Book value is not the same as market value, intrinsic value, or business quality. For a company, book value is the recorded accounting equity left after total liabilities are subtracted from total assets.

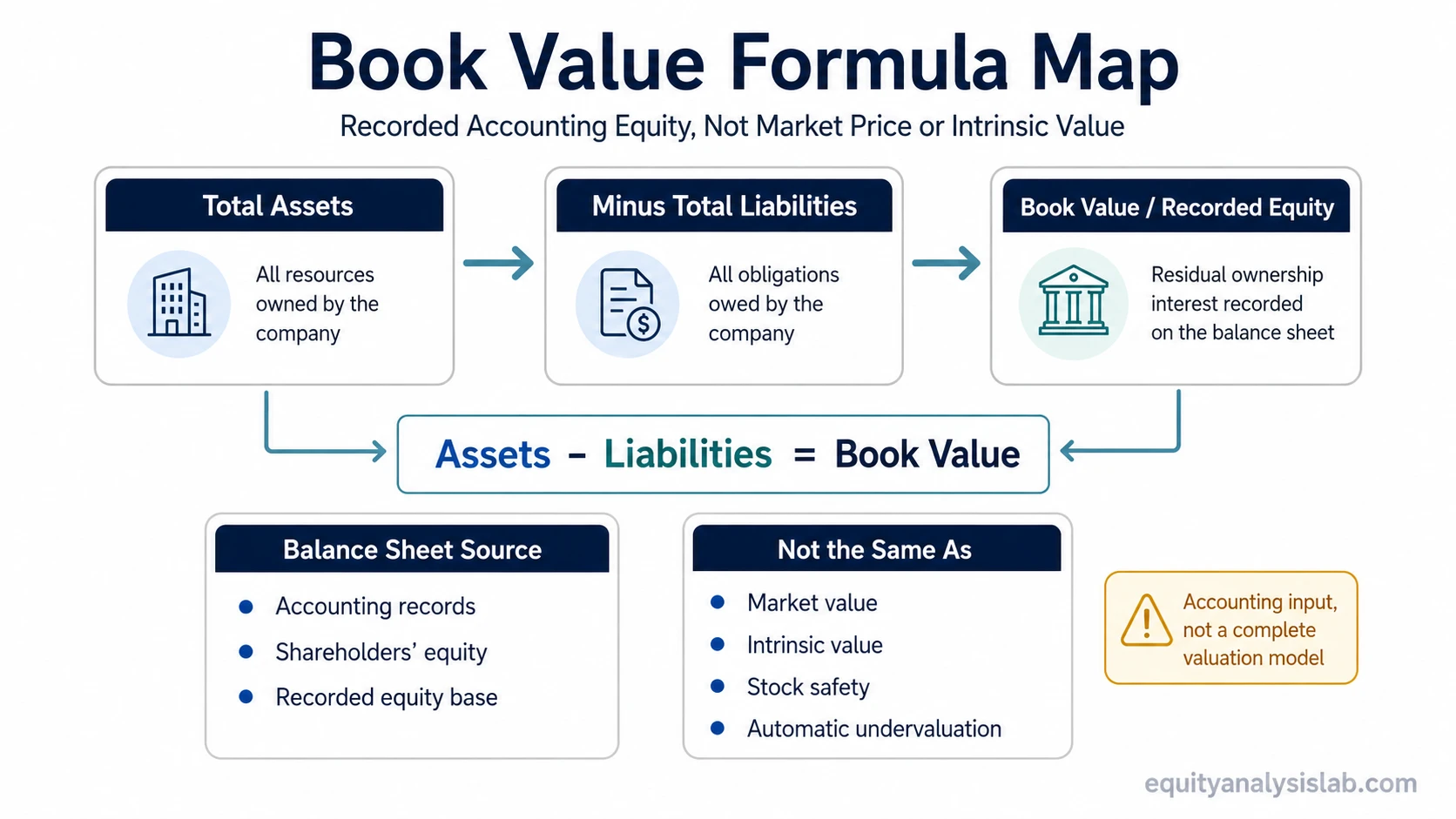

Definition: Book value is the accounting value of a company’s equity base, calculated as total assets minus total liabilities. On a company balance sheet, this usually corresponds to shareholders’ equity.

The number comes from accounting records, not from what investors currently pay for the stock. That makes book value useful for understanding the recorded balance-sheet base, but weak as a standalone judgment about what the business is worth.

Key Points

- Book value is usually calculated as total assets minus total liabilities.

- For a company, book value generally corresponds to recorded shareholders’ equity.

- Market value can be far above or below book value because market prices reflect expectations, profitability, risk, and sentiment.

- Book value can be less informative for businesses with important intangible assets that are not fully reflected on the balance sheet.

- Book value does not prove intrinsic value, business quality, stock safety, or undervaluation.

What Book Value Means

Book value means the net amount of assets recorded after liabilities are deducted under accounting records. If a company reports assets of 500 million and liabilities of 300 million, its book value is 200 million before considering any separate adjustments or accounting classifications.

That simple result can be useful, but the interpretation is narrow. Book value answers the question “what accounting equity base is recorded?” It does not answer “what is the business worth?” or “is the stock attractively priced?”

Investor-use boundary: Book value is a balance-sheet input. It can support analysis of financial structure, capital intensity, and valuation context, but it should not be treated as a complete valuation model.

