Retained earnings are cumulative profits kept within the equity section of a company’s balance sheet after losses and dividends, but they are not the same as cash available to spend.

The account shows how past profits and losses have moved through book equity over time. For investors, the useful question is not whether retained earnings are simply high or low. The useful question is what those retained earnings represent: profits kept in the business, dividends not paid out, losses that reduced equity, or capital allocation choices that need more context.

Definition: Retained earnings are the cumulative net earnings a company has kept in equity instead of distributing to shareholders as dividends, adjusted for losses and other relevant equity movements.

Key Points

- Retained earnings are cumulative, not just the profit from one period.

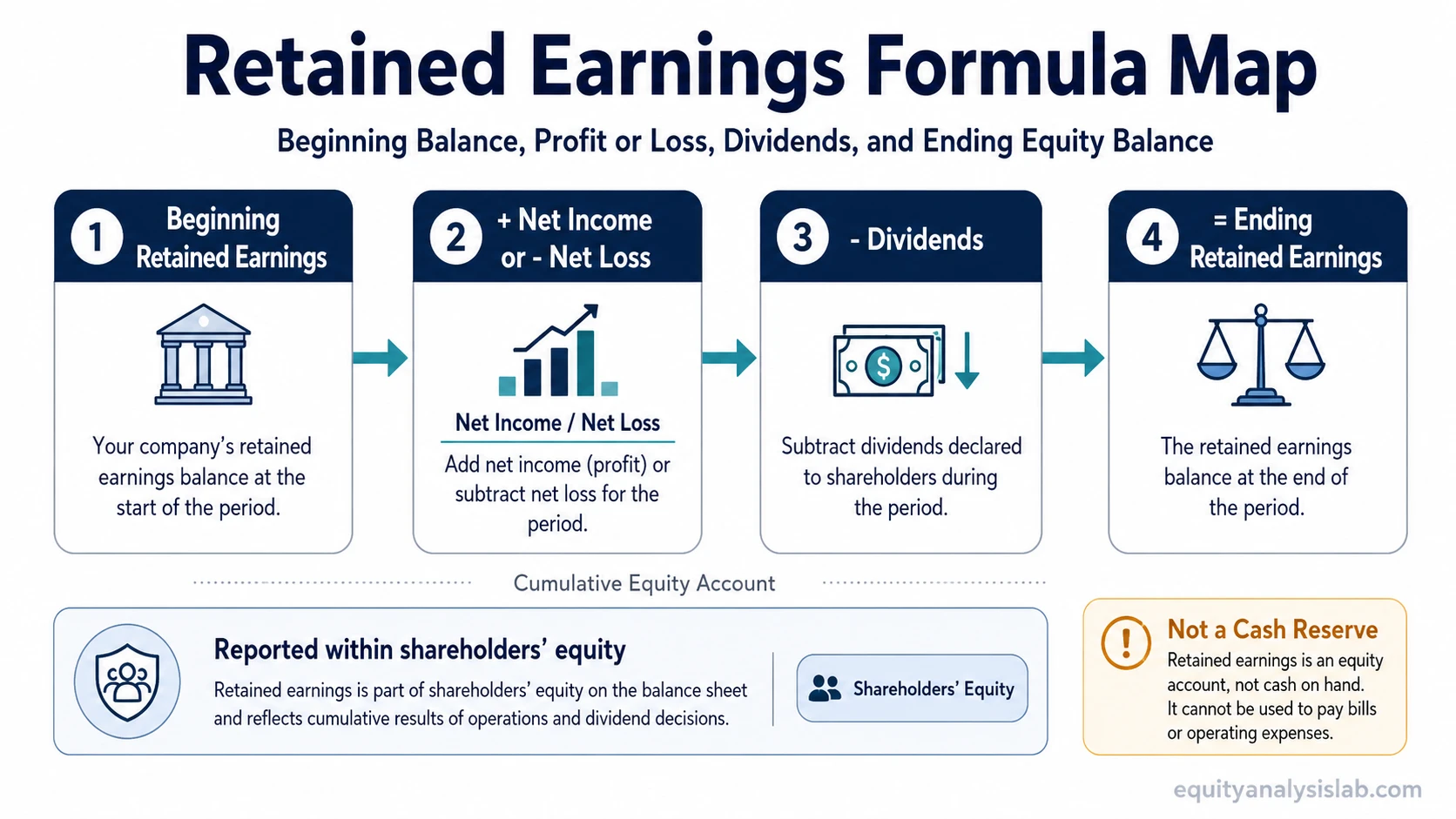

- The basic formula starts with beginning retained earnings, adds net income or subtracts net loss, and subtracts dividends.

- Retained earnings are reported inside the shareholders’ equity context, not as a cash account.

- Positive retained earnings do not prove that a company has available cash or strong reinvestment results.

- Negative retained earnings are commonly described as an accumulated deficit and need lifecycle, loss-history, and capital-structure context.

What Retained Earnings Means

Retained earnings represent the running total of earnings that remain in the company after accounting for losses and distributions to shareholders. The account accumulates across reporting periods, so it can reflect many years of profitability, losses, dividend policy, and equity adjustments.

That cumulative nature is the main distinction from current-period profit. Net income belongs to one reporting period. Retained earnings carry forward from prior periods and then change as new earnings, losses, and dividends are recorded.

