Reading an option chain means interpreting the contract terms, quoted prices, activity levels, sensitivity measures, and expiration boundaries shown for available option contracts.

An option chain is not a recommendation screen. It shows what contracts exist, how they are priced, how active they appear, and which variables can change the contract’s payoff and risk profile before expiration.

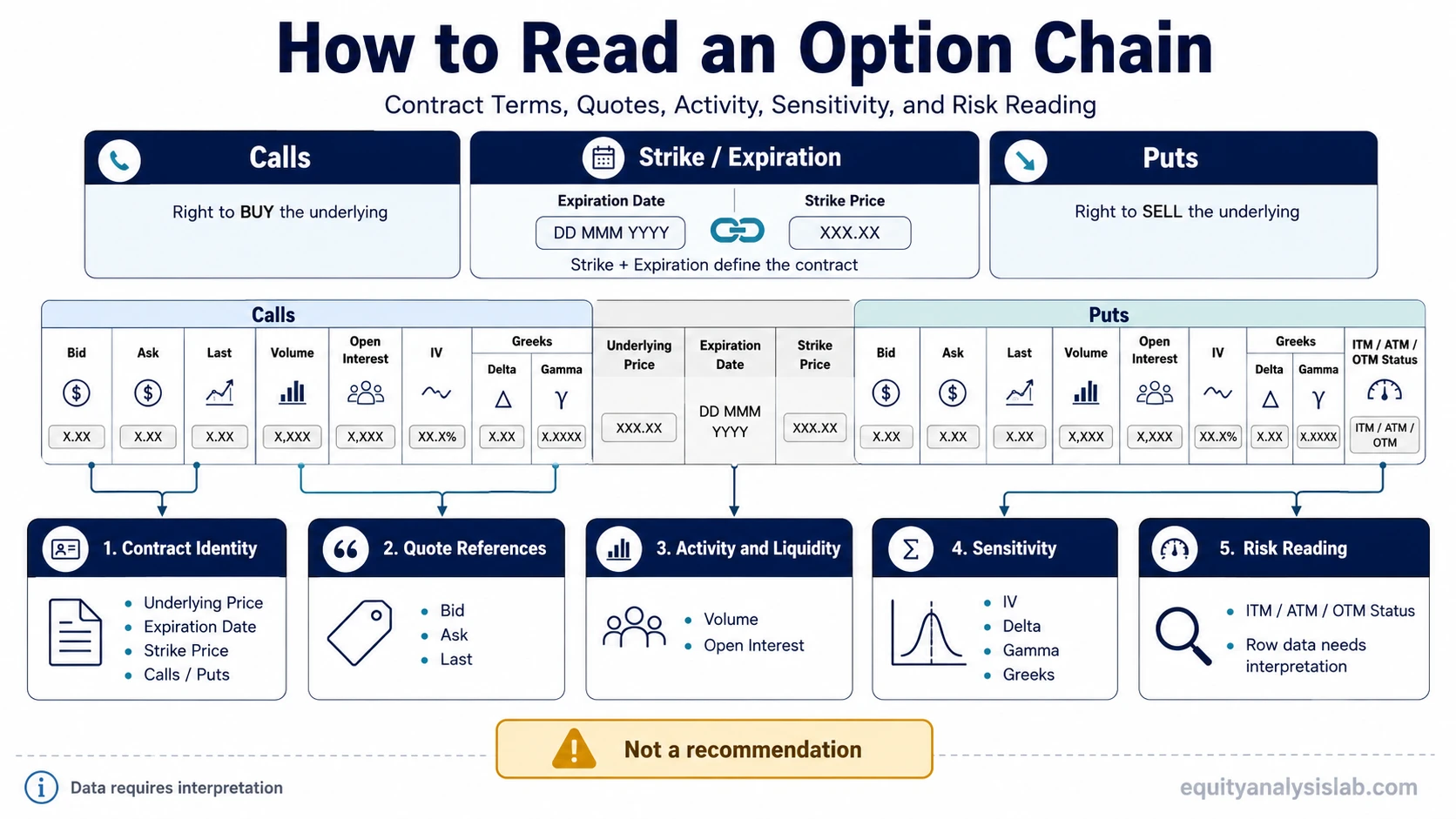

What an Option Chain Shows

An option chain groups available contracts for the same underlying asset. The two main sides are calls and puts. A call option gives the holder the right to buy the underlying at a strike price, while a put gives the holder the right to sell the underlying at a strike price.

The chain usually organizes contracts by expiration date and strike price. Each row then shows quoted market data for that strike, such as bid, ask, last price, volume, open interest, implied volatility, and sometimes Greeks.

The useful reading process starts by separating three layers: contract identity, quoted price, and interpretation risk. Contract identity tells the reader what the contract is. Quoted price shows what the market is displaying. Interpretation risk explains why the quote may not mean the contract is attractive, liquid, or suitable.

