In the money and out of the money describe whether an option has intrinsic value based on the relationship between its strike price and the current price of the underlying asset.

Calls and puts use opposite moneyness tests. A call is in the money when the underlying price is above the strike price, while a put is in the money when the underlying price is below the strike price. Out of the money means the strike relationship is not favorable for intrinsic value at that moment, although the contract may still trade with premium because time, volatility expectations, and market demand can still have value.

Core distinction: An ITM option contains intrinsic value before premium costs are considered. An OTM option does not contain intrinsic value at the current underlying price.

Key Points

- ITM and OTM are moneyness labels based on strike price versus underlying price.

- Calls and puts use opposite directional tests.

- ITM options contain intrinsic value; OTM options do not contain intrinsic value at the current price.

- OTM options can still have premium because premium can include time value and volatility expectations.

- Moneyness is a contract-status label, not a quality rating or return forecast.

What Is the Difference Between In the Money and Out of the Money?

The difference between in the money and out of the money is whether the option would have built-in value if exercised before considering the premium paid. A call becomes ITM when the underlying price is above the strike. A put becomes ITM when the underlying price is below the strike.

An in-the-money option has value built into the contract because its strike is favorable relative to the current underlying price. An OTM option does not have that built-in value, but it may still have market value if there is time left before expiration or if expected volatility is high.

An out-of-the-money option is not worthless simply because built-in value is absent. The narrower point is that OTM means no intrinsic value at the current underlying price, not zero premium and not zero possibility of future movement.

In the Money vs Out of the Money Criteria

The same strike can be interpreted differently depending on whether the contract is a call or a put. The comparison starts with the contract type, then checks the strike price against the underlying price.

| Criteria | In the Money | Out of the Money | Limit of the Label |

|---|---|---|---|

| Call option | Strike price is below the underlying price. | Strike price is above the underlying price. | The label does not show whether the call creates a net gain after premium. |

| Put option | Strike price is above the underlying price. | Strike price is below the underlying price. | The label does not rank the put as a better or worse contract choice. |

| Intrinsic value | Present before premium costs are considered. | Absent at the current underlying price. | Moneyness alone does not measure the total economic result. |

| Premium | Usually includes intrinsic value plus possible time value. | May still include time value and volatility expectations. | Premium level requires separate interpretation. |

| Expiration implication | May retain intrinsic value if still ITM at expiration. | May expire without intrinsic value if still OTM at expiration. | Contract terms and settlement mechanics still matter. |

How Calls and Puts Change the Moneyness Test

Call options and put options move through the moneyness test in opposite directions because they represent opposite rights. A call gives the right to buy the underlying at the strike price, so a lower strike becomes favorable when the underlying price is higher. A put gives the right to sell the underlying at the strike price, so a higher strike becomes favorable when the underlying price is lower.

This reversal is the main source of confusion. ITM does not always mean “price above strike.” It means the strike relationship is favorable for that specific contract type. OTM means the strike relationship is unfavorable for built-in value at that moment.

ATM boundary note: At the money sits near the strike-price boundary. It can help describe the transition between ITM and OTM, but the core comparison remains the two statuses on either side of that boundary.

