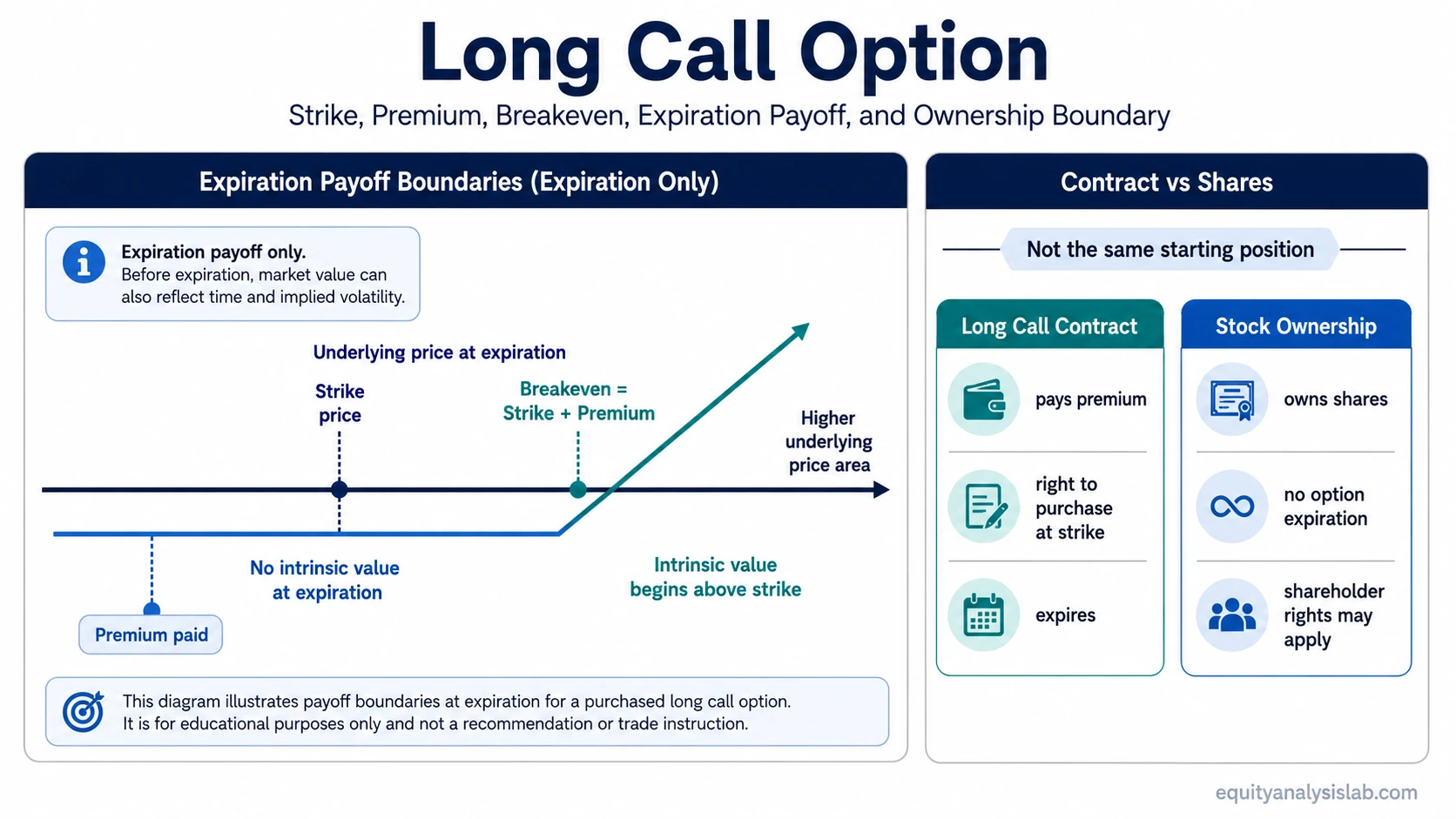

Definition: A long call option is a purchased call contract. The holder pays a premium for the right to buy the underlying shares at the strike price before the option expires. The buyer controls the right; the seller carries the corresponding obligation if exercise occurs.

Key Points

- A long call gives the buyer a right to buy shares at the strike price, not immediate stock ownership.

- The premium paid is the starting cost and is usually the maximum loss before transaction costs.

- The expiration breakeven is the strike price plus the premium paid.

- Time decay can reduce option value even when the underlying stock does not fall sharply.

- Implied volatility can raise or lower the option’s market value before expiration.

- Exercise can create share ownership, but the long call itself is still a contract until that procedural step occurs.

What Is a Long Call Option?

A long call option is created when an investor buys a call contract. The contract specifies the underlying asset, strike price, expiration date, premium, and contract size. In listed equity options, one standard contract usually represents 100 shares, although contract terms can differ after corporate actions or special adjustments.

The buyer has directional upside exposure because the call becomes more valuable when the underlying price rises above the strike by enough to matter. That exposure is different from owning the shares because the option has an expiration date and can lose value as time passes.

The clean contract distinction is simple: the buyer pays premium today, receives the right to buy at the strike price, and must account for expiration. No dividend rights, voting rights, or shareholder ownership exist from the long call alone.

Why a Long Call Is Not the Same as Owning Stock

Common misunderstanding: A long call can look like a low-cost substitute for stock because the premium is smaller than buying the shares outright. That shortcut misses the contract structure. The option can expire worthless, lose value from time decay, or change in price because implied volatility falls.

Owning stock gives direct participation in the share price, with no option expiration date. A long call gives conditional exposure through a contract. The stock price can rise, yet the option may still fail to recover its premium if the move is too small, too late, or accompanied by a drop in implied volatility.

