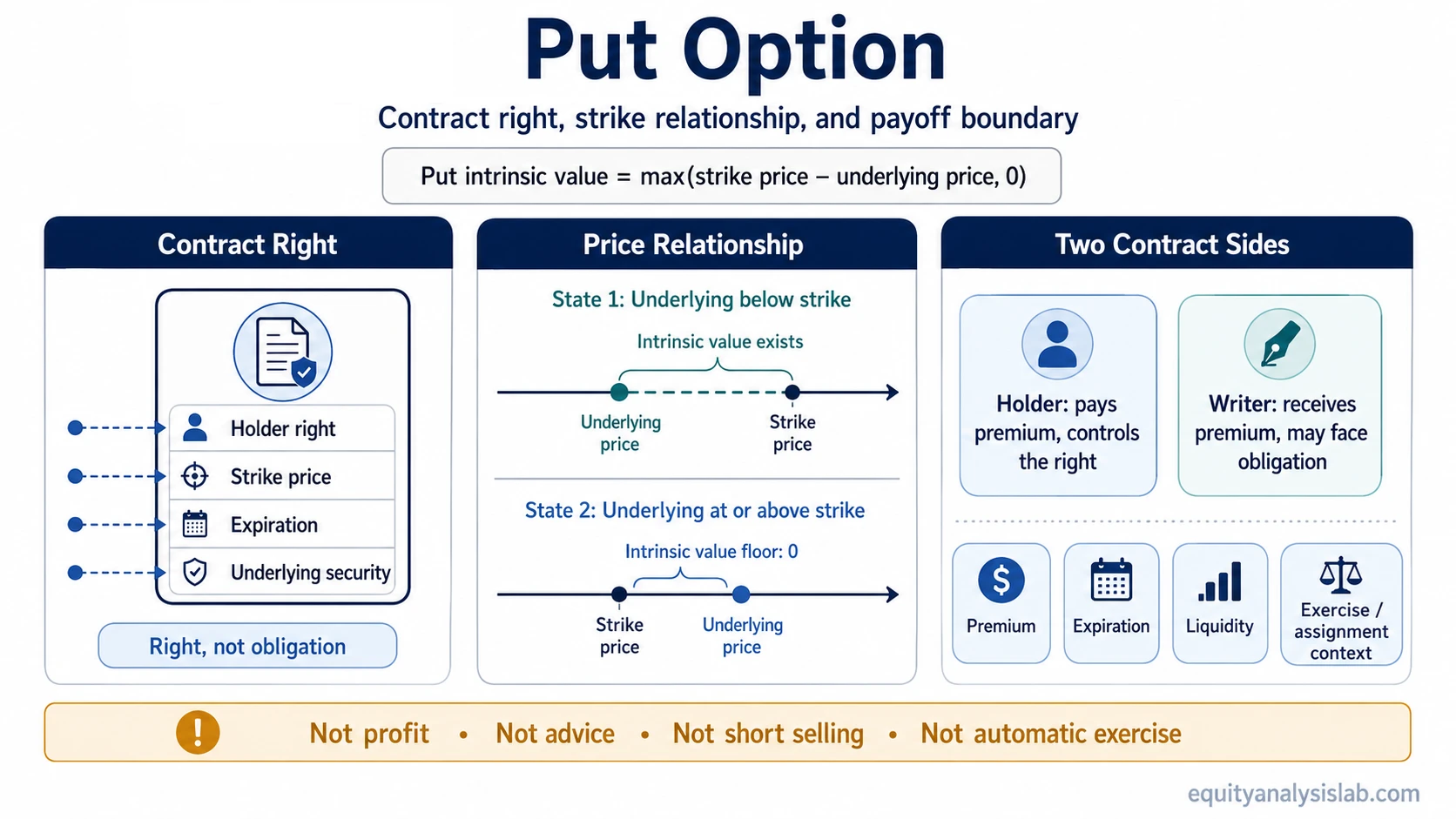

A put option is an options contract that gives the holder the right, not the obligation, to sell an underlying security at a specified strike price by or before expiration, depending on the contract style.

