Shareholders’ equity mechanics explains how a company’s book equity is formed, adjusted, reported, and interpreted. The core equation is shareholders’ equity = total assets − total liabilities. That number is only the starting point: investors also need to understand whether equity changed because of retained earnings, paid-in capital, treasury stock, accumulated deficit, AOCI, or another equity component.

The useful distinction is simple. Shareholders’ equity is the balance-sheet equity number at one point in time. The statement of shareholders’ equity explains how that number moved during a period. Retained earnings, book value per share, and tangible book value answer narrower questions about profit retention, per-share book equity, and adjusted book equity.

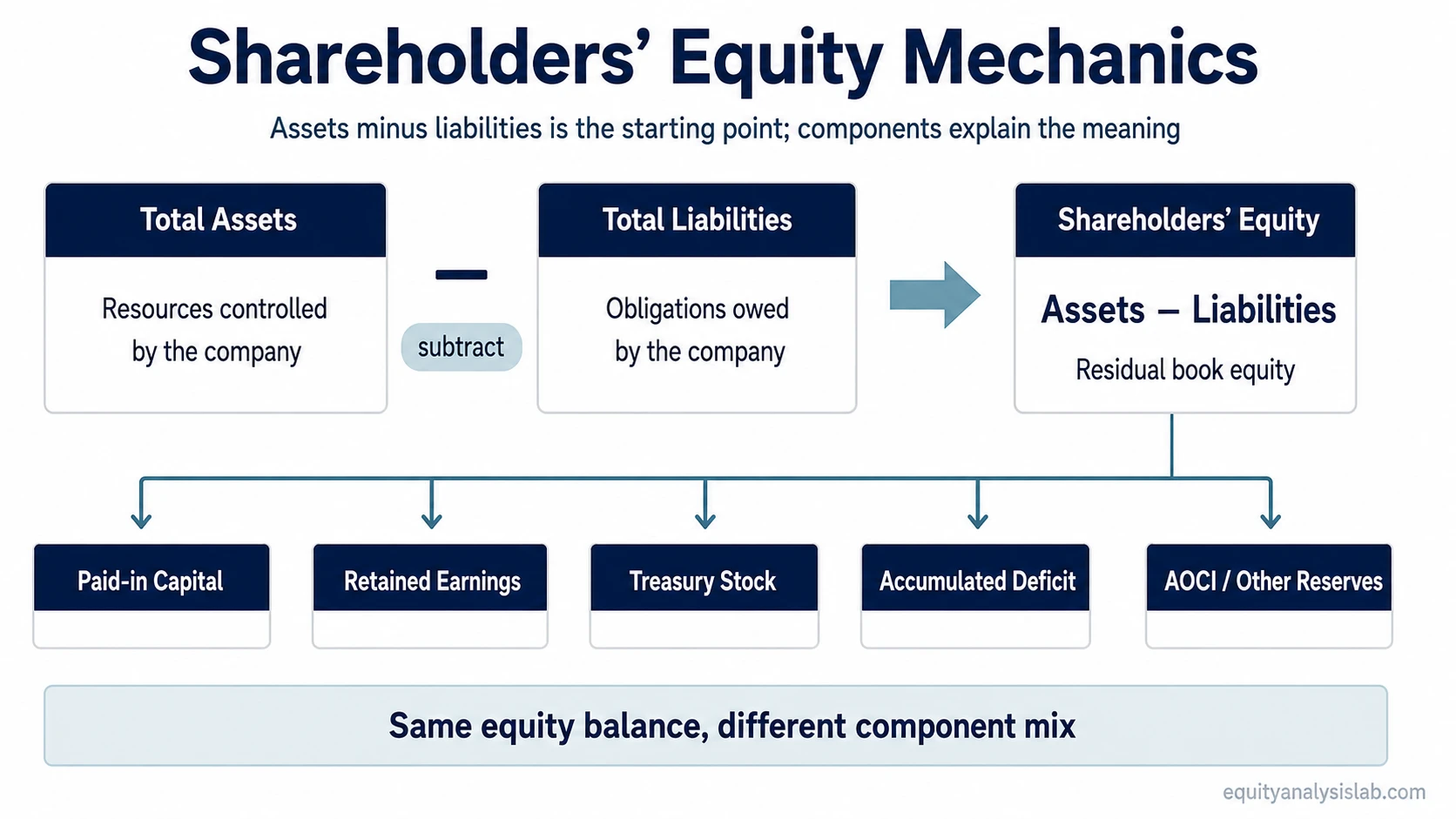

The core equation behind shareholders’ equity

Shareholders’ Equity = Total Assets − Total Liabilities

Shareholders’ equity is the residual book claim left after a company’s liabilities are subtracted from its assets. If assets increase without a matching increase in liabilities, book equity can rise. If liabilities grow faster than assets, book equity can fall. The equation explains the balance-sheet position, not the market price of the company.