Stock ownership also starts immediately when shares are purchased. A call buyer does not own shares unless the call is exercised or otherwise converted through the applicable broker and clearing process. That distinction matters for dividends, voting, capital use, and expiration planning.

Long Call Payoff, Breakeven, and Maximum Loss

At expiration, the intrinsic value of a long call depends on the underlying price relative to the strike price. If the underlying price is below the strike, the call is out of the money and usually expires worthless. If the underlying price is above the strike, the call has intrinsic value equal to the amount above the strike.

Expiration breakeven: strike price + premium paid.

The maximum loss is usually the premium paid, plus any transaction costs. This defined loss limit does not make the position safe; it only defines the most direct contract loss if the option expires worthless.

| Underlying price at expiration | Contract result | Interpretation before transaction costs |

|---|---|---|

| Below the strike price | The call expires out of the money | The premium is lost |

| At the strike price | The call has no intrinsic value | The premium is still not recovered |

| Above the strike but below breakeven | The call has intrinsic value | The value is not enough to recover the premium |

| Above breakeven | The call value exceeds strike plus premium | The expiration payoff is above breakeven |

Simple Long Call Option Example

A call option with a 50 strike and a 4 premium has an expiration breakeven of 54.

This example describes expiration payoff only; before expiration, the option’s market price can still change because time value, implied volatility, liquidity, and moneyness are changing.

If the underlying price finishes below 50, the option has no intrinsic value and the premium is lost. If the underlying finishes at 52, the option has 2 of intrinsic value, but that is still less than the 4 premium paid. If the underlying finishes above 54, the expiration payoff is above breakeven before transaction costs.

| Input or outcome | Value | Meaning |

|---|---|---|

| Strike price | 50 | The fixed purchase price if the call is exercised |

| Premium paid | 4 | The contract cost and usual maximum loss before transaction costs |

| Breakeven at expiration | 54 | Strike price plus premium paid |

| Underlying at 52 | 2 intrinsic value | Value exists, but the premium is not fully recovered |

| Underlying at 56 | 6 intrinsic value | Expiration value is above the 54 breakeven before costs |

What Changes a Long Call Before Expiration

Before expiration, a long call is not valued only by current intrinsic value. Its market price can also reflect time remaining, implied volatility, moneyness, liquidity, and how quickly the underlying price move develops.

| Variable | How it affects a long call | Point to remember |

|---|---|---|

| Underlying price | A higher underlying price generally helps a call, especially as it moves above the strike. | The move must still be large enough to offset the premium by expiration. |

| Time remaining | More time can support option value because the contract still has room for movement. | Time value usually decays as expiration approaches. |

| Implied volatility | Higher implied volatility can increase the option’s market value before expiration. | A volatility decline can hurt the option even if the stock price is stable or slightly higher. |

| Moneyness | In-the-money, at-the-money, and out-of-the-money calls behave differently. | Out-of-the-money calls require a larger price move to have intrinsic value. |

| Liquidity and spread | Bid-ask spreads can affect the price available to enter or exit the contract. | Displayed theoretical value may differ from executable market value. |

Long Call Risks and Common Misunderstandings

Limitation: Defined risk means the premium loss can be bounded, not that the position is low risk. A long call can lose the entire premium if the underlying price does not move far enough before expiration.

The most common risk is paying for a price move that does not arrive in time. The underlying stock may stay flat, rise too slowly, or rise after the option has already lost much of its time value.

Implied volatility creates another constraint. If the option was purchased when implied volatility was elevated, a later volatility decline can reduce the option’s price even when the underlying asset does not move sharply against the position.

Exercise also needs careful interpretation. A long call gives the right to buy shares, but many option positions are closed or expire without exercise. Automatic exercise rules, broker procedures, transaction costs, and available capital can affect the final outcome, so the contract right should not be confused with automatic stock ownership in every case.

Long Call vs Related Option Structures

A long call is the purchased-call structure. A covered call starts from owned shares and adds a short call obligation, so the starting position and assignment result are different.

A long put option uses a purchased put to create downside-oriented option exposure. It is the directional opposite in contract payoff, but it still shares the same need to understand premium, expiration, time value, and implied volatility.

Stock-like option exposure can also be built through a synthetic long stock structure, which combines option legs rather than using a single purchased call. That structure belongs in a separate comparison because its obligations and risk profile are not the same as a simple long call.

| Structure | Starting position | Main distinction from a long call |

|---|---|---|

| Long call | Buy one call option | Purchased right to buy at the strike before expiration |

| Covered call | Own shares and sell a call | Starts with stock ownership and creates a short-call obligation |

| Long put | Buy one put option | Purchased right to sell at the strike before expiration |

| Synthetic long stock | Combine option legs | Creates stock-like exposure through more than one option position |

What a Long Call Does and Does Not Change

A long call separates exposure from ownership. The contract can create upside participation with a defined premium outlay, but it also adds expiration, time decay, volatility sensitivity, and procedural exercise limits that do not exist in plain stock ownership.

The important distinction is not that a call is better or worse than stock. The exposure is contract-bound. The payoff depends on whether price movement, time remaining, volatility, and the strike relationship are enough to overcome the premium paid.

FAQ

What is a long call option?

A long call option is a purchased call contract that gives the buyer the right, but not the obligation, to buy shares at the strike price before expiration.

What is the maximum loss on a long call?

The maximum loss is usually the premium paid for the call, plus any transaction costs, if the option expires worthless.

How do you calculate the breakeven on a long call?

The expiration breakeven equals the strike price plus the premium paid. A call with a 50 strike and a 4 premium has a 54 breakeven before transaction costs.

Does a long call mean the buyer owns the stock?

No. A long call gives a contract right to buy shares. Stock ownership begins only if shares are acquired through exercise or another transaction.