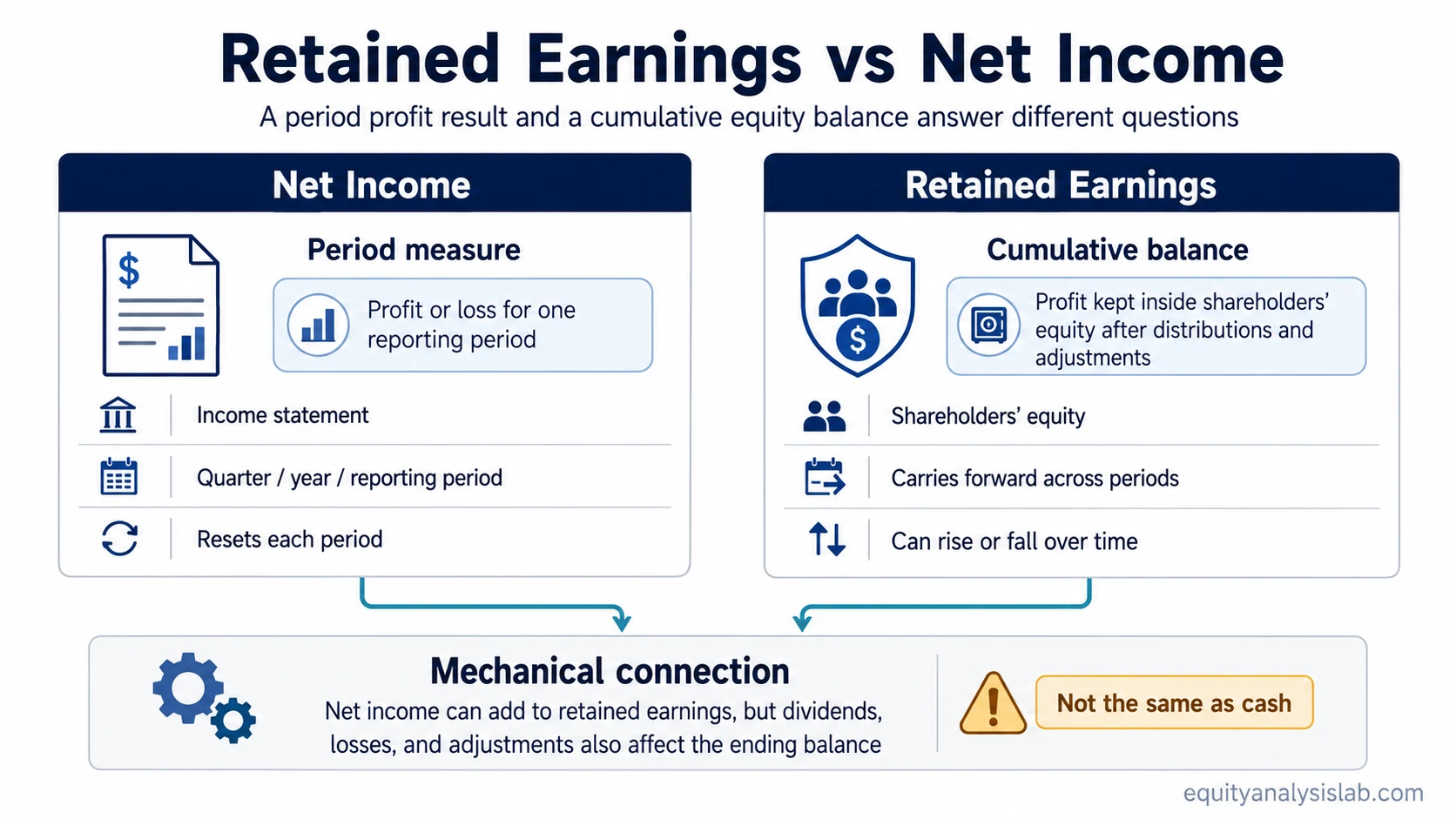

Net income measures profit or loss for one reporting period, while retained earnings shows the cumulative profit kept inside shareholders’ equity after dividends, losses, and adjustments.

Net income appears on the income statement and resets with each reporting period. It is a period measure, not a running equity balance.

Retained earnings is part of shareholders’ equity. It accumulates past profits that have not been distributed as dividends, but it can also be reduced by losses, dividends, and certain accounting adjustments.

Key Points

- Net income answers whether the company earned a profit or loss during a specific period.

- Retained earnings answers how much cumulative profit has been kept inside equity after distributions and prior effects.

