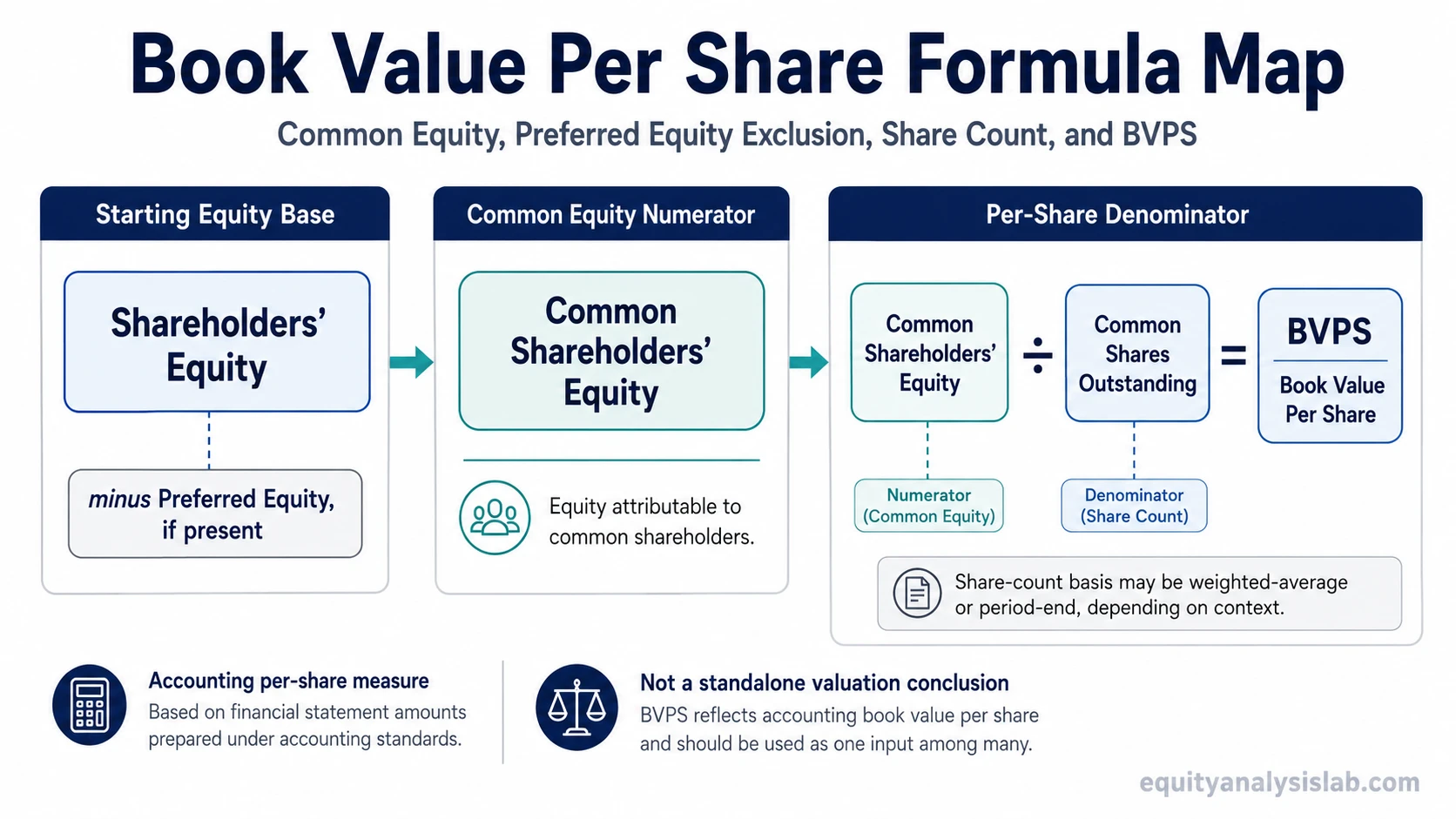

Book value per share is the amount of accounting common equity behind each common share outstanding. It is usually calculated as common shareholders’ equity divided by common shares outstanding, with preferred equity excluded when relevant. BVPS can help compare book equity per share with market value per share, but it does not prove that a stock is cheap, safe, high quality, or likely to produce a future return.

Book value per share: an accounting equity-per-share measure that converts a company’s common equity base into a per-common-share amount.

BVPS works by taking equity from the balance sheet, removing claims that do not belong to common shareholders when needed, and dividing the remaining common equity by the common share base. That makes it a denominator-based measure, not a complete valuation conclusion.

Key Points

- BVPS measures accounting common equity per common share.

- Preferred equity is excluded when calculating common shareholders’ equity.

- Share count changes can affect the denominator and the interpretation.

- BVPS can be compared with market value per share, but it does not prove undervaluation.

- Historical cost accounting and intangible assets can limit usefulness.

Book Value Per Share Formula

The standard BVPS formula is:

Book value per share = (shareholders’ equity – preferred equity) / common shares outstanding

When a company has no preferred equity, the same idea is often expressed more simply as common shareholders’ equity divided by common shares outstanding.

| Formula input | What it means | Why it affects BVPS |

|---|---|---|

| Shareholders’ equity | The accounting equity base reported on the balance sheet. | It is the starting numerator before separating common and preferred claims. |

| Preferred equity | Equity claim assigned to preferred shareholders, when present. | It is subtracted because BVPS measures equity attributable to common shareholders. |

| Common shareholders’ equity | The equity amount left for common shareholders after preferred claims are removed. | It is the numerator used for common BVPS. |

| Common shares outstanding | The common share count used as the denominator. | It converts common equity into a per-share accounting amount. |

| Weighted average shares or period-end shares | The share-count basis used for the denominator, depending on the reporting or analysis context. | It matters when issuance, repurchases, or retirements changed the share count during the period. |

How to Calculate Book Value Per Share

To calculate book value per share, start with the equity base, subtract preferred equity if the company has preferred shares, and divide the result by common shares outstanding.