A put option is best understood as a contract payoff and risk structure, not as a recommendation to bet against a stock. The buyer has a right. The seller, also called the writer, may have an obligation if the contract is exercised or assigned. Premium, strike price, expiration, underlying price, and liquidity all affect how the contract should be interpreted.

Key Points About a Put Option

- A put option gives the holder the right to sell the underlying security at the strike price.

- The buyer pays a premium for that right; the seller receives the premium and may face an obligation.

- Put intrinsic value is positive only when the strike price is above the underlying price.

- A put option is not the same as short selling, guaranteed profit, or an automatic exercise decision.

- Time decay, implied volatility, bid-ask spread, and expiration can change the value of the contract before expiration.

Put Option Definition

A put option is a contract that gives its holder the right to sell an underlying asset or security at a specified strike price within a defined time window. The holder is not required to use that right. The seller of the put may be required to buy the underlying security at the strike price if exercise or assignment occurs.

The basic definition is simple, but the contract is incomplete without its terms. A put option always needs an underlying security, strike price, expiration date, premium, and contract rules. Without those details, the word “put” does not describe the actual risk or payoff.

How a Put Option Works

A put option links the contract value to the relationship between the underlying price and the strike price. If the underlying price is below the strike price, the right to sell at the higher strike can have intrinsic value. If the underlying price is at or above the strike price, intrinsic value is zero, although the option may still have extrinsic value before expiration.

The core intrinsic value formula is:

Put intrinsic value = max(strike price − underlying price, 0)

Intrinsic value is not the same as total profit or total option premium. The premium paid, remaining time, implied volatility, bid-ask spread, and closing or exercise method can all change the final result.

Put Option Contract Terms

The contract terms determine what the put option actually represents. A put with a nearby expiration, wide spread, and high premium can behave very differently from a put with the same strike but more time, better liquidity, and different volatility conditions.

| Contract term | What it means | Why it matters |

|---|---|---|

| Underlying security | The asset connected to the option contract | Determines which price the contract references |

| Strike price | The price at which the holder has the right to sell | Sets the boundary for intrinsic value |

| Expiration | The date or time window when the contract ends | Limits how long the right can exist |

| Premium | The price paid by the buyer and received by the seller | Affects breakeven and maximum buyer loss |

| Contract size | The amount of underlying exposure represented by one contract | Changes the dollar impact of price movement |

| Option style | The rules governing when exercise may occur | Changes exercise and assignment mechanics |

| Liquidity | The ease of entering or exiting near quoted prices | Wide spreads can reduce execution reliability |

Put Option Buyer vs Seller

The buyer and seller have different positions in the same contract. The buyer controls a right. The seller accepts a possible obligation. That distinction is central because the same put option can mean limited premium risk for one side and materially larger assignment-driven exposure for the other.

| Side | Contract role | Main risk boundary |

|---|---|---|

| Put buyer / holder | Has the right, not the obligation, to sell at the strike price | The premium paid can be lost if the contract loses value or expires worthless |

| Put seller / writer | May be obligated to buy the underlying at the strike price if assigned | Risk can be much larger than the premium received because assignment exposure depends on the underlying price |

Simple Put Option Example

Suppose a put option has a strike price of 50 and the underlying security is at 45. Before considering premium, time value, liquidity, and transaction costs, the put has 5 of intrinsic value because the holder has the right to sell at 50 while the underlying is priced at 45.

If the underlying security is at 50 or above, the put has zero intrinsic value. It may still have extrinsic value before expiration, but that value depends on time remaining, implied volatility, contract demand, and the quoted market for that specific option.

Put Option Payoff and Intrinsic Value

A put option generally becomes more valuable when the underlying price falls below the strike price, but that statement only describes part of the contract. The total outcome depends on the premium paid or received, the timing of the move, the option’s remaining extrinsic value, and the price available when closing or exercising.