For investors, the equation is most useful when it is connected to the components behind the number. A higher equity balance can come from retained profits, new capital issued to shareholders, changes in accumulated other comprehensive income, or reductions in treasury stock. A lower balance can come from losses, buybacks recorded as treasury stock, dividends, write-downs, or accumulated deficits.

How the main shareholders’ equity components fit together

| Equity component | What it usually represents | Investor interpretation |

|---|---|---|

| Common stock and paid-in capital | Capital contributed by shareholders above or around the legal share value. | Shows part of the owner-capital base, but does not by itself measure business quality. |

| Retained earnings | Accumulated profits kept in the business after dividends and prior-period adjustments. | Helps separate internally generated book value from capital raised externally. |

| Treasury stock | Shares repurchased and held by the company, usually shown as a reduction to equity. | Can reduce total book equity even when the operating business remains profitable. |

| Accumulated deficit | A negative retained earnings balance after cumulative losses or distributions exceed accumulated profits. | Signals that the retained-earnings history needs context before drawing conclusions about balance-sheet strength. |

| AOCI and other reserves | Items such as unrealized gains or losses, currency translation effects, or pension-related adjustments where applicable. | Can move book equity without flowing through ordinary net income in the same way as operating profit. |

Which shareholders’ equity concept answers the investor question?

| Investor question | Concept to use | Best next step | Why it matters |

|---|---|---|---|

| What is the company’s book equity after liabilities? | Shareholders’ equity | shareholders’ equity | Starts with the balance-sheet residual claim: assets minus liabilities. |

| How did equity change during the period? | Statement movement | statement of shareholders’ equity | Separates beginning equity, period changes, and ending equity. |

| How much profit has been kept inside the business? | Retained earnings | retained earnings | Shows accumulated profit retention after dividends and adjustments. |

| Where does retained earnings appear in the accounts? | Balance-sheet placement | retained earnings on the balance sheet | Connects the retained-earnings balance to the equity section rather than treating it as cash. |

| How much book equity exists per common share? | Per-share book equity | book value per share | Converts total book equity into a per-share denominator for comparison work. |

| What remains after excluding intangible assets? | Adjusted book equity | tangible book value | Focuses on book equity after removing goodwill and other intangible assets where relevant. |

| Why is retained earnings negative? | Negative retained-earnings history | accumulated deficit | Helps explain negative retained earnings without assuming the company is automatically unsafe or uninvestable. |

