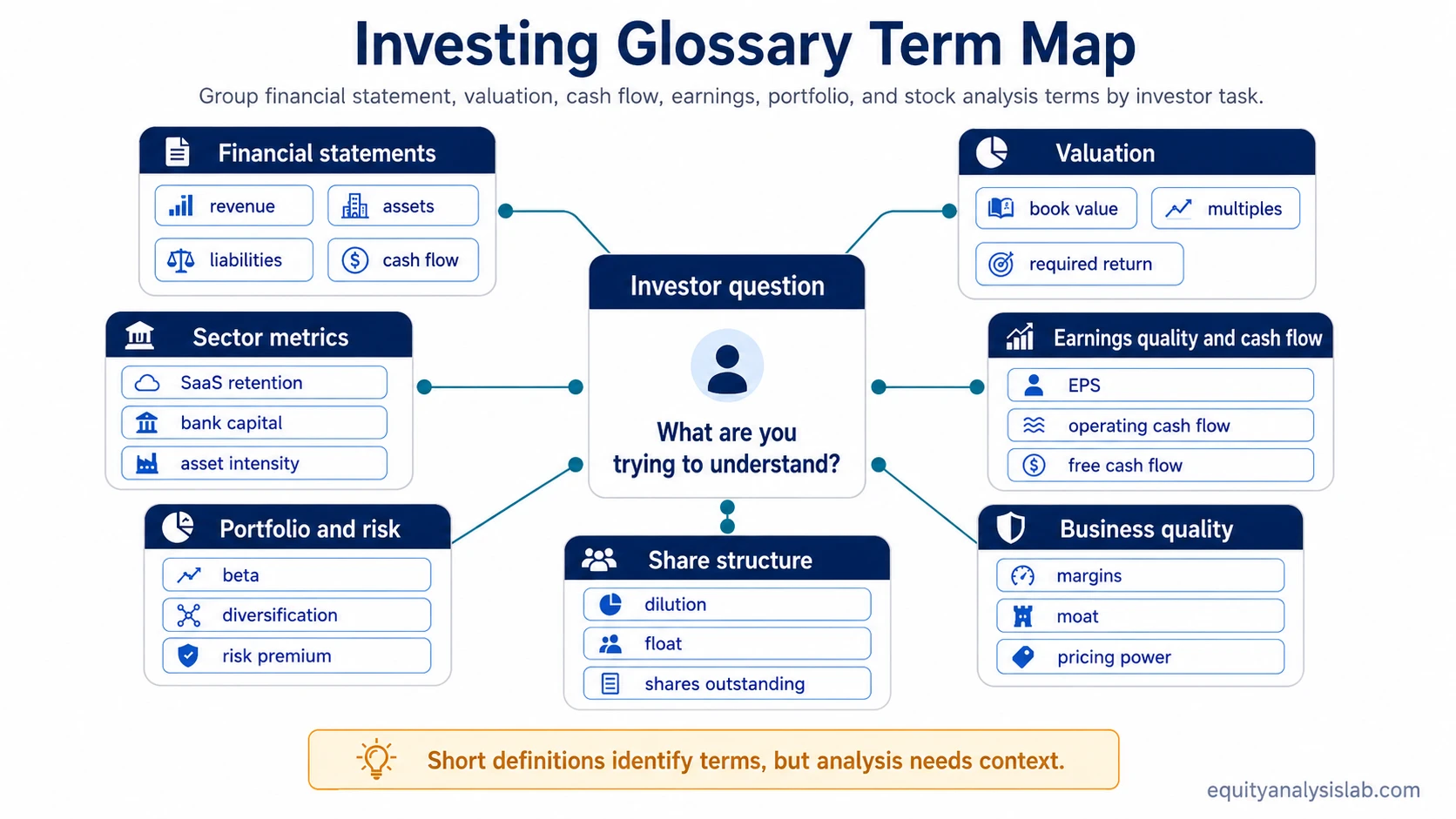

Investing terms are easier to use when they are grouped by the question an investor is trying to answer. Financial statement terms describe what a company reports, valuation terms frame what investors are paying for, cash-flow and earnings terms test quality, and portfolio terms connect a single stock to risk at the portfolio level.