- Net income can increase retained earnings, but dividends or losses can still make retained earnings fall.

- Neither number alone proves cash generation, earnings quality, or valuation attractiveness.

Retained Earnings vs Net Income in One Sentence

Definition: Net income is the current-period profit result, while retained earnings is the cumulative equity balance created by retained profit after dividends, losses, and adjustments.

The two measures are connected, but they answer different questions. Net income is a flow through the income statement. Retained earnings is a stock of accumulated profit inside shareholders’ equity.

The connection is mechanical rather than interchangeable. A profitable period usually adds to retained earnings, but the final retained earnings balance also reflects dividends, earlier deficits, restatements, and other equity adjustments.

Net Income vs Retained Earnings Comparison Table

| Comparison point | Net income | Retained earnings |

|---|---|---|

| Main question answered | Did the company make a profit or loss during the period? | How much cumulative profit has been kept inside shareholders’ equity? |

| Financial statement placement | Reported on the income statement. | Reported within shareholders’ equity and often explained through a retained earnings or shareholders’ equity movement. |

| Timing | Period-based: quarter, year, or another reporting period. | Cumulative: carries forward from prior periods. |

| Formula role | Feeds the retained earnings roll-forward as the current-period profit or loss input. | Starts with the prior balance, adds net income or subtracts net loss, then adjusts for dividends and other items. |

| Dividend effect | Dividends are not an expense in net income. | Dividends reduce retained earnings because they distribute profit to shareholders. |

| Equity effect | Net income can increase shareholders’ equity after the period closes. | Retained earnings is already part of shareholders’ equity. |

| Common misread | A profitable period does not automatically mean retained earnings increased. | A large retained earnings balance does not mean the company holds the same amount in cash. |

| Investor use | Useful for period profitability and earnings trends. | Useful for understanding accumulated profit, dividend history, losses, and equity mechanics. |

