Intrinsic value is the part of an option premium that exists if the contract is exercised now, while extrinsic value is the part paid for time, volatility, and uncertainty before expiration.

The distinction helps explain premium composition. It does not show whether an option is profitable, attractive, cheap, expensive, or suitable for any investor.

Intrinsic Value vs Extrinsic Value: The Core Difference

- Intrinsic value answers what value exists from immediate exercise.

- Extrinsic value answers how much premium remains beyond immediate exercise value.

- An out-of-the-money option has zero intrinsic value, but it can still have extrinsic value.

- Extrinsic value is most closely linked to time to expiration, implied volatility, and uncertainty around the underlying price.

- Neither value component proves profit, contract quality, or investment suitability by itself.

How Option Premium Splits Between Intrinsic and Extrinsic Value

An option premium can be read as two parts: immediate exercise value and everything paid above that amount. The immediate exercise portion is intrinsic value. The remaining portion is extrinsic value, also commonly called time value when the focus is on the premium that can disappear as expiration approaches.

Premium decomposition: option premium = intrinsic value + extrinsic value.

Extrinsic value: option premium − intrinsic value.

Extrinsic value represents premium above immediate exercise value. It is not a guaranteed future payoff, and it can change as time, implied volatility, and expected movement change.

Intrinsic Value Rules for Calls and Puts

Intrinsic value depends on the contract type because calls and puts benefit from opposite price relationships. A call has intrinsic value when the underlying price is above the strike price. A put has intrinsic value when the strike price is above the underlying price.

| Contract type | Intrinsic value rule | When intrinsic value is zero |

|---|---|---|

| Call option | max(0, underlying price − strike price) | When the underlying price is at or below the strike price |

| Put option | max(0, strike price − underlying price) | When the underlying price is at or above the strike price |

The max(0, …) structure matters because intrinsic value cannot be negative. If immediate exercise would not create value, intrinsic value is simply zero.

Intrinsic Value vs Extrinsic Value by Comparison Criteria

The useful comparison is not which component is better. The useful comparison is which question each component answers inside the option premium.

| Comparison point | Intrinsic value | Extrinsic value |

|---|---|---|

| Main question | What value exists if the option is exercised now? | How much premium remains for time, volatility, and uncertainty? |

| Premium role | The immediate exercise-value portion of the premium | The premium above intrinsic value |

| Call option test | Underlying price above strike price | Premium remaining after call intrinsic value is removed |

| Put option test | Strike price above underlying price | Premium remaining after put intrinsic value is removed |

| Out-of-the-money status | Zero | Can still be positive |

| Expiration effect | Depends on final moneyness at expiration | Tends to shrink as time value runs out, all else equal |

| Common mistake | Treating it as realized profit | Treating it as guaranteed future value |

