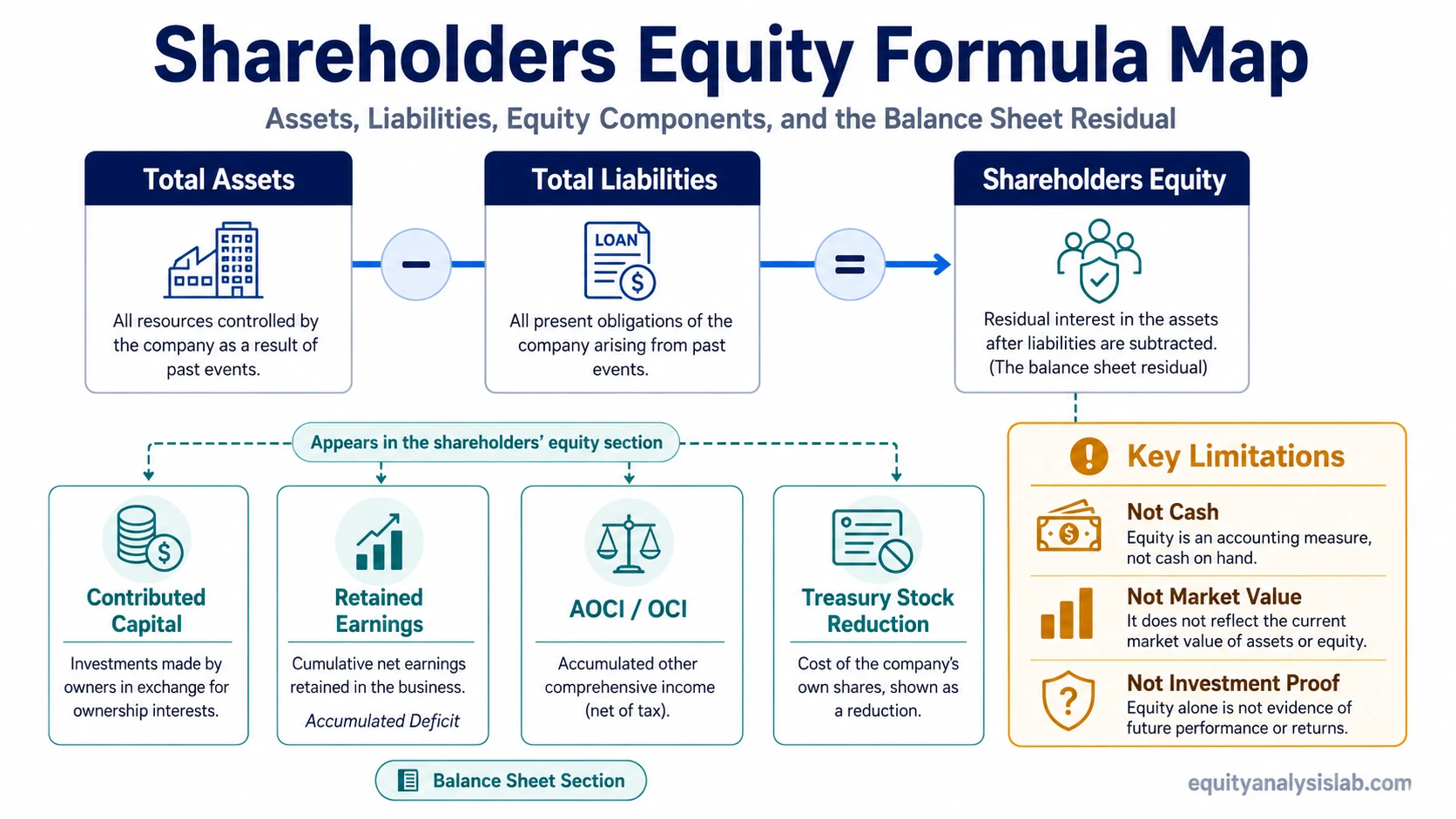

Shareholders equity is the residual accounting interest in a company after total liabilities are subtracted from total assets. It appears in the shareholders’ equity section of the balance sheet and can help investors read book value, capital structure, retained capital, and return-on-equity context, but it is not cash, market value, or proof of investment quality by itself.

