Options basics are the core contract terms and risk boundaries that explain how calls, puts, strikes, premiums, expiration, exercise, assignment, and option-chain quotes fit together.

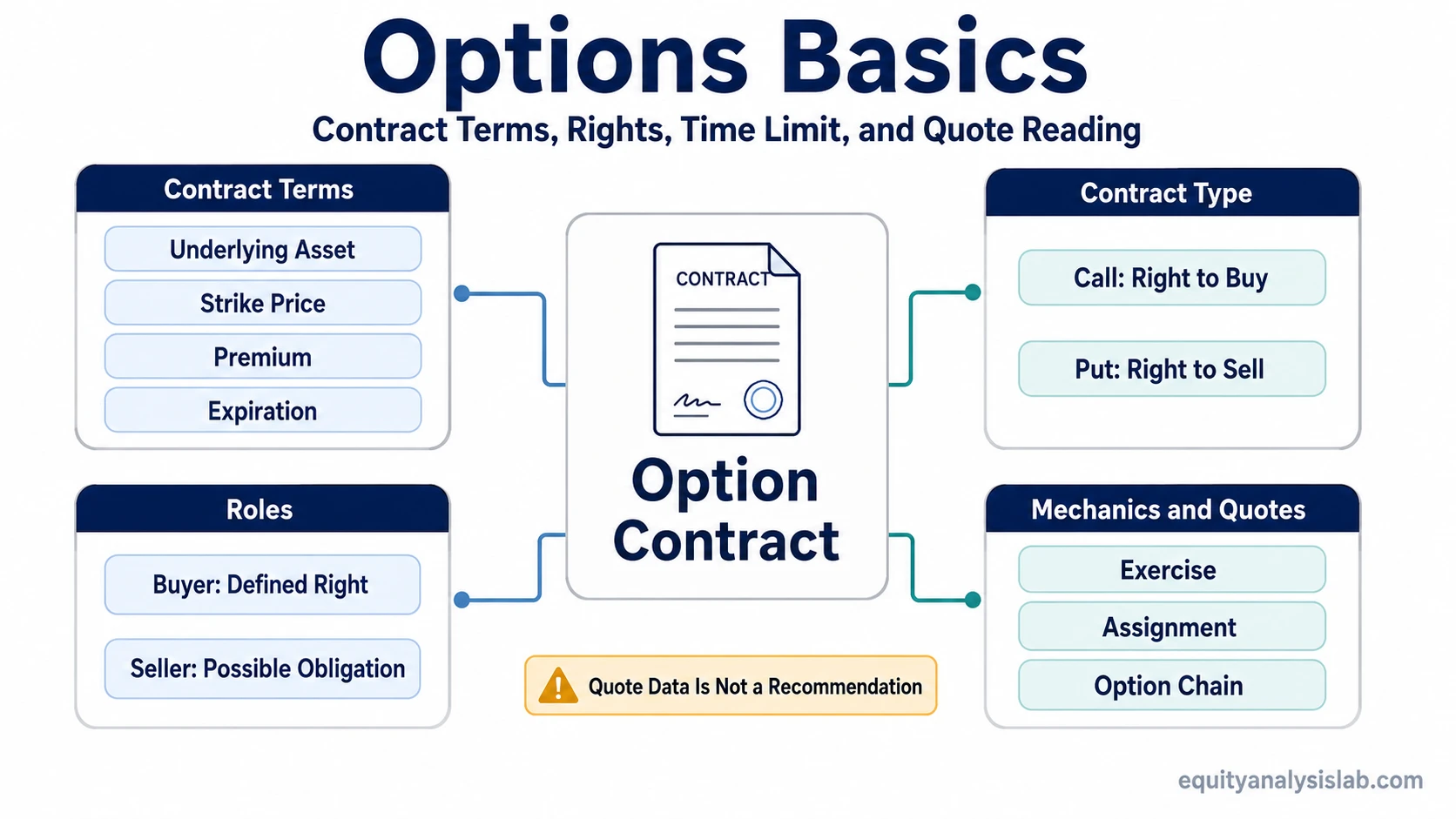

Definition: An option is a contract tied to an underlying asset. It gives the buyer a defined right and creates a different obligation profile for the seller, with the strike price, premium, and expiration date setting the basic contract frame.

