What Is Synthetic Long Stock?

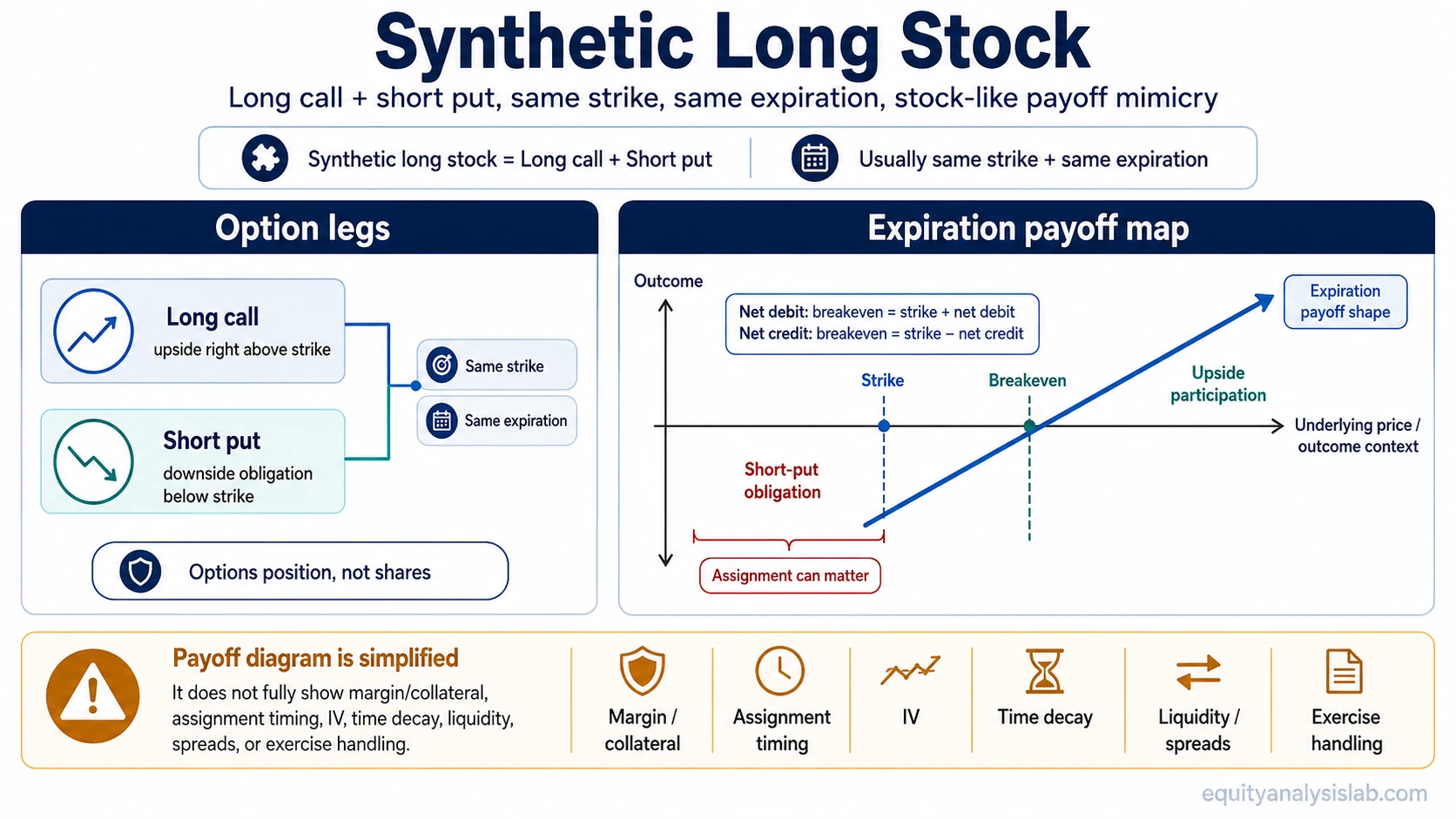

A synthetic long stock position uses a long call and a short put, usually with the same strike and expiration, to create stock-like exposure through options.

