A short put option is a sold put contract where the seller receives premium and accepts the obligation to buy shares at the strike price if assignment occurs. The premium is the maximum simplified gain, but it does not remove the downside exposure that can appear if the underlying price falls.

The position is best understood as contract exposure, not stock ownership at the start. The seller does not own downside protection. Instead, the seller has taken the other side of a put buyer’s right to sell shares at the strike price before or at expiration, depending on the option style and assignment rules.

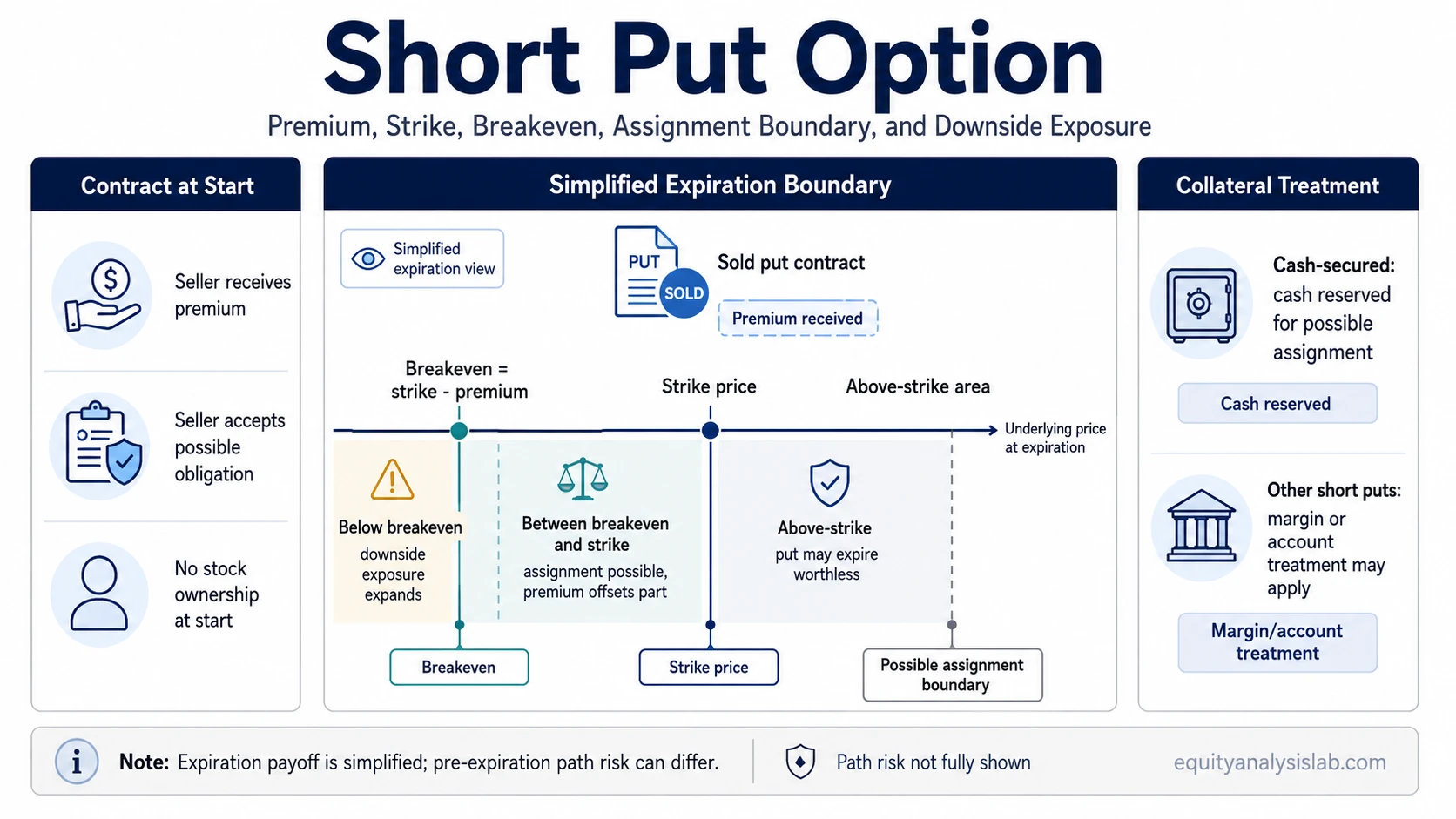

Key Points About a Short Put Option

- A short put is a sold or written put option.

- The seller receives premium upfront, and that premium is the maximum simplified gain before contract multiplier, costs, taxes, and account treatment.

- Assignment can create an obligation to buy shares at the strike price.

- The simplified breakeven is the strike price minus the premium received.

- Downside exposure can be significant if the underlying price falls far below the strike.

- A cash-secured version is collateralized with reserved cash, but not every short put is structured that way.

- Payoff diagrams usually simplify expiration outcomes and do not show every path risk before expiration.

How a Short Put Option Works

A put option gives its buyer the right to sell shares at a specified strike price. When that put is sold short, the seller receives premium and accepts the opposite exposure: the possible obligation to buy shares at the strike if the option is exercised or assigned.

The important variables are the underlying price, strike price, expiration date, premium received, implied volatility, and assignment condition. Together, these determine whether the short put remains out of the money, moves near the strike, or creates a stock-purchase obligation.

A short put is often discussed as a strategy, but the safer first reading is structural. It is a contract with defined terms and an asymmetric exposure profile: premium received is limited, while downside exposure expands as the underlying price declines.