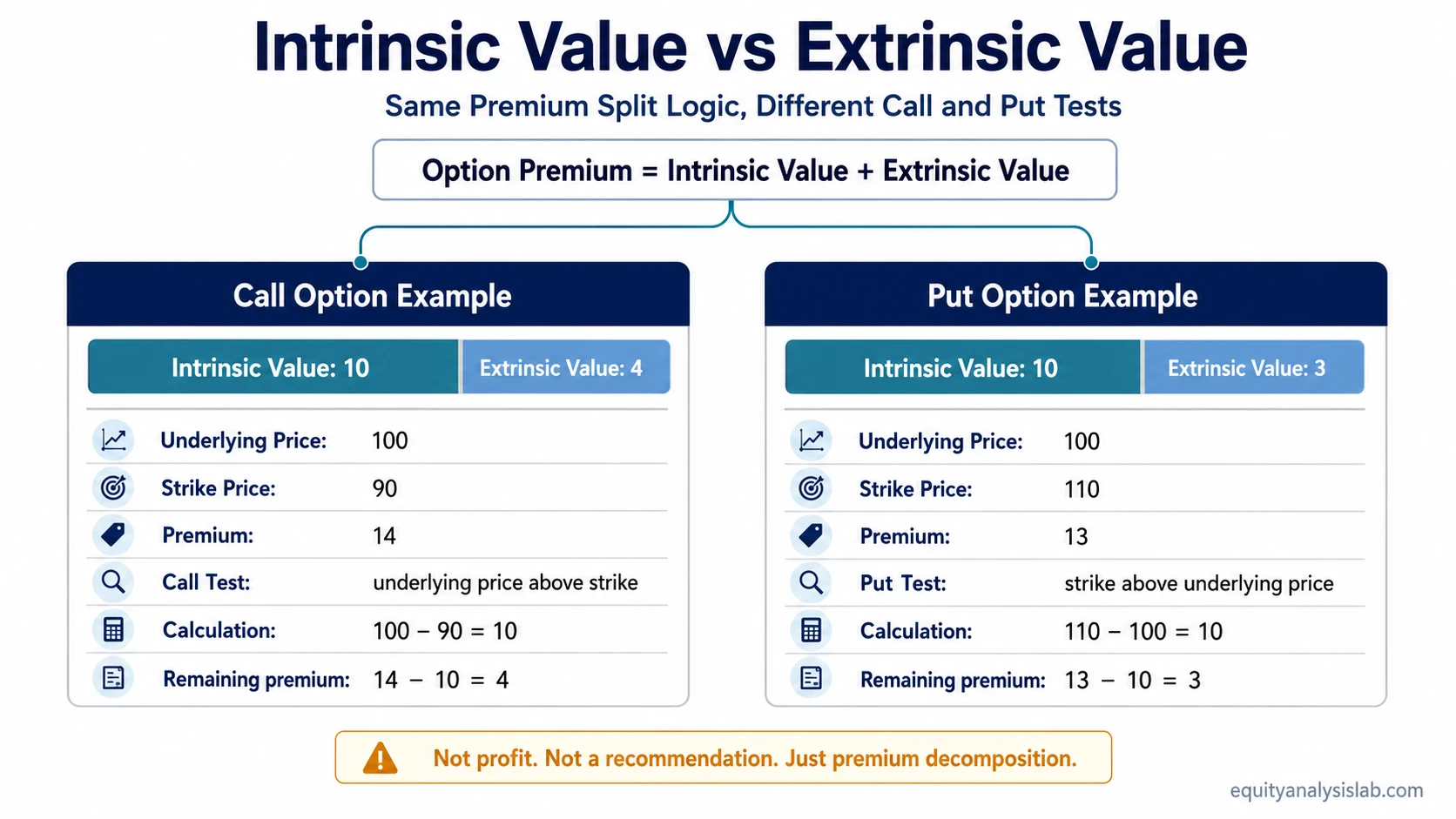

Same Scenario: Call and Put Intrinsic and Extrinsic Value

Assume the underlying price is 100. A call with a 90 strike and a put with a 110 strike both have 10 points of intrinsic value, but for opposite reasons. The call is valuable on immediate exercise because the underlying price is above the strike. The put is valuable on immediate exercise because the strike is above the underlying price.

Underlying price: 100

Call strike: 90

Call premium: 14

Call intrinsic value: 100 − 90 = 10

Call extrinsic value: 14 − 10 = 4

Underlying price: 100

Put strike: 110

Put premium: 13

Put intrinsic value: 110 − 100 = 10

Put extrinsic value: 13 − 10 = 3

The intrinsic value is the immediate exercise-value portion in both examples. The extrinsic value is the remaining premium, which reflects time to expiration, implied volatility, and uncertainty about what may happen before the contract expires.

When Extrinsic Value Changes Before Expiration

Extrinsic value can change even when intrinsic value is unchanged. Time to expiration, implied volatility, expected movement, interest-rate assumptions, dividends when relevant, and market supply-demand conditions can all affect the premium paid above immediate exercise value.

Time decay is the most visible boundary for many contracts. As expiration gets closer, less time remains for the underlying price to move in a favorable direction. All else equal, that reduces the time-related portion of the premium.

Important boundary: extrinsic value is not guaranteed future value. It is a market price for uncertainty before expiration, and that price can rise, fall, or disappear depending on contract conditions.

Common Confusion: Intrinsic Value Is Not Profit

Intrinsic value is not the same as profit because profit depends on the total premium paid, transaction costs where relevant, contract handling, and the price path after entry. A call with 10 points of intrinsic value is not automatically profitable if the buyer paid more than that amount for the contract.

Higher intrinsic value also does not automatically mean a better option contract. A contract can have high intrinsic value and still be expensive, illiquid, close to expiration, or unsuitable for a particular purpose. A contract with zero intrinsic value can still have extrinsic value if the market assigns value to time and possible future movement.

Intrinsic value options are best read as immediate exercise-value mechanics. The comparison here keeps the focus on how that value separates from the remaining premium.

How This Connects to ITM, OTM, Exercise, and Assignment

Intrinsic and extrinsic value are closely related to moneyness, but they are not the same concept. In-the-money options have intrinsic value. Out-of-the-money options have zero intrinsic value. At-the-money options usually have little or no intrinsic value, but they may still carry extrinsic value.

Exercise and assignment are contract actions, not value components. Intrinsic value explains what immediate exercise value exists, while extrinsic value explains how much of the premium sits beyond that immediate value. That distinction helps with contract reading, not with deciding whether to exercise, hold, close, or open a position.

Where the Distinction Breaks Down

The labels become misleading when they are treated as interchangeable. Intrinsic value describes immediate exercise value. Extrinsic value describes premium beyond that immediate value. Neither label alone proves profit, suitability, risk/reward, or investment attractiveness.

The cleanest use is diagnostic: identify the option type, compare the underlying price with the strike, calculate intrinsic value, subtract that amount from the premium, and then interpret the remaining premium as extrinsic value subject to time, volatility, and expiration risk.

FAQ

Can an option have extrinsic value but no intrinsic value?

Yes. An out-of-the-money option has zero intrinsic value, but it can still have extrinsic value if the market assigns value to time, volatility, and possible movement before expiration.

Is intrinsic value the same as profit?

No. Intrinsic value only measures immediate exercise value. Profit depends on the premium paid, costs, timing, and how the contract is handled.

What happens to extrinsic value at expiration?

At expiration, remaining time value disappears. The option’s value is then determined by whether it has intrinsic value based on the final relationship between the underlying price and the strike price.

Do calls and puts calculate intrinsic value the same way?

No. A call has intrinsic value when the underlying price is above the strike price. A put has intrinsic value when the strike price is above the underlying price.