Tangible book value is the portion of book value tied to tangible assets after intangible assets such as goodwill are removed. It is based on balance-sheet accounting, not cash on hand, market value, or guaranteed liquidation proceeds.

Definition: Tangible book value, often shortened to TBV, adjusts book equity by excluding intangible assets so the remaining figure focuses on tangible balance-sheet support.

TBV becomes most informative when goodwill or acquired intangible assets make reported book equity look stronger than the tangible asset base alone.

The starting point is the company’s accounting balance sheet. In a broad residual ownership account after liabilities, intangible items can be part of reported equity even though they may not represent physical or easily separable asset value.

TBV separates tangible asset coverage from total accounting equity. The number still requires judgment because assets may be overstated, liabilities may be material, and market prices can differ sharply from accounting values.

Key Points

- Tangible book value removes goodwill and other intangible assets from book equity.

- The formula can be shown from total assets, liabilities, and intangible assets, or from shareholders’ equity and intangible assets.

- Goodwill is a common intangible asset excluded from the calculation.

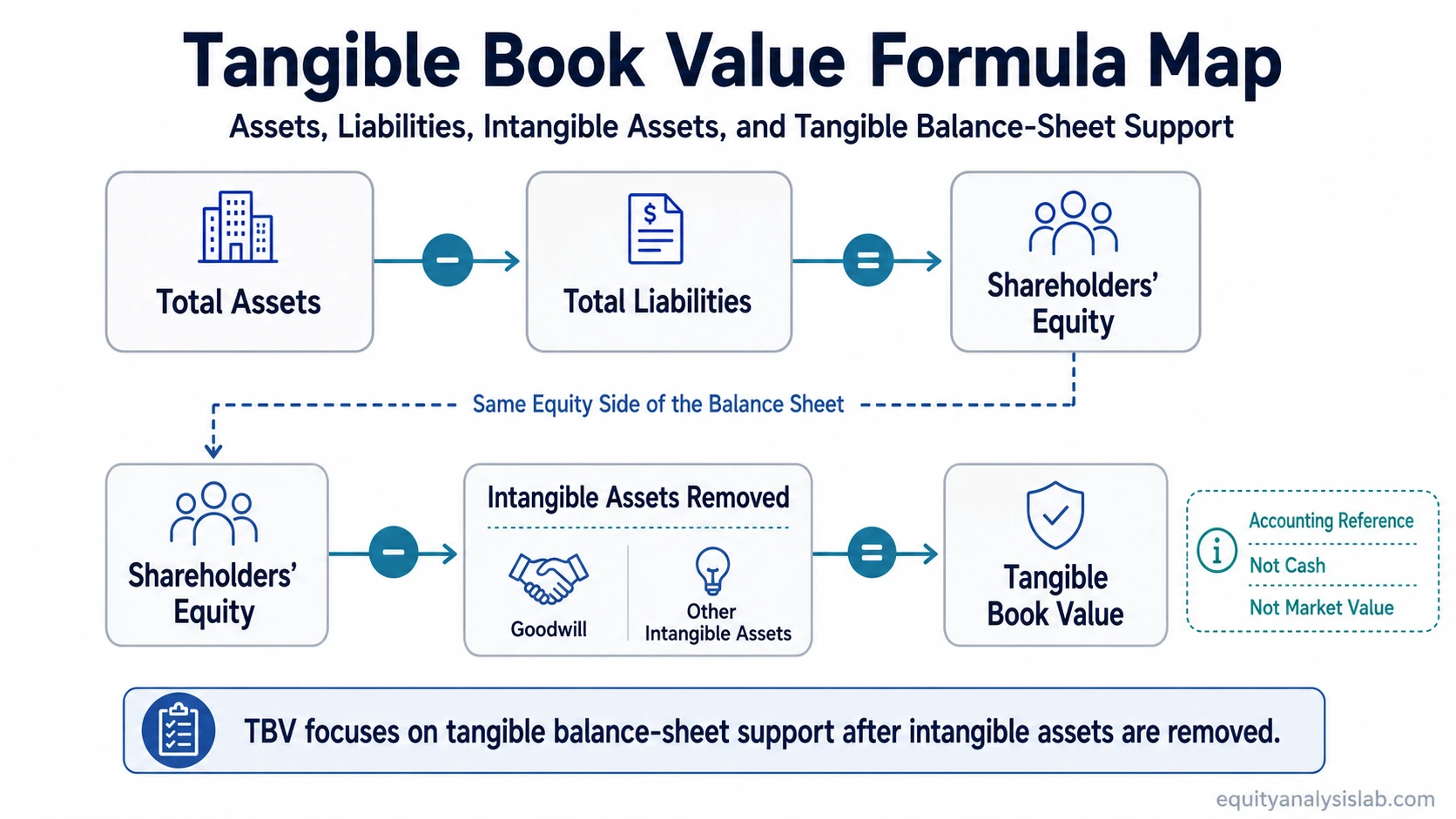

- TBV is not cash, market value, guaranteed liquidation value, or standalone investment proof.

- TBVPS, BVPS, and price-to-tangible-book are related metrics, but they answer different questions.

What Tangible Book Value Means

Tangible book value narrows total book value to the portion supported by tangible assets. Tangible assets include items such as cash, receivables, inventory, property, plant, equipment, and other physical or financial assets that remain after removing intangible assets.

Intangible assets include items such as goodwill, acquired customer relationships, trademarks, patents, and other non-physical assets recorded through accounting rules. Some intangible assets may have real economic value, but TBV excludes them to create a stricter tangible-asset view.

That stricter view is most useful when the balance sheet contains large goodwill or acquired-intangible balances. A company can report positive book equity while a large share of that equity depends on assets that are difficult to sell, value, or separate from the operating business.

Tangible Book Value Formula

The most direct formula is:

Tangible Book Value = Total Assets – Total Liabilities – Intangible Assets

The same calculation is often shown from the equity side of the balance sheet:

Tangible Book Value = Shareholders’ Equity – Intangible Assets

Both versions point to the same idea when the balance sheet is internally consistent. Total assets minus total liabilities equals shareholders’ equity, so subtracting intangible assets from either framing leaves the tangible portion of book equity.

The formula depends on how the source presents the balance sheet. Some data providers begin with shareholders’ equity, while others begin with total assets and liabilities. The consistency check is whether goodwill and other intangible assets are removed once, not ignored or double-counted.

Balance-Sheet Inputs Behind Tangible Book Value

The main advantage of TBV is observability. The inputs usually come from the balance sheet, but the interpretation depends on whether the reported numbers are clean, current, and economically meaningful.

| Input | Where it appears | Role in TBV | Interpretation note |

|---|---|---|---|

| Total assets | Balance sheet asset section | Starting asset base in the asset-side formula | Includes both tangible and intangible assets, so it is not the final tangible value. |

| Total liabilities | Balance sheet liability section | Subtracted before equity value belongs to common owners | Debt, leases, payables, and other obligations reduce residual equity. |

| Goodwill | Asset section, usually under intangible or non-current assets | Removed from book value | Goodwill often comes from acquisitions and may not be separately saleable. |

| Other intangible assets | Asset section, often near goodwill | Removed along with goodwill | Examples can include brands, patents, customer lists, and acquired technology. |

| Shareholders’ equity | Equity section | Alternative starting point for the equity-side formula | Represents accounting residual interest, not market capitalization. |

Equity components also shape the starting book value. A company with years of profits kept in the business may show a larger accumulated profit balance, while profits retained in equity can still be offset by write-downs, buybacks, dividends, or losses.

When losses accumulate enough to create negative retained earnings, an accumulated deficit can reduce or eliminate the equity base before tangible book value is even calculated.

Simple Tangible Book Value Example

A company reports $1,000 million in total assets, $600 million in total liabilities, and $150 million in goodwill and other intangible assets. Tangible book value would be calculated as:

Example calculation: $1,000 million total assets – $600 million liabilities – $150 million intangible assets = $250 million tangible book value.