Definition: Shareholders equity, also called stockholders equity in many financial statements, represents the accounting claim left for common and preferred shareholders after a company’s liabilities are deducted from its assets.

The number is a balance-sheet measure, not a market-price measure. A company can report positive shareholders equity while still facing weak profitability, high leverage, or poor future returns. A company can also report low or negative shareholders equity for reasons that require context, such as accumulated losses, large buybacks, accounting write-downs, or industry-specific balance-sheet structures.

Key Points

- Shareholders equity equals total assets minus total liabilities.

- It appears in the shareholders’ equity section of the balance sheet.

- Common components include share capital, additional paid-in capital, retained earnings, accumulated other comprehensive income or loss, and treasury stock.

- It is an accounting residual, not the company’s cash balance or stock-market value.

- Investors can use it as one input for book value, leverage context, ROE analysis, and retained-capital interpretation.

What Is Shareholders Equity?

Shareholders equity is the portion of the balance sheet that remains after liabilities are deducted from assets. In accounting terms, it is the residual interest attributable to the company’s shareholders rather than to creditors.

The basic relationship comes from the accounting equation: assets are financed either by liabilities or by equity. If liabilities are the creditor-financed part of the balance sheet, shareholders equity is the accounting residual that belongs to the shareholder side of the capital structure.

This does not mean shareholders can withdraw that amount as cash. Assets may include inventory, property, receivables, investments, intangibles, deferred tax assets, or other non-cash items. Shareholders equity is therefore a book accounting measure, not a liquidity measure.

Shareholders Equity Formula

Formula: Shareholders Equity = Total Assets – Total Liabilities

If a company reports $500 million in total assets and $320 million in total liabilities, shareholders equity is $180 million. That $180 million is the accounting residual on the balance sheet. It does not mean the company holds $180 million in cash, and it does not mean the stock market should value the company at $180 million.

| Formula View | Component View | Investor-Use Boundary |

|---|---|---|

| Total assets minus total liabilities | Capital accounts, retained earnings, AOCI or OCI where relevant, and treasury stock reductions | Useful for book-value and balance-sheet analysis, but not a standalone valuation or quality signal |

Where Shareholders Equity Appears on the Balance Sheet

Shareholders equity appears below liabilities in the balance sheet’s equity section. The exact label may appear as shareholders’ equity, stockholders’ equity, total equity, total shareholders’ equity, or a similar phrase depending on the company and reporting format.

The balance sheet shows the equity balance at a point in time. It does not, by itself, explain every change that occurred during the period. New share issuance, retained profit, losses, dividends, buybacks, currency translation adjustments, and other comprehensive income items can all change the equity section between reporting dates.

For investors, the placement matters because shareholders equity connects the asset base, the liability structure, and the accounting claim left for shareholders in one section of the financial statements.

Main Components of Shareholders Equity

The components of shareholders equity vary by company, but several recurring line items appear frequently in public financial statements.

| Component | What It Represents | How It Affects Equity |

|---|---|---|

| Common stock or share capital | Capital recorded from issued common shares | Usually increases recorded equity when shares are issued |

| Additional paid-in capital | Capital paid above par or stated value | Usually increases contributed capital within equity |

| Retained earnings or accumulated deficit | Cumulative profits kept in the business, reduced by losses and distributions | Can increase equity when profits are retained, or reduce equity when losses accumulate |

| Accumulated other comprehensive income or loss | Selected gains and losses recorded outside net income under accounting rules | Can increase or reduce equity depending on the item |

| Treasury stock | Shares repurchased and held by the company rather than retired | Usually reduces shareholders equity while held as treasury stock |

One important component is retained capital. When profits are kept in the business rather than distributed to shareholders, they flow into profits kept in the business rather than distributed to shareholders within the equity section. Losses and dividends reduce the cumulative retained balance.

Positive and Negative Shareholders Equity

Positive shareholders equity means recorded assets exceed recorded liabilities. That can indicate that the company has a positive accounting net asset base, but it does not automatically prove that the company is financially strong, undervalued, or high quality.