The focus is investor analysis, not personal budgeting, trading execution, startup equity compensation, or regulatory terminology. A short definition can identify the term, but the next step is usually to connect that term to the specific investor question it helps answer.

Browse by term family: financial statements, valuation, earnings quality and cash flow, business quality, share structure, portfolio and risk, and sector metrics.

Browse Investing Glossary Terms

Use the glossary term pages for short reference definitions, then move into the stronger entity pages when the investing question needs full analysis context.

| Term family | Glossary terms |

|---|---|

| Valuation and required return | beta, cost of equity, weighted average cost of capital, exit multiple |

| Book value and working capital | book value, working capital, net working capital, deferred revenue |

| Earnings and margins | EBIT, EBITDA, EBIT vs EBITDA, gross profit, gross margin vs operating margin |

| Cash-flow valuation | free cash flow to equity, free cash flow to the firm, FCFF vs FCFE |

| SaaS and customer economics | churn rate, revenue churn, net dollar retention, customer acquisition cost, lifetime value, LTV CAC ratio |

Start With the Investor Task

Many investing terms overlap because they describe different parts of the same company or portfolio. The cleanest starting point is the task: reading statements, valuing the business, checking cash quality, understanding ownership, or comparing risk.

| Investor task | Start with these concepts | Why they matter | Best next page |

|---|---|---|---|

| Understand company cash generation | Operating cash flow, capital expenditures, free cash flow, cash conversion | Cash-flow terms help separate reported profit from the cash a business can reinvest, repay, or return to shareholders. | free cash flow |

| Read balance-sheet valuation language | Book value, book value per share, price-to-book, tangible equity | Balance-sheet valuation terms help investors compare accounting equity, asset backing, and market price in context. | book value per share |

| Compare portfolio risk assumptions | Beta, expected return, risk premium, diversification, CAPM | Portfolio-risk terms help connect individual securities to broader portfolio exposure and required-return assumptions. | capital asset pricing model |

| Interpret SaaS revenue quality | ARR, churn, retention, expansion, net revenue retention | SaaS metrics help investors distinguish reported growth from recurring-revenue durability and customer expansion quality. | net revenue retention |

Financial Statement Terms

Financial statement terms describe the accounting reports investors use to understand a business. Income statement terms focus on revenue, expenses, margins, and profit. Balance sheet terms focus on assets, liabilities, equity, debt, working capital, and share structure. Cash flow statement terms focus on the movement of cash through operations, investment, and financing.

Common starting terms: revenue, gross profit, operating income, net income, assets, liabilities, shareholders’ equity, working capital, operating cash flow, capital expenditures, and free cash flow.

Use boundary: a financial statement term names the reported item, but analysis depends on scale, trend, business model, accounting policy, and comparison with peers or prior periods.

For example, net income and operating cash flow can both appear positive while telling different stories about the business. Net income is an accounting profit measure. Operating cash flow focuses on cash generated from the company’s core operations before investment and financing choices are considered.

Valuation Terms

Valuation terms describe the relationship between a company’s price, financial base, growth expectations, asset backing, and future cash-flow assumptions. Some terms compare market value with earnings or sales. Others compare market value with book value, free cash flow, enterprise value, or expected future cash flows.

Common starting terms: market capitalization, enterprise value, price-to-earnings ratio, forward P/E, EV/EBITDA, price-to-sales ratio, price-to-book ratio, intrinsic value, margin of safety, discount rate, and terminal value.

Use boundary: a valuation multiple is a comparison tool, not a conclusion by itself. The same multiple can imply different things depending on growth durability, margin quality, capital intensity, debt, cyclicality, and accounting quality.

Book-based terms are most useful when the balance sheet is central to the investment question. Earnings and cash-flow terms are usually more useful when the investor is comparing operating performance, reinvestment needs, and long-term earning power.