The same result can be reached from shareholders’ equity. If total assets are $1,000 million and total liabilities are $600 million, shareholders’ equity is $400 million. Subtracting $150 million of intangible assets leaves $250 million of tangible book value.

The example only shows the accounting path. It does not judge whether the company is attractive, safe, or undervalued.

Tangible Book Value vs Related Concepts

Tangible book value is easy to confuse with nearby accounting and valuation metrics. The differences matter because each metric changes the unit of analysis.

| Concept | What it measures | How it differs from TBV |

|---|---|---|

| Book value | Total accounting equity after liabilities | Book value can include goodwill and other intangible assets. |

| Tangible book value | Book equity after intangible assets are removed | TBV focuses on tangible balance-sheet support. |

| Book value per share | Book value divided by shares outstanding | It converts equity into a per-share number, while TBV is the aggregate tangible equity amount. |

| Tangible book value per share | TBV divided by shares outstanding | It translates TBV into a per-share figure, but still depends on the same accounting inputs. |

| Price to tangible book | Market value compared with TBV | It is a valuation multiple, not the tangible book value number itself. |

A per-share version changes the question from total tangible equity to tangible equity per share. That distinction matters because book value per common share can move because of share issuance, repurchases, losses, or changes in equity, even when the underlying accounting concept is similar.

Price to tangible book adds the market price layer. A low price-to-tangible-book ratio does not automatically mean undervaluation, because the market may be discounting asset quality, earning power, leverage, business decline, or future losses.

What Tangible Book Value Can and Cannot Show

TBV can help frame tangible balance-sheet support. It can be useful when analyzing companies where physical assets, financial assets, or regulated balance-sheet strength are more central than brand value or acquired goodwill.

Limitation: Tangible book value is an accounting reference point. It is not cash, market value, intrinsic value, or guaranteed liquidation proceeds.

Asset quality can change the interpretation. Inventory may be marked above what it could recover, receivables may not be fully collected, and property values may differ from carrying value. A positive TBV number can still sit beside weak economics if the company’s tangible assets do not generate adequate returns.

Liability priority also matters. Creditors, lease obligations, preferred claims, legal obligations, and other senior claims can absorb value before common shareholders receive anything. TBV starts after liabilities in the formula, but the accounting figure does not simulate an actual liquidation process.

TBV is usually more relevant when tangible assets play a central role in the balance sheet. It is less complete when the business depends mainly on software, networks, brand, data, customer relationships, or human capital.

Common Mistakes With Tangible Book Value

| Mistake | Safer interpretation |

|---|---|

| Treating TBV as cash | Tangible assets can include receivables, inventory, equipment, property, and other assets that are not immediately available cash. |

| Treating TBV as guaranteed liquidation value | Accounting values do not guarantee sale prices, liquidation timing, transaction costs, or creditor outcomes. |

| Treating low price-to-tangible-book as automatic undervaluation | A low ratio can reflect real risk, weak profitability, poor asset quality, or expected balance-sheet deterioration. |

| Ignoring intangible asset economics | Removing goodwill and intangibles creates a stricter accounting view, but some intangible assets may still support real earning power. |

TBV works best as a starting boundary for balance-sheet review. It still needs to be checked against liabilities, asset quality, profitability, and the business model before it can support any broader interpretation.

FAQ

What is tangible book value?

Tangible book value is book equity after goodwill and other intangible assets are removed. It focuses on the tangible portion of a company’s accounting equity.

How do you calculate tangible book value?

Tangible book value can be calculated as total assets minus total liabilities minus intangible assets. It can also be calculated as shareholders’ equity minus intangible assets.

Is tangible book value the same as liquidation value?

No. Tangible book value is an accounting figure. Liquidation value depends on actual asset recoveries, liabilities, transaction costs, timing, and legal claim priority.

Does tangible book value prove that a stock is cheap?

No. TBV does not prove cheapness or investment attractiveness by itself. Asset quality, liabilities, profitability, business durability, and market expectations still matter.