A statement of shareholders’ equity is a financial statement schedule that reconciles beginning shareholders’ equity to ending shareholders’ equity over a reporting period.

It shows whether book equity changed because of profit or loss, dividends, share issuance, buybacks, accumulated other comprehensive income, or other equity movements.

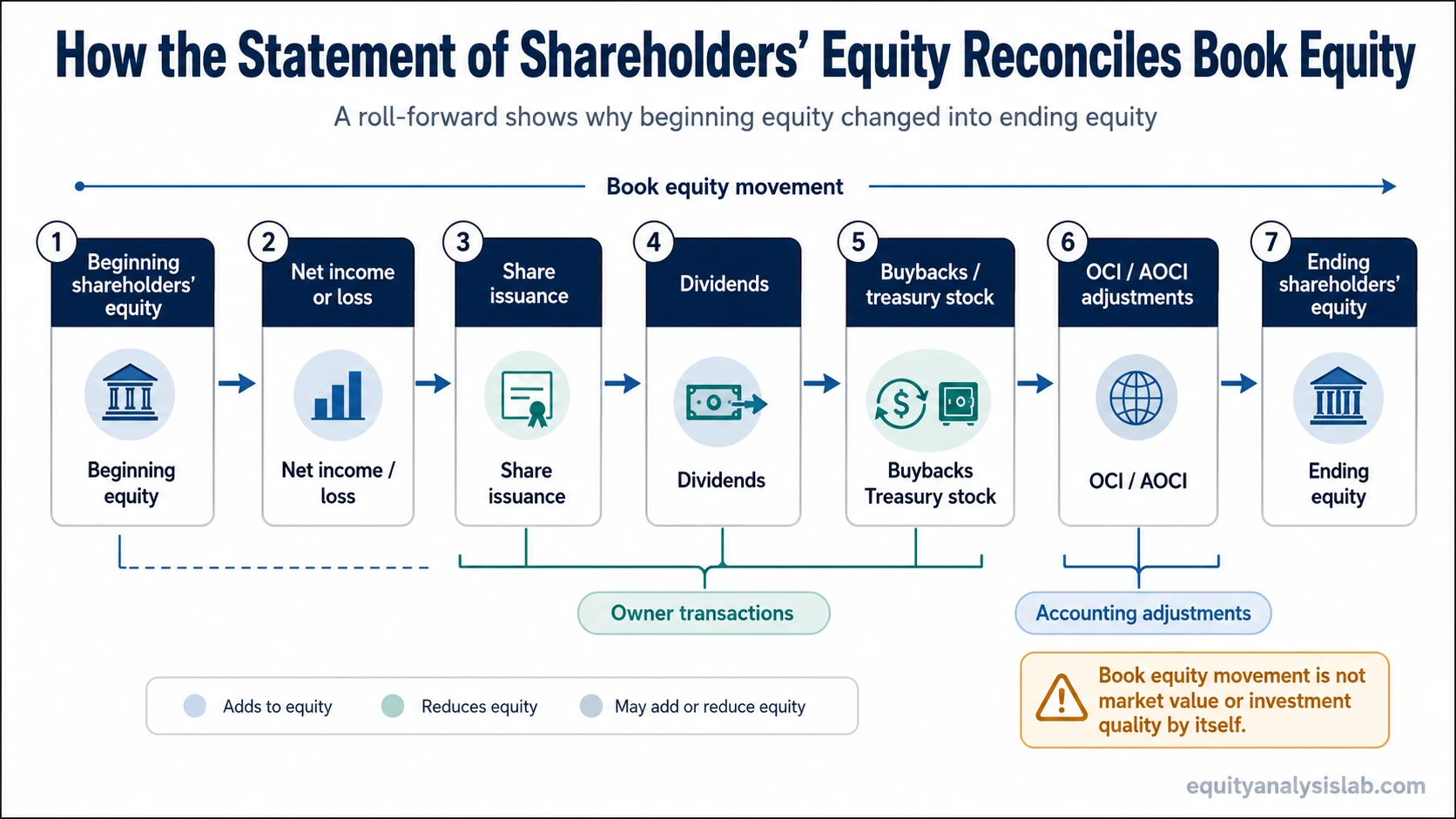

Definition: A statement of shareholders’ equity explains the movement in the equity section of the balance sheet. Shareholders’ equity is the ending balance at a point in time; the statement of shareholders’ equity shows how that balance changed during the period.

Key Points

- The statement reconciles beginning shareholders’ equity to ending shareholders’ equity.

- It separates earnings from owner transactions and accounting adjustments.

- Common line items include common stock, additional paid-in capital, retained earnings, dividends, treasury stock, and accumulated other comprehensive income.

- It explains book-equity movement, not market value, cash balance, or investment quality by itself.

What the Statement of Shareholders’ Equity Shows

The statement of shareholders’ equity shows why the equity section changed between two reporting dates. The starting point is beginning shareholders’ equity. The ending point is ending shareholders’ equity. The bridge between them is built from earnings, distributions, capital transactions, and accounting adjustments.

The same increase in equity can come from very different sources. Equity may rise because the company earned profit and retained it, because it issued shares, because accumulated other comprehensive income improved, or because several smaller changes moved in the same direction.

That source-of-change detail matters for interpretation. A higher ending equity balance can be more useful when it comes from retained earnings than when it comes mainly from new capital issuance, but the statement itself is still a reconciliation of book equity rather than a valuation conclusion.

How the Equity Roll-Forward Works

The basic roll-forward logic is:

Beginning shareholders’ equity + net income or loss + share issuance – dividends – share repurchases + or – other equity adjustments = ending shareholders’ equity.

This bridge is not a valuation model. Its value is in showing which forces moved book equity during the period and which of those forces deserve more analysis.