For an investor, the useful starting point is not strategy selection. It is contract literacy: what the contract controls, what the buyer can choose, what the seller may be required to do, and which terms change the risk reading before any deeper analysis begins.

Key Points

- Options are contracts, not direct ownership of the underlying asset.

- Calls and puts differ because the right being controlled is different.

- Strike price, premium, and expiration define the basic contract terms.

- Exercise and assignment connect the contract to possible underlying-asset delivery or settlement mechanics.

- Option chains, liquidity, volatility, and Greeks help interpret quotes, but they do not turn a contract row into a recommendation.

What Options Basics Means

Options basics means understanding the contract before interpreting any strategy, quote, or payoff diagram. The contract has an underlying asset, a strike price, an expiration date, a premium, and a call or put type. Those terms explain what the contract references, what right exists, when the right ends, and what price is paid or received for the contract.

The beginner mistake is to treat the option as if it were only a cheaper version of the stock or ETF. An option can reference the same underlying asset, but the contract behaves differently because time, volatility, liquidity, and the buyer-seller obligation split matter.

Investor-use boundary: Options basics can help decode contract language and risk exposure. They do not answer whether an option should be used, which strategy fits, or whether a quote is attractive.

The Core Parts of an Option Contract

An option contract starts with the underlying asset. That underlying asset may be a stock, ETF, index, or another eligible instrument. Standard listed equity options often represent 100 shares, but contract size can vary after adjustments or in nonstandard contracts, so the actual contract specifications should be checked rather than assumed.

| Contract part | What it tells you | Beginner reading |

|---|---|---|

| Underlying asset | The asset the option references | The option is linked to that asset, but it is not the same as owning it directly |

| Strike price | The contract price used to test the option’s rights | The strike helps determine whether the contract has intrinsic value |

| Premium | The price paid by the buyer and received by the seller | The premium is part of risk, but it is not the whole risk story for every participant |

| Expiration | The date after which the contract right no longer exists | Time is part of the contract, not a background detail |

| Call or put type | The direction of the right created by the contract | A call and a put answer different contract questions |

The time limit on the contract matters because an option can lose relevance even if the underlying asset remains active. The expiration date controls when the right ends and when unresolved contract mechanics must be interpreted.

Calls, Puts, Rights, and Obligations

A call option gives the buyer the right to buy the underlying asset at the strike price, subject to the contract terms. A put gives the buyer the right to sell the underlying asset at the strike price, within the same contract framework.

The seller has the opposite side of that right. If the buyer has a right, the seller may have an obligation if the contract is exercised or otherwise assigned under the applicable contract rules. That asymmetry is one reason options cannot be understood only by looking at the premium.

Call buyer: controls a right related to buying the underlying at the strike price.

Put buyer: controls a right related to selling the underlying at the strike price.

Option seller: receives premium but may face obligations that depend on the contract type and assignment mechanics.

Assignment is the process that requires the seller side to fulfill the contract obligation when exercise or contract rules trigger that obligation. That is different from simply seeing a quote move up or down in an option chain.

Premium, Expiration, Exercise, and Assignment

The premium is the visible price of the option contract. For the buyer, the premium paid is a central part of the risk boundary. For the seller, the premium received does not automatically describe the full exposure, because seller obligations can extend beyond the premium depending on the position and contract type.

Expiration changes how the contract is read because time is finite. A contract can have a right that is economically meaningful at one point and less meaningful later if the underlying price, time remaining, implied volatility, and liquidity conditions change.

To exercise an option means to use the contract right under its terms. Assignment is the corresponding obligation process for the seller side. These concepts are related, but they are not the same action from the same participant’s perspective.

Risk boundary: Premium helps explain contract cost, but options risk also depends on position side, contract type, expiration, exercise and assignment mechanics, liquidity, volatility, and how the position is structured. Treating premium as the entire risk in every case is an unsafe shortcut.