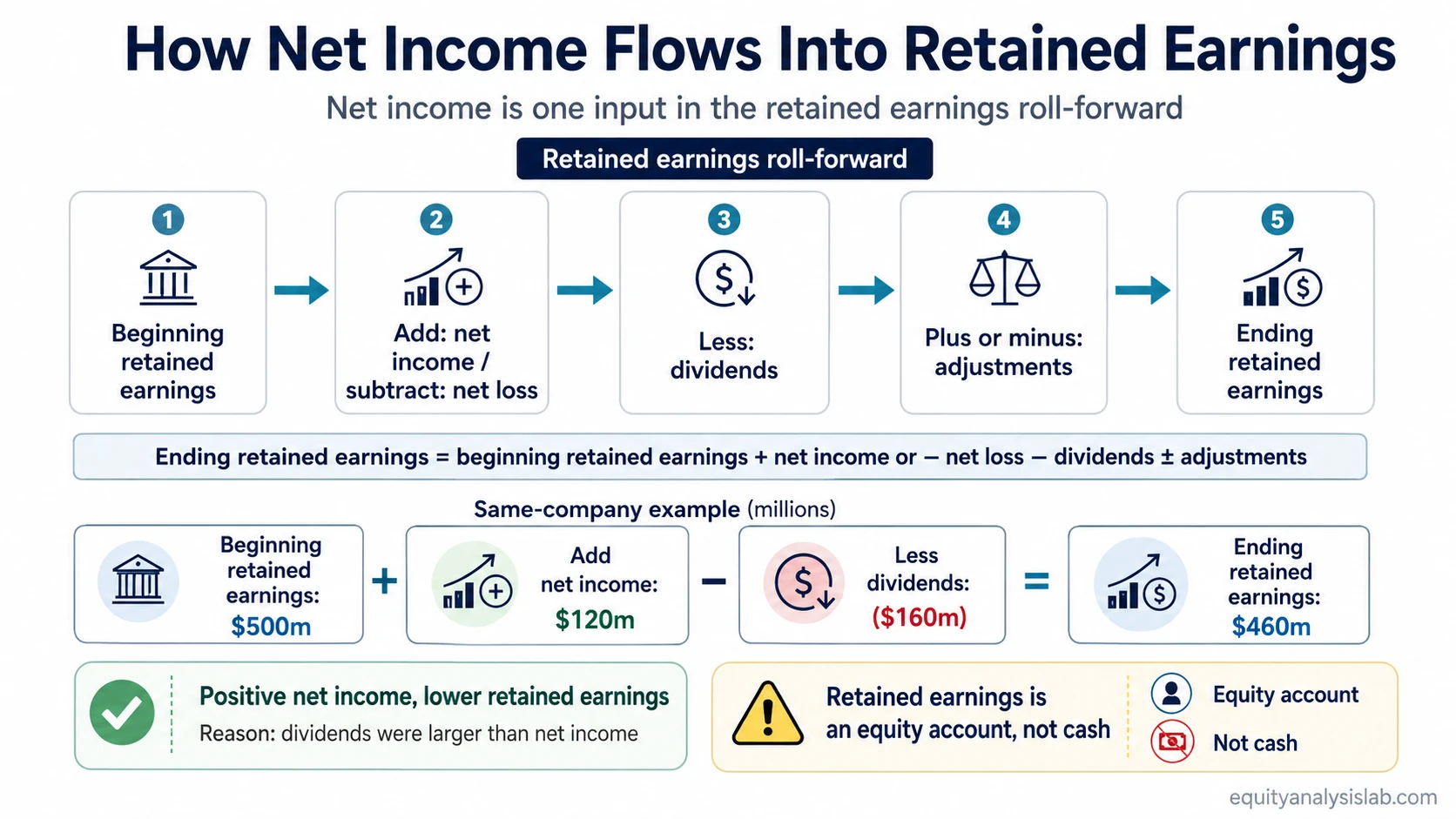

How Net Income Flows Into Retained Earnings

Retained earnings usually moves through a roll-forward:

Ending retained earnings = beginning retained earnings + net income or − net loss − dividends ± accounting adjustments.

This formula explains why net income and retained earnings can move in different ways. Net income is one input. Dividends, prior accumulated losses, and certain equity adjustments can change the ending balance even when the company reports a profit.

A net loss works in the opposite direction. Instead of adding to retained earnings, it reduces the accumulated balance and can contribute to an accumulated deficit if losses exceed retained profits over time.

Same-Company Retained Earnings and Net Income Example

Illustrative example: A company begins the year with $500 million of retained earnings. During the year, it earns $120 million of net income and pays $160 million in dividends.

| Retained earnings movement | Amount |

|---|---|

| Beginning retained earnings | $500 million |

| Add: net income | $120 million |

| Less: dividends | ($160 million) |

| Ending retained earnings | $460 million |

The company was profitable, but retained earnings still declined because dividends were larger than net income. The period profit was $120 million, while the ending cumulative retained earnings balance was $460 million.

The same logic can work in the other direction. If the company earned $120 million and paid no dividends, retained earnings would rise before considering other adjustments.

Why Investors Confuse Retained Earnings and Net Income

The confusion usually comes from the flow-through relationship. Net income closes into equity, so it affects retained earnings, but it does not become the same number.

Common mistake: Treating retained earnings as “profit this year” mixes a period result with a cumulative balance. Treating retained earnings as cash creates a second error because accumulated profit may have been reinvested, used to repay debt, used for working capital, or distributed through dividends.

A second mistake is assuming that higher retained earnings automatically proves stronger business quality. The balance can reflect long operating history, conservative dividend policy, accounting accumulation, prior profitability, or limited distributions. It still needs to be interpreted with cash flow, reinvestment returns, leverage, and earnings durability.

How Investors Can Read Both Measures

Net income helps frame period profitability, margin direction, earnings growth, and whether reported performance improved or weakened during the reporting window.

Retained earnings helps frame how profits have accumulated inside equity, how distributions changed that accumulation, and whether prior losses or adjustments shaped the equity base.

Because retained earnings is part of shareholders’ equity, it can affect book equity interpretation and metrics such as book value per share. The balance still needs context: a company can have retained earnings without matching cash, and a profitable period can still produce weak cash conversion.

Limitation: Net income, retained earnings, and book equity are accounting measures. They can support company analysis, but they do not replace cash-flow analysis, earnings-quality review, capital-allocation judgment, or valuation work.

FAQ

Is retained earnings the same as net income?

No. Net income is profit or loss for one reporting period. Retained earnings is the cumulative profit kept inside shareholders’ equity after dividends, losses, and adjustments.

Does net income increase retained earnings?

Net income usually increases retained earnings after the period closes, but dividends, net losses, and certain accounting adjustments can reduce the ending retained earnings balance.

Can retained earnings go down when net income is positive?

Yes. Retained earnings can fall even when net income is positive if dividends or other reductions are larger than the profit added during the period.

Are retained earnings cash?

No. Retained earnings is an equity account, not a cash account. The accumulated profit may have been reinvested in assets, used in operations, used to reduce debt, or distributed through dividends.