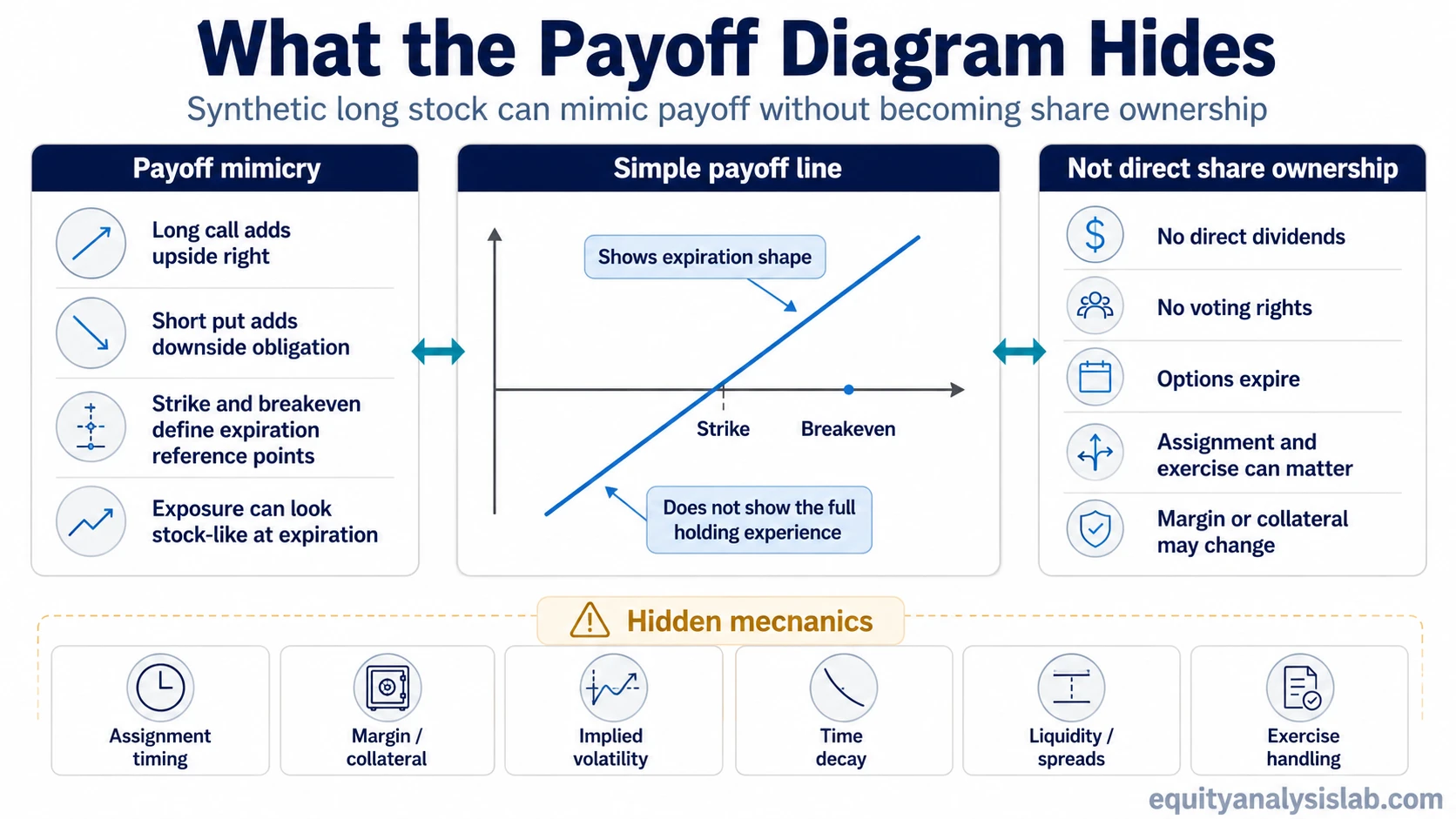

At expiration, the structure can resemble owning shares: it participates in upside above the strike and loses value when the underlying falls below the strike. But payoff mimicry is not the same as share ownership. A synthetic long stock position has expiration, short put assignment risk, margin or collateral requirements, option liquidity, and no direct shareholder voting rights or dividend ownership.

Definition: Synthetic long stock is an options structure made from buying a call and selling a put on the same underlying, usually at the same strike price and expiration date. The combined position is designed to behave like long stock exposure, while still remaining an options position.

Key Points About Synthetic Long Stock

- A synthetic long stock position combines a long call with a short put.

- The call creates upside participation above the strike.

- The short put creates downside exposure and potential assignment below the strike.

- The breakeven depends on whether the combined options position is opened for a net debit or net credit.

- The position does not provide direct dividends, voting rights, or permanent ownership of shares.

- Lower initial cash outlay does not automatically mean lower risk because the short put leg can require margin or collateral.

How Synthetic Long Stock Works

The structure starts with two option legs on the same underlying. The investor buys a call option and sells a put option, usually using the same strike price and the same expiration date. A long call gives upside exposure if the underlying rises above the strike, while the short put creates an obligation if the underlying falls below the strike.