Negative shareholders equity means recorded liabilities exceed recorded assets. It can appear after sustained losses, large distributions, large buybacks, asset write-downs, or capital-structure decisions. The meaning depends on why the balance became negative: operating losses, asset write-downs, large repurchases, distributions, and leveraged capital structures do not all carry the same interpretation.

Negative equity boundary: An accumulated deficit is a negative retained-earnings balance. It can reduce shareholders equity, but total shareholders equity also includes other capital accounts and comprehensive-income items.

Because of that, negative shareholders equity should be analyzed through the cause, trend, business model, financing access, and asset base rather than treated as an automatic conclusion.

What Shareholders Equity Can Tell Investors

Shareholders equity can help investors understand the accounting base behind several balance-sheet and performance measures. It is most useful when combined with profitability, cash flow, leverage, dilution, asset quality, and valuation context.

- Book value context: Shareholders equity is a starting point for book-value analysis. book value per share translates equity into a per-share denominator.

- Capital structure context: Comparing liabilities and equity helps show how much of the asset base is financed by creditors versus shareholders.

- ROE context: Return on equity uses equity as a denominator, so changes in equity can affect the ratio even when net income changes less dramatically.

- Retained-capital context: Growth in retained equity can show that profits are being kept in the business, but the quality of those profits still needs separate analysis.

- Trend context: Changes in equity over time can reveal dilution, buybacks, losses, dividends, comprehensive-income changes, or balance-sheet restructuring.

What Shareholders Equity Cannot Prove

Shareholders equity is useful, but it is often misread when treated as a complete investment conclusion.

Limit: Shareholders equity does not prove that a stock is cheap, safe, high quality, or likely to produce future returns. It is one accounting input inside a broader analysis.

- It is not the company’s cash balance.

- It is not the company’s market capitalization.

- It does not prove that assets are worth their carrying value in the market.

- It does not prove that management has allocated capital well.

- It does not prove that a company has strong earnings quality.

- It does not create a buy signal, sell signal, or valuation conclusion by itself.

For example, a company can have high shareholders equity because it owns large recorded assets, but those assets may produce weak returns. Another company can have low or negative equity because of accumulated buybacks, accounting structure, or past losses. Used alone, it is too broad to support an investment conclusion.

Shareholders Equity vs Related Concepts

Several nearby concepts overlap with shareholders equity, but they answer different questions. Keeping those boundaries clear prevents the equity section from being treated as a catch-all explanation for every book-value or capital-account topic.

| Concept | Main Question It Answers | Boundary Against Shareholders Equity |

|---|---|---|

| Retained earnings | How much cumulative profit has been kept in the business after losses and distributions? | Retained earnings are one component of equity, not the full shareholders equity section. |

| Accumulated deficit | Has the retained-earnings balance turned negative? | An accumulated deficit can reduce equity, but total equity also includes other capital and comprehensive-income items. |

| Book value per share | How much book equity is associated with each share? | It translates equity into a per-share denominator rather than defining the whole equity section. |

| Statement of shareholders’ equity | What changed in equity during the period? | It explains movement over time, while the balance sheet shows the period-end equity balance. |

| Market capitalization | What value does the stock market assign to the company’s equity? | It is price-based, not the same as recorded book equity. |

The balance sheet shows the ending equity balance, while changes in the equity section from one period to another are explained through a separate movement schedule.

FAQ

Is shareholders equity an asset?

No. Shareholders equity is not an asset. It is the residual accounting interest after total liabilities are subtracted from total assets.

Is shareholders equity the same as book value?

Shareholders equity is closely related to book value because it represents the recorded equity base of the company. Book value per share takes that equity concept and divides it by a share-count denominator.

What does negative shareholders equity mean?

Negative shareholders equity means recorded liabilities exceed recorded assets. It can reflect accumulated losses, write-downs, buybacks, distributions, or capital-structure choices, so the cause matters more than the sign alone.

How is shareholders equity calculated?

Shareholders equity is calculated by subtracting total liabilities from total assets. The formula is: Shareholders Equity = Total Assets – Total Liabilities.

Does high shareholders equity mean a company is a better investment?

No. A higher shareholders equity balance does not automatically mean a better investment. The number needs to be interpreted with profitability, cash flow, leverage, asset quality, dilution, and valuation context.