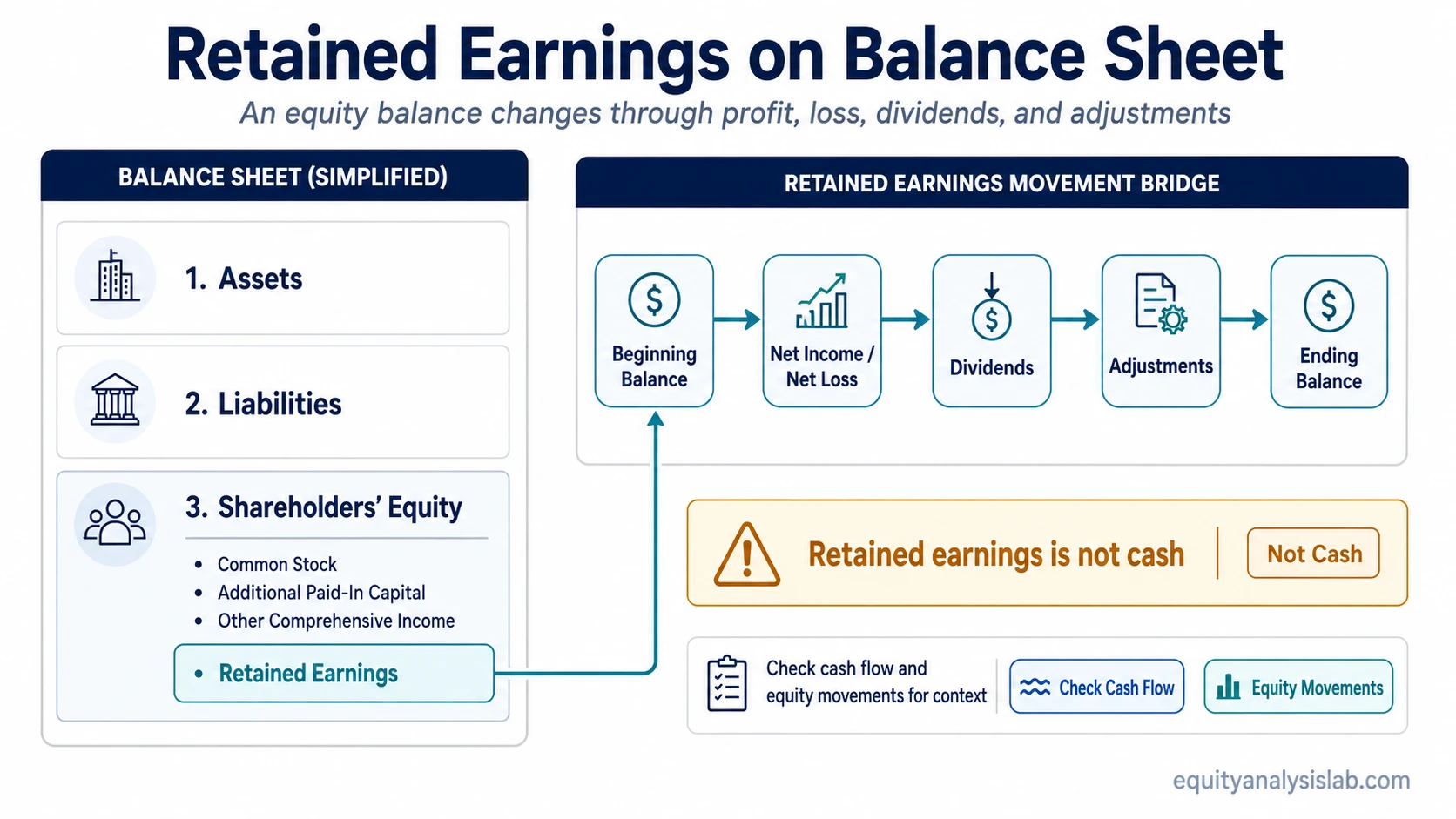

Retained earnings appears in the shareholders’ equity section of the balance sheet. It is the accumulated earnings kept in the business after losses, dividends, and certain adjustments, but it is not the same as cash.