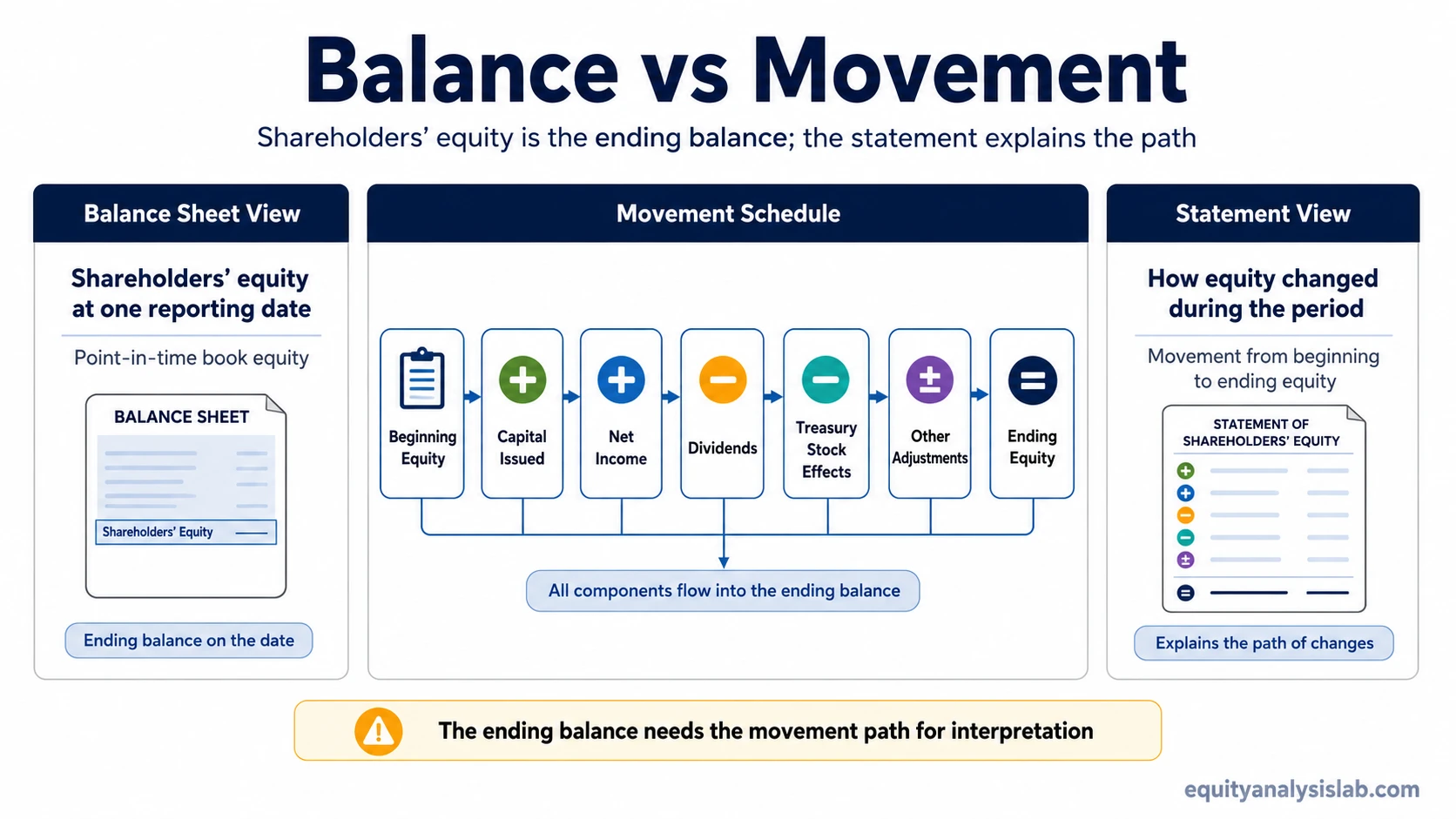

Balance-sheet stock vs statement movement

Shareholders’ equity on the balance sheet is a stock measure. It shows the equity balance at a reporting date. The statement of shareholders’ equity is a movement schedule. It connects beginning equity to ending equity by showing the period’s changes.

Simple movement logic:

Beginning shareholders’ equity + capital issued + net income − dividends − treasury stock effects ± other equity adjustments = ending shareholders’ equity.

This movement view prevents a common misread. A company can report higher total equity without the increase coming only from operating performance. New paid-in capital, AOCI changes, treasury stock movement, and other adjustments can all affect the equity section.

Short example: why the source of the change matters

Assume a company reports a higher ending equity balance than last year. The better question is where the increase came from. A rise driven mainly by retained profits means something different from a rise driven mainly by new share issuance or an accounting adjustment. A decline caused by treasury stock can also mean something different from a decline caused by operating losses.

The same ending number can carry different meaning depending on the path. Shareholders’ equity mechanics separates the balance from the movement behind the balance.

What shareholders’ equity mechanics does not decide by itself

Shareholders’ equity is not a standalone proof of business quality, balance-sheet safety, or future return potential. It is an accounting measure that needs context from profitability, cash flow, debt, asset quality, dilution, and valuation.

- Book equity is not market value. The market can price a company above or below book equity depending on expected returns, asset quality, growth, risk, and investor expectations. The specific distinction belongs in book value vs market value.

- Higher equity is not automatically better. A larger equity base may reflect retained profits, new capital issuance, asset revaluations, or accounting adjustments.

- Negative equity is not automatically fatal. It can be serious, but the cause matters: cumulative losses, distributions, buybacks, write-downs, or capital structure can produce different interpretations.

- Retained earnings are not cash. Retained earnings track accumulated profit retention, while cash depends on working capital, capital spending, financing flows, and other balance-sheet movements. The related comparison is retained earnings vs net income.

- Treasury stock is not automatically bullish. Buybacks reduce equity through treasury stock accounting, but the investment interpretation depends on price paid, business quality, capital needs, and alternative uses of cash.

Shareholders’ equity mechanics FAQ

Is shareholders’ equity the same as market value?

No. Shareholders’ equity is a book accounting measure based on assets minus liabilities. Market value reflects the price investors assign to the company’s equity in the market.

Is retained earnings the same as cash?

No. Retained earnings are accumulated profits kept in the business after dividends and adjustments. Cash is a separate balance-sheet asset. Retained earnings build from profit history rather than from cash balance alone.