Illustrative calculation: A company reports $500 million of shareholders’ equity, including $50 million of preferred equity. It has 90 million common shares outstanding.

Common shareholders’ equity is $450 million, calculated as $500 million minus $50 million. BVPS is $5.00, calculated as $450 million divided by 90 million common shares.

The share-count basis can change the interpretation. If a company issued shares, repurchased shares, or retired shares during the period, a period-end share count can give a different impression from a weighted average share count. The right denominator depends on the analytical context and the financial statement presentation being used.

What Book Value Per Share Tells Investors

BVPS shows how much accounting common equity sits behind each common share. It can help separate the total equity number from the ownership denominator, which is useful when share issuance, buybacks, or retained losses have changed the capital structure.

For example, rising total equity does not automatically mean rising BVPS if the share count rises faster. A company can also report stable equity while BVPS changes because the denominator changed. That is why the per-share framing matters.

Retained earnings can increase shareholders’ equity over time when cumulative profits exceed distributions. An accumulated deficit can reduce equity when cumulative losses exceed retained profits. Both can flow into the equity base that BVPS uses.

Book Value Per Share vs Market Value Per Share

Book value per share and market value per share answer different questions. BVPS is based on accounting equity. Market value per share is the price investors currently assign to one common share in the market.

| Measure | Based on | What it shows | What it does not prove |

|---|---|---|---|

| Book value per share | Common shareholders’ equity and common shares outstanding. | Accounting common equity per common share. | It does not prove fair value, quality, safety, or expected return. |

| Market value per share | The stock price in the market. | The price investors are currently assigning to one share. | It does not prove that the accounting equity base is high quality or recoverable. |

A stock can trade above or below book value for many reasons, including expected earnings power, asset quality, leverage, industry structure, intangible assets, and investor expectations. The comparison is a starting point for analysis, not a conclusion by itself.

What Can Change Book Value Per Share

BVPS changes when either the numerator or denominator changes. The numerator changes when common equity changes. The denominator changes when the common share count changes.

| Driver | Common effect on BVPS | Interpretation caution |

|---|---|---|

| Profits retained in the business | Can increase common equity and BVPS. | The quality and durability of earnings still matter. |

| Net losses or write-downs | Can reduce common equity and BVPS. | The cause of the loss matters more than the accounting change alone. |

| Share issuance | Can increase the denominator and dilute BVPS if equity does not rise proportionally. | Issuance may fund value-creating or value-destroying activity, so context matters. |

| Share repurchases | Can reduce the denominator and raise BVPS if shares are bought below book value. | Repurchases do not automatically create value or improve business quality. |

| Preferred equity changes | Can change the amount of equity attributable to common shareholders. | Preferred claims should be separated from common claims when calculating common BVPS. |

Limitations of Book Value Per Share

Book value per share is limited because accounting equity is not the same as economic value. Many assets are recorded at historical cost, some assets may be impaired, and internally generated intangible value may not appear fully on the balance sheet.

BVPS limitation: the number can be useful for asset-heavy or balance-sheet-driven companies, but it can be less informative for companies whose value depends on intangible assets, network effects, software, brands, or future earnings power.

BVPS can also be distorted by capital structure. Preferred stock, treasury stock, accumulated losses, and buyback accounting can change the relationship between reported equity and the common-share denominator. A tangible equity lens may help when goodwill or other intangibles dominate the equity base, but even tangible book value remains an accounting measure.

The main mistake is treating BVPS as a standalone valuation verdict. A low price relative to BVPS does not automatically mean a stock is undervalued, and a high price relative to BVPS does not automatically mean a stock is overvalued. The business model, asset quality, earnings power, leverage, and reinvestment economics still matter.

Related Shareholders’ Equity Concepts

| Concept | How it relates to BVPS |

|---|---|

| Shareholders’ equity | The starting balance-sheet equity base before separating common and preferred claims. |

| Retained earnings | A cumulative profit component that can increase equity when profits are retained. |

| Accumulated deficit | A cumulative loss position that can reduce or eliminate common equity. |

| Tangible book value | A stricter equity measure that removes certain intangible assets from book equity. |

| Market value per share | The market price per share, which can be compared with BVPS but is not the same measure. |

FAQ

What is the book value per share formula?

Book value per share is usually calculated as shareholders’ equity minus preferred equity, divided by common shares outstanding. If there is no preferred equity, it can be calculated as common shareholders’ equity divided by common shares outstanding.

Is a higher book value per share always better?

No. A higher BVPS can show more accounting equity per common share, but it does not prove business quality, undervaluation, safety, or future return. Asset quality, earnings power, cash flow, and business model context still matter.

How is book value per share different from market value per share?

Book value per share is based on accounting common equity. Market value per share is the stock price assigned in the market. One is an accounting measure, and the other is a market-pricing measure.

Can book value per share be negative?

Yes. BVPS can be negative if common shareholders’ equity is negative. That can happen when accumulated losses, write-downs, liabilities, or capital structure effects reduce equity below zero.

Why can BVPS be less useful for asset-light companies?

Asset-light companies may rely on intangible assets, software, brands, customer relationships, or network effects that are not fully reflected in book equity. BVPS may understate or misrepresent the economics of those businesses.