Book Value Formula

The basic book value formula is:

Book Value = Total Assets – Total Liabilities

Total assets include resources recorded on the balance sheet. Total liabilities include obligations the company owes. The difference is the residual accounting claim attributable to equity holders under the company’s accounting records.

Simple example: A company records 120 million in total assets and 75 million in total liabilities. Its book value is 45 million. That number describes recorded accounting equity, not the price investors would necessarily pay for the entire business.

Where Book Value Comes From on the Balance Sheet

For common company analysis, book value is usually tied to the equity section of the balance sheet. The related accounting concept is shareholders’ equity, which represents the residual interest after liabilities are deducted from assets.

The exact composition can include common stock, additional paid-in capital, retained earnings, treasury stock adjustments, accumulated other comprehensive income, and other equity-related line items. The investor question is not only the final number, but also what created it.

A book value built mainly from retained earnings may carry a different analytical meaning from one shaped by write-downs, buybacks, accounting adjustments, or accumulated losses. The same headline book value can therefore reflect very different balance-sheet histories.

Company Book Value vs Asset Carrying Value

Book value can describe a company’s net recorded equity, but it can also describe the carrying value of a specific asset. Those are related accounting ideas, but they are not the same analytical object.

| Use of book value | What it refers to | How investors should read it |

|---|---|---|

| Company book value | Total recorded assets minus total recorded liabilities | A measure of accounting equity for the whole company |

| Asset carrying value | The recorded value of a specific asset on the balance sheet | A historical accounting amount that may differ from current economic value |

This distinction matters because a company can own assets whose accounting values differ from their current economic values. Depreciation, amortization, impairment, accounting policy, and acquisition history can all affect the recorded number.

Book Value vs Market Value

Book value is accounting-based. Market value is price-based. A company’s market value reflects what investors are currently willing to pay for the equity, while book value reflects recorded assets and liabilities under accounting rules.

| Concept | What it reflects | Source | Main limitation |

|---|---|---|---|

| Book value | Recorded accounting equity | Balance sheet | Can miss economic value not captured well by accounting records |

| Market value | Current market pricing of the company’s equity | Share price and shares outstanding | Can move with expectations, sentiment, liquidity, and risk appetite |

A market value above book value does not automatically mean overvaluation. A market value below book value does not automatically mean undervaluation. The gap needs interpretation through profitability, asset quality, reinvestment prospects, balance-sheet risk, and the durability of future earnings.

Book Value Per Share and Tangible Book Value

Investors often convert company book value into a per-share number. Book value per share divides common equity by the relevant share count, making the accounting equity base easier to compare with a stock price.

Another related lens removes certain intangible assets from the equity base. Tangible book value can be more useful when the main question is how much recorded equity remains after goodwill and other intangible items are excluded.

Both related measures need context. Per-share book value can be affected by buybacks, issuance, losses, and accounting adjustments. Tangible book value can be useful for asset-heavy analysis, but it can understate businesses whose real value depends on brands, software, networks, data, or customer relationships.

When Book Value Can Mislead Investors

Book value can look precise because it comes from financial statements, but precision is not the same as economic completeness. Accounting values can lag current business reality, especially when the most important assets are intangible, internally developed, or difficult to measure on the balance sheet.

Main limitation: Book value is shaped by accounting treatment. Historical cost, depreciation, amortization, impairment charges, goodwill, and intangible asset recognition can make recorded equity very different from economic value.

The risk is greatest when book value is treated as a shortcut. A low price relative to book value may reflect asset risk, weak profitability, poor capital allocation, expected losses, or a business model that cannot earn adequate returns on its recorded equity. A high price relative to book value may reflect valuable earning power that accounting book value does not fully capture.

Common mistake: Treating book value as proof of cheapness turns an accounting number into a valuation conclusion. The better use is narrower: start with the recorded equity base, then test asset quality, profitability, leverage, cash generation, and business durability.

How Investors Can Use Book Value Carefully

Book value is most useful when it stays connected to its source. The number should lead back to the balance sheet, the assets that support it, the liabilities that reduce it, and the accounting choices that shaped it.

Asset-heavy companies, financial companies, and balance-sheet-sensitive businesses may give book value more analytical weight than businesses where brand strength, software, intellectual property, network effects, or customer relationships dominate economic value. Even then, book value is only one input.

A careful reading separates three questions. First, what equity base is recorded? Second, how reliable and economically relevant are the recorded assets and liabilities? Third, what return can the company earn on that equity base over time?

That sequence keeps the interpretation grounded. Book value can clarify the starting accounting base, while profitability, cash flow, capital allocation, and competitive position explain whether that base is likely to create durable value.

FAQ

What is book value in simple terms?

Book value is the accounting value left after a company subtracts total liabilities from total assets. For a company, it usually corresponds to shareholders’ equity on the balance sheet.

Is book value the same as market value?

No. Book value comes from accounting records, while market value comes from the stock market’s current pricing of the company’s equity.

Does a stock trading below book value mean it is undervalued?

No. A stock trading below book value may reflect asset risk, weak profitability, expected losses, poor capital allocation, or other problems. Book value can support valuation context, but it does not prove undervaluation by itself.

Why can book value be less useful for intangible-heavy companies?

Many intangible sources of value, such as internally developed software, brand strength, data, or customer relationships, may not be fully reflected in book value.