Retained earnings are part of book equity. They help explain how profit has flowed into the equity base, but they do not show where the cash went. Earnings may have been used for working capital, acquisitions, capital expenditures, debt repayment, buybacks, or other corporate purposes.

Retained Earnings Formula

The standard retained earnings formula starts with the prior retained earnings balance, adds current-period net income or subtracts a net loss, and subtracts dividends distributed during the period.

| Formula component | What it represents |

|---|---|

| Beginning retained earnings | The retained earnings balance carried forward from the previous period. |

| Plus net income or minus net loss | The current-period profit or loss that changes the retained earnings account. |

| Minus dividends | Distributions to shareholders that reduce retained earnings when they are recorded in the period. |

| Ending retained earnings | The retained earnings balance after the period’s profit, loss, and dividend movements. |

Illustrative example: If a company starts with $100 million of retained earnings, earns $25 million of net income, and records $10 million of dividends, ending retained earnings would be $115 million. The example shows the accounting movement only; it does not prove that the company has $115 million of cash available.

Where Retained Earnings Appears in Financial Statements

Retained earnings usually appears within the equity section of the balance sheet. It may also be reconciled in a statement of retained earnings, a statement of changes in equity, or the statement where equity changes are shown.

The balance sheet shows the ending retained earnings balance at a point in time. The equity statement or retained earnings statement explains how the balance changed during the reporting period. That movement view is often more useful than the ending number alone because it separates beginning balance, net income or loss, dividends, and other equity movements.

Source-of-evidence note: Statement names vary by company and reporting format. When reviewing a filing, look for both the retained earnings line item and the reconciliation of equity changes rather than relying on one label only.

What Retained Earnings Can and Cannot Tell Investors

Retained earnings can help investors trace how much profit has been retained inside book equity over time. A company that regularly generates profit and pays modest dividends may build retained earnings. A company with repeated losses or large distributions may show a smaller balance or a negative balance.

The number still needs context. Retained earnings do not reveal whether retained capital was reinvested well, whether the company has strong cash conversion, or whether management made good capital allocation decisions. Those questions require cash flow, return metrics, debt levels, share count changes, and business model analysis.

Limitation: Retained earnings are an accounting equity balance, not a cash reserve, valuation conclusion, or stand-alone quality score. A high retained earnings balance can coexist with weak cash flow, and a low or negative balance can require more context before any investor interpretation is reasonable.

Retained Earnings vs Nearby Equity Concepts

Retained earnings sits close to several related accounting concepts, but each one answers a different question. The boundary matters because retained earnings can affect equity without becoming revenue, cash, dividends, or a per-share valuation metric by itself.

| Concept | Core distinction | Why the boundary matters |

|---|---|---|

| Revenue | Revenue is sales or operating income before expenses, not cumulative earnings kept in equity. | A company can grow revenue while retained earnings remain flat or negative if profits are weak or losses persist. |

| Net income | Net income is profit for one period. Retained earnings is a cumulative balance after prior periods and dividends. | Current profitability can improve before the retained earnings balance fully reflects a longer loss history. |

| Cash | Cash is a balance-sheet asset. Retained earnings is an equity account. | Retained earnings may have been reinvested or used elsewhere, so it should not be read as spendable cash. |

| Dividends | Dividends are distributions that can reduce retained earnings. | A company can report profits while retained earnings grow more slowly if dividends are large. |

| Accumulated deficit | An accumulated deficit is commonly used when retained earnings are negative. | The negative balance needs context around lifecycle stage, historical losses, recapitalizations, and future profitability. |

| Book value per share | The book value per share calculation uses common equity and share count context, not retained earnings alone. | Retained earnings can affect equity, but it does not independently determine per-share book value. |

Common Misunderstandings About Retained Earnings

Misunderstanding 1: Retained earnings are not the same as cash. The balance records cumulative earnings retained in equity, while cash depends on collections, spending, investment, financing, and working-capital movement.

Misunderstanding 2: Positive retained earnings are not automatically good. The company may have retained profits but used them inefficiently, diluted shareholders, or failed to convert accounting earnings into durable cash flow.

Misunderstanding 3: Negative retained earnings are not automatically bad in every case. The balance may reflect early-stage losses, restructuring history, large distributions, or long-term loss accumulation. The correct interpretation depends on the business model, capital structure, profitability path, and equity context.

Misunderstanding 4: Retained earnings should not be used as a stock screen by itself. It is one accounting account inside equity mechanics, not a complete valuation or investment decision framework.

FAQ

What is retained earnings?

Retained earnings are cumulative profits kept in a company’s equity after losses and dividends. They represent an accounting balance, not cash available to spend.

What is the retained earnings formula?

The basic formula is beginning retained earnings plus net income, or minus net loss, minus dividends. The result is ending retained earnings for the period.

Where is retained earnings shown on the balance sheet?

Retained earnings is usually shown inside shareholders’ equity. The period-by-period movement may appear in a statement of retained earnings, statement of changes in equity, or statement of shareholders’ equity.

Can retained earnings be negative?

Yes. Negative retained earnings are commonly described as an accumulated deficit. The meaning depends on the company’s loss history, lifecycle stage, distributions, and broader equity context.