The basic inputs are the underlying price, strike price, expiration date, call premium, put premium, net debit or net credit, and the implied volatility environment. These inputs determine the position’s breakeven and how closely the options package behaves like stock before expiration.

The important boundary is that synthetic long stock expresses a market view through options. It can create stock-like exposure, but it does not turn the holder into a shareholder unless exercise or assignment results in actual shares.

| Input | Why it matters |

|---|---|

| Underlying price | Shows where the market is trading relative to the strike. |

| Strike price | Sets the central payoff reference point for both the call and the put. |

| Expiration | Defines the life of the option structure; unlike stock, the position does not exist indefinitely. |

| Call premium | Cost paid for upside participation through the long call. |

| Put premium | Premium received for accepting the short put obligation. |

| Net debit or net credit | Changes the breakeven level above or below the strike. |

| Implied volatility and liquidity | Affect option pricing, spreads, and mark-to-market behavior before expiration. |

Synthetic Long Stock Payoff and Breakeven

At expiration, synthetic long stock is designed to move like long stock around the strike. If the underlying finishes above the strike, the long call has value and the short put usually expires out of the money. If the underlying finishes below the strike, the call may expire worthless and the short put can create a purchase obligation through assignment.

The position’s downside can be substantial because the investor is exposed to a stock-like decline below the strike. That downside is not unlimited in the literal sense, because an underlying stock cannot fall below zero, but the loss can still be large relative to the initial cash paid if the structure required little upfront debit.

In a stock-based underlying, the theoretical lower boundary is zero, so the risk should be described as substantial stock-like downside rather than literally unlimited downside.

| Opening cash flow | Breakeven formula | Meaning |

|---|---|---|

| Net debit | Strike price + net debit | The underlying must finish above the strike by enough to recover the net cost. |

| Net credit | Strike price − net credit | The premium received lowers the expiration breakeven below the strike. |

A payoff diagram can make this look simple, but the real position can change before expiration as implied volatility, time value, spreads, margin requirements, and assignment risk change.

Synthetic Long Stock vs Owning Stock vs Long Call

The main misunderstanding is treating synthetic long stock as identical to owning shares. The payoff can be similar at expiration, but the legal and practical position is different. Stock has no option expiration and includes shareholder rights. Synthetic long stock is a contract-based structure with exercise, assignment, and margin considerations.

| Feature | Synthetic long stock | Owning stock | Long call |

|---|---|---|---|

| Construction | Long call plus short put, usually same strike and expiration. | Direct ownership of shares. | One purchased call option. |

| Upside exposure | Stock-like upside above the strike at expiration. | Direct upside as the share price rises. | Upside through the right to buy above the strike. |

| Downside exposure | Stock-like downside below the strike through the short put obligation. | Share price can decline toward zero. | Loss is generally limited to the premium paid. |

| Initial capital / margin | May require less cash upfront, but the short put can require margin or collateral. | Requires paying for shares or using stock margin if applicable. | Requires paying the call premium. |

| Expiration | Yes. The options expire. | No fixed expiration for the shares themselves. | Yes. The call expires. |

| Assignment / exercise | Short put assignment and long call exercise can matter. | No option assignment or exercise process. | Exercise is possible, but there is no short put assignment. |

| Dividends / voting rights | No direct dividends or voting rights from the synthetic position. | Shareholder may receive dividends and voting rights, if applicable. | No direct dividends or voting rights from the call alone. |

| Main limitation | Stock-like exposure without stock ownership, plus expiration and assignment complexity. | Requires direct capital exposure to the shares. | Only captures the upside-right leg and can expire worthless. |

Synthetic Long Stock vs Long Call

A long call is only the upside-right leg of the structure. It gives the holder the right to buy the underlying at the strike price, but it does not create the same downside obligation as synthetic long stock.

Synthetic long stock adds the short put leg. That short put is what makes the payoff more stock-like below the strike, because the investor may be required to buy shares if assigned. This is why the structure can resemble long stock more closely than a call alone, but also why its downside and margin profile are very different from a simple long call.