Definition: Retained earnings on the balance sheet is the ending retained earnings balance reported inside equity, after the company’s prior retained earnings have been adjusted for current-period profit or loss, dividends, and applicable accounting adjustments.

The broader retained earnings concept explains how profits accumulate over time. The balance-sheet view is narrower: it shows where the ending amount sits in the financial statements and why the number needs context before it can support an investor interpretation.

Retained earnings is an equity component, not an asset. A company can report a large retained earnings balance while having limited cash on hand, weak recent cash conversion, or large non-cash accounting items affecting reported profit.

Key Points

- Retained earnings appears under shareholders’ equity, not under assets or liabilities.

- The balance usually changes through net income, net losses, dividends, and certain accounting adjustments.

- Retained earnings is not a cash reserve and does not prove reinvestment quality by itself.

- Cash flow, dividend policy, buybacks, treasury stock, and equity movements help explain what the balance means.

Where Retained Earnings Appears on the Balance Sheet

Retained earnings is normally listed within shareholders’ equity, alongside other equity accounts such as common stock, additional paid-in capital, accumulated other comprehensive income, and treasury stock where applicable.

The line does not show cash held in a bank account. It shows the cumulative portion of accounting earnings that has remained in equity rather than being distributed as dividends, reduced by losses, or changed by relevant adjustments.

| Balance sheet area | Line item | What it means | What it does not mean |

|---|---|---|---|

| Shareholders’ equity | Retained earnings | Cumulative earnings kept in the business after dividends, losses, and applicable adjustments | Cash available for spending, reinvestment, or distribution |

| Assets | Cash and cash equivalents | Cash-like resources held at the reporting date | The accumulated profit history of the company |

| Shareholders’ equity | Treasury stock, if reported | Shares repurchased and held by the company, often reducing total equity presentation | A direct retained earnings calculation in a simple reading |

What the Retained Earnings Balance Represents

The retained earnings balance is a movement bridge. It starts with the prior retained earnings balance, then changes as the company reports profit or loss, pays dividends, and records certain adjustments.

| Movement item | Typical effect on retained earnings | Interpretation note |

|---|---|---|

| Beginning retained earnings | Starting point for the period | Reflects cumulative prior-period earnings retained in equity |

| Net income | Usually increases retained earnings | Reported profit adds to equity if it is not distributed |

| Net loss | Usually reduces retained earnings | Losses absorb prior retained earnings and may create or deepen an accumulated deficit |

| Dividends | Reduce retained earnings | Distributions transfer value out of retained earnings rather than proving weak performance |

| Prior-period or accounting adjustments | Can increase or reduce retained earnings | The effect depends on the adjustment and presentation in the filing |

A simple movement formula is: beginning retained earnings plus net income, minus net losses and dividends, plus or minus relevant adjustments. The exact presentation can vary by company and reporting framework, so the statement of shareholders’ equity or retained earnings schedule matters when the movement is material.

What Changes Retained Earnings

Profits usually raise retained earnings, while losses and dividends reduce it. That pattern makes the balance useful, but it should not be read as a clean scorecard for business quality.

Dividend policy can make a profitable company’s retained earnings grow slowly because more earnings are distributed. A company that retains more profit may show a larger balance, but that does not confirm that the retained capital was reinvested well.

Buybacks require careful reading. Repurchased shares often affect equity presentation through treasury stock or related equity accounts, so buybacks should not be treated as a simple retained earnings movement without checking the statement of shareholders’ equity.

Reading note: Retained earnings is best read as an accounting equity balance. Cash flow, capital allocation, and equity movement schedules explain whether the balance reflects durable earning power, distributions, accounting adjustments, or a mix of several forces.