A put is commonly described as in the money when it has positive intrinsic value. That means the strike price is above the underlying price. For a deeper definition of this boundary, see in-the-money put option.

Put Option Premium and Risk

The premium is the price of the put option contract. For the buyer, the premium is the amount paid to obtain the right to sell at the strike price. If the contract expires worthless or is closed for less than the premium paid, the buyer can lose some or all of that premium.

For the seller, the premium received is not the whole risk story. The seller may be assigned and required to buy the underlying at the strike price. That obligation can create exposure far larger than the premium received, especially when the underlying price is much lower than the strike price.

Put Option vs Call Option

A put option gives the holder the right to sell. A call option gives the holder the right to buy. Both are options contracts, but they respond differently to the relationship between the underlying price and the strike price.

| Contract type | Holder’s right | Basic intrinsic value condition |

|---|---|---|

| Put option | Right to sell at the strike price | Positive when strike price is above underlying price |

| Call option | Right to buy at the strike price | Positive when underlying price is above strike price |

Exercise, Assignment, and Closing a Put Option

Exercise means using the contractual right to sell the underlying at the strike price. Assignment is the process that can place the seller under the corresponding obligation. Closing a put option is different: it means exiting the option position through an offsetting transaction rather than using the contract to sell the underlying.

Exercise and assignment are mechanics, not automatic judgments about whether the contract was useful or profitable. A put option may be sold, closed, exercised, assigned, or expire depending on contract terms and account-level decisions. For a focused explanation of the mechanics, see option exercise.

Common Put Option Misunderstandings

A put option is often described too loosely as a bearish bet. That framing can hide the actual contract mechanics. The safer interpretation is to separate the right, the obligation, the premium, the expiration date, and the possible exercise or closing path.

| Misunderstanding | Cleaner interpretation |

|---|---|

| A put option is the same as short selling | A put is an options contract with premium, expiration, strike, and assignment mechanics. Short selling is a separate position type. |

| A put option automatically creates profit if the underlying falls | The underlying move must be considered alongside premium, timing, volatility, spreads, and closing or exercise value. |

| A put option has value whenever the market feels risky | Contract value depends on the specific strike, expiration, premium, underlying price, volatility, and liquidity. |

| Buying a put means the contract must be exercised | Exercise is only one possible path. Many option positions are closed before expiration instead. |

Limitations That Change Put Option Interpretation

Time decay: A put option can lose extrinsic value as expiration approaches, even if the underlying price does not move much.

Implied volatility: Changes in expected volatility can raise or lower option premium before expiration.

Bid-ask spread: A wide spread can make the quoted value less reliable than it appears on the surface.

Expiration: A correct directional idea can still fail to translate into contract value if timing and premium work against the position.

Assignment and exercise: Contract rights and obligations can change into underlying exposure if exercise or assignment occurs.

Related Options Concepts

A put option is easier to interpret after the basic options framework is clear. The broader contract structure is covered in how options work. The closest related concepts are call options, option exercise, and in-the-money status because they define the opposite contract right, the contract-use mechanics, and the intrinsic-value boundary.

FAQ

Is a put option the same as short selling?

No. A put option is a contract that gives the holder the right to sell at a strike price. Short selling is a separate position type that involves selling borrowed shares or another borrowed asset. A put has premium, expiration, strike, and contract-specific exercise or assignment mechanics.

Can a put option buyer lose more than the premium?

The buyer of a standard put option can lose the premium paid for the option, plus any transaction costs. The seller’s risk is different because assignment can create an obligation connected to the underlying security.

Does a put option have to be exercised?

No. Exercise is one possible path, but a put option may also be closed before expiration or allowed to expire. The correct mechanical outcome depends on the contract, account rules, and the holder’s decision.

When does a put option have intrinsic value?

A put option has intrinsic value when the strike price is above the underlying price. The basic formula is max(strike price − underlying price, 0). Intrinsic value is only one part of total option value before expiration.