What a Synthetic Long Stock Payoff Diagram Hides

A clean payoff line shows the expiration shape, not the full experience of holding the position. The diagram can show the slope above and below the strike, but it may not show the path risk created by assignment timing, margin changes, option pricing, or liquidity.

| Area | What the payoff diagram shows | What it may not show |

|---|---|---|

| Assignment timing | Exposure below the strike at expiration. | The short put may create assignment considerations before or at expiration. |

| Margin / capital requirement | The final payoff line. | Broker margin or collateral requirements can be material and may change. |

| Implied volatility | Expiration value at a final underlying price. | Option prices can move before expiration even if the underlying price does not move much. |

| Time decay | Final intrinsic-value relationship. | The long call and short put may not offset time-value changes perfectly before expiration. |

| Liquidity / spreads | Theoretical payoff. | Wide bid-ask spreads or thin contract liquidity can affect entry, adjustment, and exit value. |

| Dividends / shareholder rights | Stock-like price exposure. | The synthetic position does not directly receive dividends or voting rights. |

| Exercise / expiration handling | Where the payoff ends at expiration. | The investor still has to manage exercise, assignment, and contract settlement mechanics. |

Risks and Limitations of Synthetic Long Stock

The main risk is that the structure can look capital-efficient while still carrying stock-like downside. A small net debit or a net credit does not remove the obligation created by the short put. If the underlying falls sharply, the position can lose value in a way that resembles owning shares from around the strike level.

Capital efficiency is not the same as low risk. Synthetic long stock may reduce the initial cash paid compared with buying shares, but the short put leg can still require margin, collateral, and the ability to handle assignment. A cash-secured put is a related structure where the collateral side of the put obligation is more explicit.

| Risk or limitation | How it affects the position |

|---|---|

| Short put assignment | The investor may be obligated to buy shares if the put is assigned. |

| Margin / capital changes | Lower upfront cost can coexist with significant margin or collateral requirements. |

| Expiration handling | The position must be resolved, exercised, assigned, closed, or allowed to expire according to contract terms and account rules. |

| Implied volatility and time decay | Before expiration, option value may change for reasons beyond the underlying price move. |

| Liquidity and spreads | Contract liquidity and bid-ask spreads can affect the practical price of entering or exiting the legs. |

| No dividends or voting rights | The options position does not directly provide shareholder benefits. |

| Execution and exercise complexity | Two option legs create more moving parts than simply owning shares. |

Simple Synthetic Long Stock Example

Consider a generic underlying trading near 100. An investor creates synthetic long stock by buying a 100-strike call for 6 and selling a 100-strike put for 5, using the same expiration. The position is opened for a net debit of 1.

The expiration breakeven is the strike plus the net debit: 100 + 1 = 101. Above 101, the position begins to show a net gain at expiration. Below 101, the position loses value, and below the strike the short put becomes the main downside leg.

If the underlying finishes at 120, the call is in the money and the put is out of the money, creating stock-like upside exposure after accounting for the net debit. If the underlying finishes at 80, the call may expire worthless and the short put creates a loss that resembles owning stock from the strike area, subject to the opening debit and assignment handling.

Example summary: Strike 100, call premium paid 6, put premium received 5, net debit 1, breakeven 101. The example is illustrative only and does not represent a real ticker, recommendation, or trade result.

When Synthetic Long Stock Is Misread

A common mistake is focusing only on the stock-like payoff line and ignoring what creates it. The long call supplies the upside right, but the short put supplies the downside obligation. The combined exposure can look simple on a payoff chart while still carrying assignment, expiration, margin, and liquidity considerations.

Another mistake is assuming the structure is automatically better than buying shares because it may require less initial cash. The better framing is narrower: synthetic long stock is an options-based expression of stock-like exposure. Its practical use depends on margin rules, contract terms, risk capacity, and the ability to handle assignment.

Related Concepts

For the upside-right leg, the long call section above explains why the call creates upside participation without direct share ownership. For the obligation and collateral side of the short put exposure, compare the structure with a cash-secured put. For the opposite directional option right, a long put explains how a put buyer gains downside participation instead of stock-like upside exposure.

Protective puts and covered calls are separate stock-and-option structures. They can help clarify the difference between owning shares with an option overlay and creating stock-like exposure synthetically through options.

FAQ

Is synthetic long stock the same as owning shares?

No. Synthetic long stock can mimic long stock payoff at expiration, but it is not direct share ownership. It has option expiration, assignment and exercise mechanics, margin or collateral considerations, and no direct shareholder voting rights or dividends from the synthetic position itself.

Can synthetic long stock be assigned?

Yes. The short put leg can create assignment risk if the put is assigned. Assignment handling depends on the contract, account, broker rules, and timing, so the payoff diagram alone does not show the full operational reality.

Does synthetic long stock receive dividends?

No. The synthetic options position does not directly receive dividends because it is not direct stock ownership. Dividends may still affect option pricing and exercise considerations, but the position itself is not the same as holding shares.