Simple statement of shareholders’ equity example: A company begins the year with $500 million of shareholders’ equity. It earns $80 million of net income, pays $20 million in dividends, repurchases $30 million of stock, and records a $10 million positive accumulated other comprehensive income adjustment. Ending shareholders’ equity would be $540 million: $500 million + $80 million – $20 million – $30 million + $10 million.

In that scenario, equity increased by $40 million, but the increase was not simply “net income.” Dividends, repurchases, and other comprehensive income also affected the final equity balance.

Main Line Items in a Statement of Shareholders’ Equity

The exact layout varies by company and reporting format, but the main line items usually explain contributed capital, cumulative retained profit, distributions, buybacks, and other equity adjustments.

| Line item | What it usually represents | How investors can read the movement |

|---|---|---|

| Common stock or preferred stock | Equity capital issued under the company’s share structure. | Increases can reflect new share issuance, equity financing, or conversion activity. |

| Additional paid-in capital | Capital paid by shareholders above stated or par value. | Large changes may point to issuance, stock-based compensation effects, or other capital transactions. |

| Retained earnings | Cumulative profit retained in the company after losses and dividends. | Growth can reflect profitable retention, while declines can reflect losses, dividends, or prior-period adjustments. |

| Net income or net loss | The current-period profit or loss that flows into retained earnings. | Profit-driven equity growth is different from equity growth caused mainly by new share issuance. |

| Dividends | Distributions paid to shareholders. | Dividends reduce retained earnings and can lower book equity even when the company reports profit. |

| Treasury stock or buybacks | Shares repurchased by the company and recorded as a reduction of equity. | Repurchases can reduce book equity while also changing per-share interpretation. |

| Accumulated other comprehensive income | Certain gains and losses recorded outside net income. | Changes can move equity without appearing as ordinary net income. |

How Investors Interpret Changes in Shareholders’ Equity

The strongest use of the statement is identifying the source of the movement. A company that grows equity through retained profits is different from a company that grows equity mainly by issuing new shares.

Profit-driven growth can suggest that earnings are being retained inside the company, but it still needs comparison with cash flow, return on equity, reinvestment opportunities, and capital allocation. A company can report net income while still having weak cash conversion or poor reinvestment results.

Issuance-driven growth can improve the balance sheet, but it may also dilute existing shareholders. Buybacks can reduce shareholders’ equity because treasury stock is recorded as a contra-equity item. That reduction does not automatically make the repurchase good or bad; the interpretation depends on price paid, business quality, balance-sheet strength, and the opportunity cost of the capital used.

Dividends reduce retained earnings because part of the company’s cumulative profit has been distributed rather than retained. A decline in retained earnings can therefore come from shareholder distributions, not only from business weakness.

Per-share interpretation becomes important when equity changes alongside share-count changes. Book value per share connects book equity to the number of shares, which can change the way investors read buybacks, issuance, and dilution.

What the Statement Does Not Prove

Limitation: The statement of shareholders’ equity explains book-equity movement. It does not prove market value, cash generation, solvency, future returns, or business quality by itself.

Book equity is an accounting measure, not the company’s market capitalization. A company can trade far above or below book equity depending on profitability, asset quality, growth expectations, risk, and investor demand.

Retained earnings are also not the same as cash. A company may have positive retained earnings while cash is tied up in inventory, receivables, acquisitions, debt repayment, or other uses. The retained earnings balance records cumulative accounting profit after distributions; it does not show where the cash sits today.

Negative retained earnings require context. A young company, cyclical company, turnaround, or heavily loss-making business may show a deficit for different reasons. When cumulative losses exceed retained profits, the condition is usually described as an accumulated deficit.

Rising shareholders’ equity is not automatically a quality signal. The movement becomes more useful when it is compared with the income statement, cash flow statement, capital allocation record, share-count changes, and returns generated on the equity base.

Statement of Shareholders’ Equity vs Shareholders’ Equity

The statement and the balance-sheet line are related, but they answer different questions. Shareholders’ equity is the balance at a specific date. The statement of shareholders’ equity explains the changes that produced that balance.

| Concept | Question answered | Investor use |

|---|---|---|

| Shareholders’ equity | What is the book equity balance at the reporting date? | Helps frame book value, leverage, and the residual accounting claim after liabilities. |

| Statement of shareholders’ equity | Why did book equity change during the reporting period? | Helps separate earnings, dividends, buybacks, issuance, and accounting adjustments. |

Related Concepts

Nearby equity concepts sharpen the interpretation without replacing the statement-level roll-forward.

| Related concept | How it connects |

|---|---|

| Shareholders’ equity | The balance-sheet equity figure is the ending point that the statement helps explain. |

| Retained earnings | This line captures cumulative profits retained in the business after losses and dividends. |

| Accumulated deficit | This condition appears when cumulative losses exceed retained profits. |

| Book value per share | This metric connects book equity to share count for per-share interpretation. |

FAQ

What is a statement of shareholders’ equity?

A statement of shareholders’ equity is a financial statement schedule that reconciles beginning shareholders’ equity to ending shareholders’ equity over a reporting period.

Is the statement of shareholders’ equity the same as the balance sheet?

No. The balance sheet shows shareholders’ equity at a point in time, while the statement of shareholders’ equity explains how that equity balance changed during the period.

Why can shareholders’ equity fall when a company is profitable?

Shareholders’ equity can fall despite profit if dividends, buybacks, negative other comprehensive income, or other equity adjustments are larger than the positive contribution from net income.

Does higher shareholders’ equity always mean a better investment?

No. Higher shareholders’ equity explains a larger book-equity balance, but investment quality also depends on profitability, cash flow, valuation, returns on capital, dilution, and business risk.