Where Option Chains, Liquidity, and Volatility Fit

An option chain is the quote surface where contracts are usually grouped by expiration, strike, call side, put side, bid, ask, volume, open interest, and sometimes Greeks or implied volatility. The chain helps organize the contract information, but it does not decide whether a contract is suitable or attractive.

Liquidity affects how readable and usable a quote may be. A contract with a wide bid-ask spread, low volume, or limited open interest can be harder to interpret because the displayed quote may include more friction than a beginner expects.

Volatility and Greeks belong to the sensitivity layer. They help explain why an option price can change even when the underlying price has not moved in a simple one-for-one way. The basic point is that price sensitivity exists; detailed Greek-by-Greek interpretation belongs in more advanced options pricing concepts.

| Quote or sensitivity item | Basic role | What not to assume |

|---|---|---|

| Bid and ask | Show quoted buying and selling interest | A tight quote does not guarantee a good decision |

| Volume | Shows recent contract activity | High activity is not the same as a recommendation |

| Open interest | Shows contracts still open | Open interest does not explain why participants hold them |

| Implied volatility | Reflects market pricing of expected movement | High or low implied volatility needs context |

| Greeks | Estimate sensitivity to price, time, volatility, and rates | They are measurement tools, not standalone instructions |

Common Beginner Mistakes With Options Basics

Mistake 1: Confusing the buyer’s right with the seller’s obligation. The buyer and seller do not have the same contract exposure.

Mistake 2: Treating the premium as the full risk for every participant. That shortcut may fit a simple buyer-side view, but it can fail badly for seller-side obligations or multi-leg structures.

Mistake 3: Reading an option chain as if it were a strategy menu. A chain displays contract terms and quotes; it does not choose a strategy.

Mistake 4: Ignoring expiration. Time is part of the contract’s design, not a minor label.

Mistake 5: Treating volatility as optional. Volatility can affect option pricing even when the underlying asset’s price movement looks modest.

Mistake 6: Assuming options are always safer or cheaper than stock exposure. Lower upfront premium does not automatically mean lower total risk or better exposure quality.

Which Options Concept to Study Next

Options basics are easiest to learn as a sequence. The contract terms come first, then the rights and obligations, then the quote and risk interpretation layers.

| Question you are trying to answer | Concept to study next | Why it comes next |

|---|---|---|

| What does the buyer control when the contract is a call? | Call option | It explains the right attached to buying the underlying at the strike price |

| When does the contract right end? | Expiration date | It sets the time boundary for the contract |

| What happens when the buyer uses the contract right? | Exercise | It connects the contract right to the next mechanical step |

| What can happen to the seller when the right is used? | Assignment | It explains the seller-side obligation boundary |

| How much of the option price is built from immediate value versus remaining time and uncertainty? | Intrinsic and extrinsic value | It separates the premium into more useful interpretation parts |

| How readable is the contract quote? | Options liquidity | It helps interpret bid-ask spread, activity, and friction |

The sequence should stay concept-first. Contract identity explains what the option is, rights and obligations explain who can do what, and quote interpretation explains why two contracts with similar labels can behave differently.

FAQ

What are options in simple terms?

Options are contracts tied to an underlying asset. They give the buyer a defined right and create a different obligation profile for the seller, with terms such as strike price, premium, and expiration setting the basic structure.

What is the difference between a call and a put?

A call gives the buyer a right related to buying the underlying asset at the strike price. A put gives the buyer a right related to selling the underlying asset at the strike price.

Is the premium the full risk of an option?

For a simple buyer-side contract, the premium paid is a central risk boundary. For sellers or more complex structures, premium alone does not describe the full exposure.

What is exercise in options?

Exercise means using the option right under the contract terms. It is related to assignment, but assignment describes the seller-side obligation process.

Are options basics the same as learning an options strategy?

No. Options basics focus on contract terms, rights, obligations, quotes, and risk boundaries. Strategy selection requires additional analysis and is a separate layer.