How to Read the Main Option Chain Columns

The core columns of an option chain are easier to read when each one is treated as a different type of information rather than as a single decision signal.

| Column or field | What it shows | How to interpret it carefully |

|---|---|---|

| Call / put side | Whether the contract is a call or a put. | The contract type changes the payoff direction and the way moneyness is measured. |

| Strike price | The price level written into the option contract. | The strike helps define whether the option is in the money, at the money, or out of the money. |

| Expiration | The date or time boundary when the option contract reaches expiration. | Shorter and longer expirations can behave differently because time remaining affects premium, time decay, and sensitivity. |

| Bid | The displayed price buyers are currently showing. | A low bid or wide spread can make the displayed value less reliable as a clean valuation reference. |

| Ask | The displayed price sellers are currently asking. | The ask may be meaningfully higher than the bid, so the spread matters before interpreting cost. |

| Last | The last reported transaction price. | Last price can be stale when activity is low, so it should not be treated as the current executable price by itself. |

| Volume | The number of contracts traded during the current session. | Volume shows current activity, not necessarily long-term interest or reliable exit quality. |

| Open interest | The number of outstanding contracts that remain open. | Open interest can show participation, but it does not guarantee a tight spread or active current trading. |

| Implied volatility | The volatility assumption reflected in the option’s market price. | Higher IV can raise premium, but it is not a standalone signal that the contract is better or worse. |

| Greeks | Sensitivity measures such as delta, gamma, theta, and vega. | Greeks describe how the option may respond to changes in price, time, and volatility; they do not remove risk. |

How Strike, Expiration, and Premium Change Interpretation

The strike price defines the contract’s reference price. For calls, lower strikes are usually more likely to be in the money when the underlying price is above the strike. For puts, higher strikes are usually more likely to be in the money when the underlying price is below the strike.

Expiration defines the remaining time boundary. A contract with more time remaining can carry more time value, while a contract close to expiration can become more sensitive to immediate price movement, time decay, and liquidity conditions.

Premium is the quoted cost or value of the option contract before contract multiplier, fees, and execution effects are considered. It can include intrinsic value, time value, volatility expectations, and market supply-demand conditions.

Why Moneyness Does Not Tell the Whole Story

Moneyness compares the underlying price with the strike price. It helps classify whether a contract is in the money, at the money, or out of the money.

That classification is useful, but it is incomplete. In-the-money status does not include the premium paid, the bid-ask spread, time remaining, implied volatility, fees, or the path of the underlying before expiration.

| Reading point | Useful information | Important limitation |

|---|---|---|

| In the money | The contract has intrinsic value based on the current underlying price and strike. | It can still be unprofitable after premium, spread, and transaction costs. |

| At the money | The underlying price is near the strike price. | Small price changes, volatility changes, and time decay can strongly affect interpretation. |

| Out of the money | The contract has no intrinsic value at the current underlying price. | Its premium may still reflect time value, volatility expectations, and event risk. |

Common Mistakes When Reading an Option Chain

Mistake 1: Treating last price as the current market. Last price is only the last reported trade. The bid and ask usually provide a more current view of the displayed market.

Mistake 2: Ignoring the bid-ask spread. A wide spread can make a contract look easier to value than it really is. Spread quality is part of liquidity reading.

Mistake 3: Reading open interest as current demand. Open interest shows contracts that remain open, while volume shows current session activity. They answer different questions.

Mistake 4: Assuming Greeks are recommendations. Greeks are sensitivity measures. They describe exposure to price, time, and volatility changes, but they do not say whether the contract should be used.

Mistake 5: Confusing moneyness with profit. A contract can be in the money and still produce an unfavorable result after premium, spread, timing, and transaction costs.

How Option Chain Reading Connects to Contract Risk

An option chain can show where contract risk begins to appear, but it cannot remove that risk. Premium, spread, expiration, implied volatility, and sensitivity measures all affect how the contract may behave before it is closed, exercised, assigned, or allowed to expire.

For some contracts, exercise option mechanics can also change the practical interpretation because the contract right may connect to buying or selling the underlying shares. That does not mean exercise is always relevant, but it shows why contract terms must be understood before interpreting quoted prices.

The safest way to read an option chain is to separate what the row displays from what the row does not prove. The row displays terms, quotes, activity, and sensitivity. It does not prove suitability, liquidity quality, expected return, or final outcome.

FAQ

What is the first thing to check in an option chain?

Start with the underlying price, expiration date, contract type, and strike price. Those fields define what contract is being shown before price, liquidity, volatility, and sensitivity measures are interpreted.

Is the last price the same as the current option price?

No. Last price is the most recent reported trade. The current bid and ask are usually more relevant for understanding the displayed market, especially when volume is low or the spread is wide.

Does high open interest mean an option is liquid?

High open interest can show that many contracts remain outstanding, but it does not guarantee a tight bid-ask spread or easy execution. Liquidity should be judged with spread, volume, and current quotes together.

Does in-the-money status mean the option is profitable?

No. In-the-money status only compares the underlying price with the strike price. Premium paid, spread, time decay, volatility changes, and transaction costs can still affect the final result.