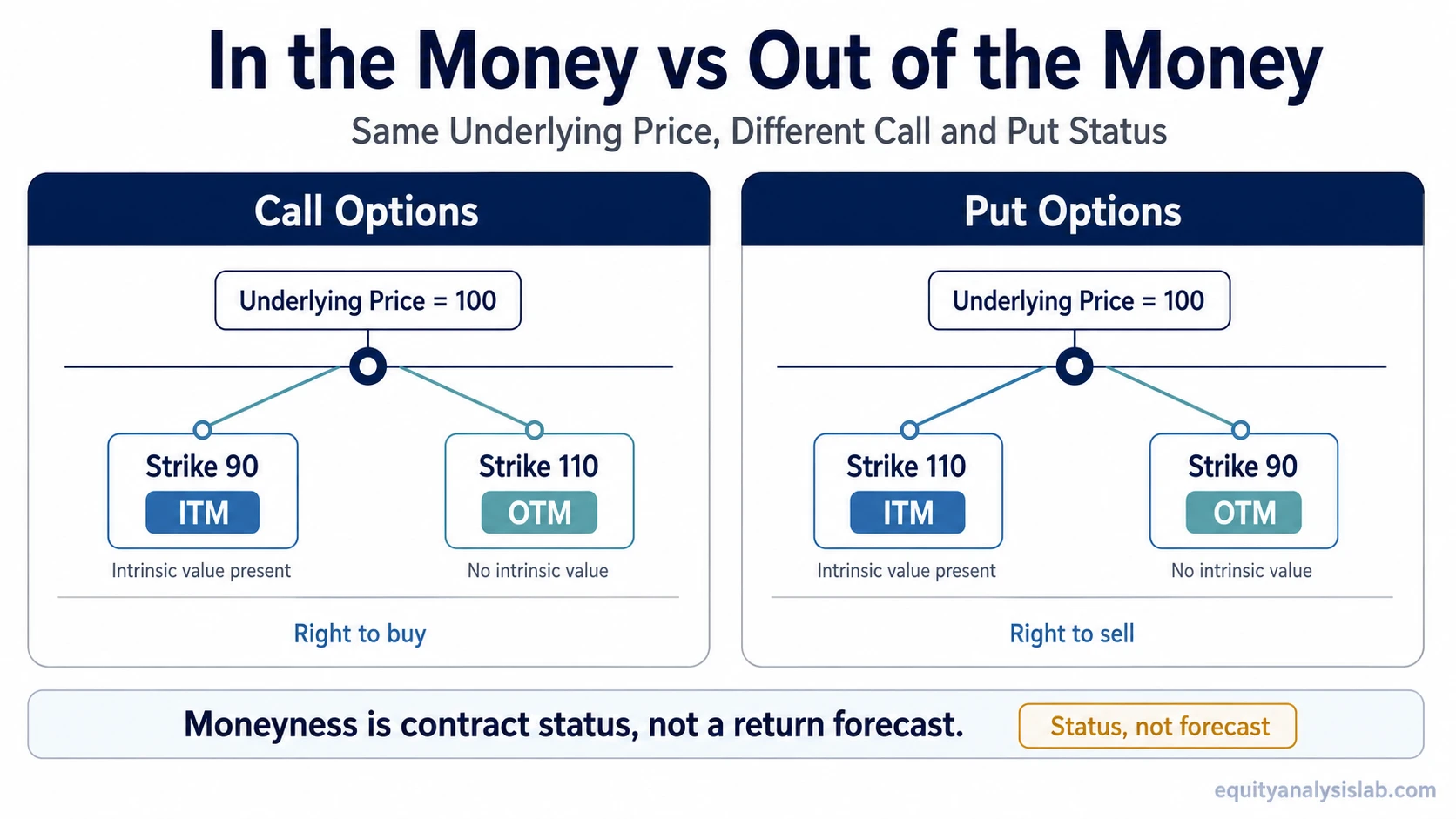

Same Underlying, Different Option Status

Consider an underlying asset trading at 100 with two call options that share the same expiration. A 90 strike call is in the money because the right to buy at 90 has built-in value while the underlying trades at 100. A 110 strike call is out of the money because buying at 110 is not favorable while the underlying trades at 100.

The same underlying price creates the opposite status for puts. With the underlying at 100, a 110 strike put is in the money because the right to sell at 110 has built-in value. A 90 strike put is out of the money because selling at 90 is not favorable while the underlying trades at 100.

| Contract | Underlying Price | Strike Price | Status | Reason |

|---|---|---|---|---|

| Call | 100 | 90 | ITM | The right to buy at 90 is favorable when the underlying trades at 100. |

| Call | 100 | 110 | OTM | The right to buy at 110 is not favorable while the underlying trades at 100. |

| Put | 100 | 110 | ITM | The right to sell at 110 is favorable when the underlying trades at 100. |

| Put | 100 | 90 | OTM | The right to sell at 90 is not favorable while the underlying trades at 100. |

Common Mistakes When Comparing ITM and OTM Options

| Mistake | Safer interpretation |

|---|---|

| Treating OTM premium as automatically attractive because the contract appears cheaper. | A lower premium does not say whether the contract has favorable economics, enough time, or a reasonable risk profile. |

| Treating ITM status as automatic profitability. | Built-in value does not account for premium paid, bid-ask spread, fees, tax treatment, or later changes in the underlying price. |

| Treating moneyness as a forecast. | ITM and OTM describe current contract status, not whether the underlying will move in a favorable direction. |

The cleanest distinction is mechanical. Moneyness answers one question: does the option have intrinsic value based on the current relationship between strike price and underlying price?

What the Distinction Helps Investors Check

ITM versus OTM helps investors read an option contract more accurately before moving into broader interpretation. The label clarifies whether the option already contains built-in value, how the strike relates to the underlying, and why premium may differ between contracts with the same expiration.

The distinction is useful for contract literacy, scenario analysis, and understanding option-chain language. It is not enough to decide whether a contract is suitable, fairly priced, or consistent with a portfolio objective. Premium, time to expiration, volatility assumptions, liquidity, position size, and the underlying investment thesis still matter.

Boundary: ITM and OTM describe moneyness. They do not replace valuation work, portfolio risk controls, or a full options strategy framework.

Expiration and Exercise Boundary

Expiration makes the moneyness label more consequential because built-in value can determine whether an option has value at the contract deadline. An ITM option may have intrinsic value at expiration, while an OTM option may expire without intrinsic value if the underlying price remains on the unfavorable side of the strike.

Operational outcomes can still depend on contract specifications, settlement type, account rules, and broker procedures. The useful comparison remains the moneyness label, not the full exercise or assignment workflow.

FAQ

Can an out-of-the-money option still have value?

Yes. An OTM option can still trade with premium because time to expiration, expected volatility, and market demand can give the contract value even without intrinsic value.

Is an in-the-money option always better than an out-of-the-money option?

No. ITM status only describes intrinsic value. It does not prove that the contract is suitable, fairly priced, or likely to produce a favorable economic result after premium and costs.

Why do calls and puts use opposite ITM and OTM tests?

Calls give the right to buy, so a strike below the underlying price is favorable. Puts give the right to sell, so a strike above the underlying price is favorable.