What Retained Earnings Can and Cannot Tell Investors

The retained earnings line can help frame a company’s profit retention history, but the same balance can support different interpretations depending on cash conversion, payout policy, buybacks, and recent profitability.

| Balance-sheet signal | What it can indicate | What it cannot prove | Cross-check |

|---|---|---|---|

| Positive retained earnings | The company has accumulated profits after losses and distributions over time | Does not show that current cash is high or that reinvestment has been successful | Operating cash flow, free cash flow, and capital allocation history |

| Negative retained earnings / accumulated deficit | Losses, distributions, or adjustments have exceeded accumulated retained profits | Should not be read as an automatic verdict on future viability | Recent profitability, operating cash flow, liquidity, and balance-sheet strength |

| Rising retained earnings | Profits are being retained after dividends and adjustments | Does not confirm that retained capital is earning attractive returns | Return on equity, return on invested capital, cash conversion, and growth quality |

| Falling retained earnings | Losses, dividends, or adjustments are reducing the balance | Needs context before being treated as negative for shareholders | Dividend policy, one-time items, and statement of shareholders’ equity movements |

| High retained earnings with weak cash flow | Reported earnings may not be converting cleanly into cash | Should not be treated as evidence that accounting profit equals economic cash generation | Operating cash flow, receivables, working capital, and accrual quality |

| Retained earnings with large dividends or buybacks | Capital returns may be materially changing equity composition | Needs support from payout, repurchase, and share-count evidence | Dividend payout, treasury stock, share count, and book value per share |

Common Mistakes When Reading Retained Earnings

| Mistake | Safer interpretation |

|---|---|

| Treating retained earnings as cash | Retained earnings can be tied up in inventory, receivables, fixed assets, acquisitions, debt reduction, or past losses that were later recovered. Cash and retained earnings can move in very different ways. |

| Treating high retained earnings as automatic business quality | A high balance can come from years of profits, but quality depends on what the company did with those retained earnings and whether cash flow supports the accounting profit. |

| Treating negative retained earnings as a complete verdict | An accumulated deficit is a warning flag, not a full diagnosis. The interpretation changes when losses are shrinking, cash generation is improving, or new capital has changed the equity base. |

Simple Retained Earnings on Balance Sheet Example

Company A and Company B both report retained earnings of $500 million. Company A has consistent operating cash flow, modest dividends, and limited accounting adjustments. Company B has the same retained earnings balance, but recent profit depends heavily on accruals, working-capital swings, and large adjustments.

The balance is identical, but the interpretation is not. Company A’s retained earnings is more closely supported by cash generation, while Company B requires closer review of earnings quality and statement-of-equity movements.

The same logic applies when retained earnings is negative. A deficit caused by years of operating losses differs from a deficit shaped by restructuring, distributions, or a recent business turnaround. The balance starts the analysis; the supporting statements explain the path.

How to Cross-Check Retained Earnings

Retained earnings becomes more useful when it is compared with other financial statement evidence. The strongest checks usually come from cash flow, equity movement, and capital allocation rather than the balance-sheet line alone.

- Operating cash flow: check whether reported earnings are converting into cash and whether gaps between net income and cash flow persist.

- Statement of shareholders’ equity: review the movement from beginning to ending equity accounts, including dividends, buybacks, stock compensation, AOCI, and adjustments.

- Dividend policy: compare retained earnings growth with payout ratio, dividend consistency, and dividend sustainability.

- Buybacks and treasury stock: check whether repurchases are changing equity presentation and share count.

- Per-share equity metrics: compare total equity changes with ownership-base changes through book value per share trends and share-count movement.

Limitation: Retained earnings is a useful balance-sheet anchor, but it is not a valuation verdict. A careful reading separates the accounting balance from cash generation, reinvestment quality, payout policy, and changes in the equity base.

FAQ

Where is retained earnings shown on the balance sheet?

Retained earnings is shown in the shareholders’ equity section of the balance sheet. It is an equity account, not an asset account.

Is retained earnings the same as cash?

No. Retained earnings is an accumulated accounting balance. Cash is reported separately as an asset and may be much higher or lower than retained earnings.

Can retained earnings be negative?

Yes. Negative retained earnings are often described as an accumulated deficit. The cause may include losses, distributions, or adjustments, so the surrounding financial statements matter.

Do dividends reduce retained earnings?

Yes. Dividends normally reduce retained earnings because they distribute part of the company’s accumulated earnings to shareholders.