Short Put Payoff, Breakeven, and Risk

The simplified expiration payoff starts with the premium received. If the underlying price finishes above the strike at expiration and no assignment occurs, the put expires worthless and the seller keeps the premium. That is the maximum simplified gain before contract multiplier, transaction costs, taxes, and account-specific effects.

The simplified breakeven is:

Short put breakeven = strike price – premium received

If the underlying price is below the breakeven at expiration, the short put has a simplified loss. The lower the underlying price falls, the larger the loss becomes. The premium reduces the breakeven but does not create a full protection boundary.

| Underlying price at expiration | Simplified short put outcome | Interpretation |

|---|---|---|

| Above the strike | Put likely expires worthless | Premium is retained as the simplified maximum gain. |

| Between strike and breakeven | Assignment may occur, but premium offsets part of the strike exposure | The result may still be positive or near breakeven in simplified expiration terms. |

| Below breakeven | Loss increases as the underlying price falls | The premium is no longer enough to offset the decline below the strike. |

Short Put Assignment and Collateral Requirements

Assignment is the event that turns the short put obligation into a stock-purchase obligation. If assigned, the seller may be required to buy shares at the strike price, even if the market price is lower at that time.

Collateral and margin treatment change how the exposure is supported inside an account. A cash-secured put reserves enough cash to support the possible stock purchase if assigned.

A margin-based, naked, or uncovered short put may not reserve the full purchase amount in cash. That can increase account-level risk because margin requirements, buying power, and liquidation pressure can change before expiration.

Collateral is therefore not just an administrative detail. It changes how the same short put payoff profile interacts with account liquidity and assignment risk.

Short Put vs Cash-Secured Put and Long Put

A short put is the broader sold-put exposure. A cash-secured put is one collateralized version of that exposure where cash is reserved for possible assignment.

A long put option has the opposite contract role. The long put buyer pays premium for downside rights, while the short put seller receives premium and takes on the possible obligation to buy shares.

That distinction also separates short puts from put protection on owned shares. A protective put usually starts with stock ownership and adds a long put to define part of the downside. A short put starts with a sold option contract and can create ownership only if assignment occurs.

| Concept | Starting position | Main contract role | Key boundary |

|---|---|---|---|

| Short put | Sold put contract | Receives premium and accepts possible buy obligation | Breakeven is strike minus premium. |

| Cash-secured put | Sold put with reserved cash | Same sold-put exposure, collateralized for possible assignment | Cash support changes account risk but not the basic payoff formula. |

| Long put | Purchased put contract | Pays premium for downside rights | Risk is generally limited to premium paid, before costs and exercise considerations. |

| Protective put | Owned shares plus purchased put | Uses a put as downside protection | The put is attached to existing stock exposure. |

What a Short Put Does Not Show on a Payoff Chart

A short put payoff chart usually shows a clean expiration line: limited upside from premium and increasing downside below breakeven. That is useful, but it is not a complete model of the position before expiration.

Before expiration, option value can move against the seller because of the underlying price, remaining time, implied volatility, and assignment risk. A short put can show an unrealized loss even if the underlying price has not reached the final expiration breakeven.

Payoff Chart Limitation

Expiration payoff diagrams usually omit path risk, early assignment risk, liquidity, transaction costs, tax treatment, and changes in margin or collateral requirements. They clarify the boundary, but they do not describe every account-level risk while the contract is open.

Simple Short Put Payoff Example

Consider a generic short put with a $50 strike and $2 premium received. The simplified breakeven is $48. If the underlying price is above $50 at expiration and the option expires worthless, the simplified maximum gain is $2 per share before contract multiplier, costs, and account-specific effects.

If the underlying price is $45 at expiration, the simplified intrinsic loss is $5 per share against the strike. After the $2 premium received, the simplified net loss is $3 per share before costs and other adjustments. The example shows why premium lowers the breakeven but does not cap downside exposure.

| Input or outcome | Value | Meaning |

|---|---|---|

| Strike price | $50 | Price at which assignment may require share purchase. |

| Premium received | $2 | Maximum simplified gain before multiplier, costs, and account effects. |

| Breakeven | $48 | Strike minus premium. |

| Underlying at $45 | $3 simplified net loss per share | Loss below breakeven after premium offset. |

Common Misunderstandings About Short Puts

Premium is not full protection: The premium reduces the breakeven, but it does not protect the seller from a large decline in the underlying price. Treating premium as a safety cushion rather than a limited offset understates the exposure.

Cash-secured and naked are not the same account setup: Both can involve a sold put, but the account support differs. A cash-secured structure reserves cash for assignment, while uncovered or margin-based versions depend on account rules and available buying power.

Assignment is not only a technical detail: Assignment can convert option exposure into share ownership at the strike. That changes the position from an option contract into stock exposure, with a cost basis shaped by the strike and premium.

FAQ

What is a short put option?

A short put option is a sold put contract. The seller receives premium and accepts the obligation to buy shares at the strike price if assignment occurs.

What is the maximum gain on a short put?

The simplified maximum gain is the premium received, before contract multiplier, transaction costs, taxes, and account-specific effects.

What is the breakeven on a short put?

The simplified breakeven is the strike price minus the premium received.

Can a short put lose more than the premium received?

Yes. The premium is the maximum simplified gain, but downside losses can increase if the underlying price falls below the breakeven.

Is a short put the same as a cash-secured put?

No. A cash-secured put is a collateralized version of a short put where cash is reserved for possible assignment. Other short puts may rely on margin or other account treatment.