Earnings Quality and Cash Flow Terms

Earnings quality terms test whether accounting profit is durable, repeatable, and supported by cash generation. Cash-flow terms show whether a business is producing cash after normal operating needs and capital spending.

| Term family | What it helps answer | Common interpretation boundary |

|---|---|---|

| Earnings terms | How much profit is reported for common shareholders? | Earnings can be affected by accounting estimates, one-time items, margins, tax effects, and share count changes. |

| Cash-flow terms | How much cash does the business generate through operations and after investment needs? | Cash flow can vary with working capital, capital intensity, timing, and investment cycle. |

| Quality terms | How repeatable and reliable are the reported results? | Quality depends on durability, cash conversion, accounting clarity, customer behavior, and business model stability. |

Accounting profit and cash generation are related, but they are not the same concept. A company can report profit while consuming cash, or generate strong cash flow during a period when accounting profit is temporarily pressured.

Business Quality Terms

Business quality terms describe the strength, durability, and economics of the company behind the financial statements. The useful question is whether the business can defend margins, reinvest well, retain customers, and convert growth into shareholder value.

Common starting terms: gross margin, operating margin, net margin, return on invested capital, pricing power, economic moat, customer concentration, unit economics, capital allocation, and competitive advantage.

Use boundary: quality terms should be connected to evidence. A company is not high quality simply because one margin or return metric looks strong in isolation.

Margin terms describe profitability at different levels of the business. Moat and pricing-power terms describe whether those economics may be defensible. Unit-economics terms connect customer-level or product-level economics to the wider company model.

Share Structure Terms

Share structure terms describe the ownership base that sits underneath per-share analysis. They matter because a company’s total value and a shareholder’s claim on that value are not always the same question.

| Term | Plain meaning | Investor use |

|---|---|---|

| Shares outstanding | The number of company shares currently issued and held by shareholders. | Used in market capitalization, earnings per share, and ownership dilution analysis. |

| Diluted shares | A share count that includes potential shares from instruments such as options, warrants, or convertibles when relevant. | Helps investors avoid overstating per-share value when future issuance is possible. |

| Free float | The portion of shares generally available for public trading. | Useful when thinking about liquidity, index inclusion, and market ownership structure. |

| Buybacks | Company repurchases of its own shares. | Can reduce share count, but the effect depends on price paid, funding source, dilution offset, and business quality. |

Per-share metrics become more useful when the share count is stable or clearly understood. If dilution, buybacks, or convertible securities are material, the investor needs both company-level results and ownership-level context.

Portfolio and Risk Terms

Portfolio and risk terms connect individual securities to the wider portfolio. These terms do not replace company analysis. They frame exposure, diversification, volatility, return assumptions, and how one position may affect the portfolio as a whole.

Common starting terms: risk, volatility, drawdown, diversification, concentration, correlation, beta, expected return, risk premium, asset allocation, rebalancing, and capital asset pricing model.

Use boundary: risk terms are context-dependent. A high-quality company can still create portfolio risk if the position size, valuation, sector exposure, or correlation profile is poorly understood.

Beta and expected return are portfolio-language terms, not complete investment judgments. They can help organize assumptions, but they still need to be interpreted alongside the company’s fundamentals, valuation, time horizon, and portfolio role.

Sector and SaaS Metric Terms

Some terms only become useful inside a specific business model. A bank, insurer, industrial company, software company, and commodity producer may all require different vocabulary because their economics are built differently.

| Business area | Useful term families | What the terms usually clarify |

|---|---|---|

| SaaS and subscription software | ARR, churn, retention, expansion, CAC, gross margin, net revenue retention | Recurring revenue quality, customer durability, acquisition efficiency, and expansion economics. |

| Banks and financials | Net interest margin, deposits, loan losses, capital ratios, tangible book value | Funding quality, credit risk, balance-sheet strength, and profitability. |

| Capital-intensive businesses | Capital expenditures, depreciation, maintenance capex, free cash flow, return on invested capital | How much reinvestment is needed to sustain or grow the business. |

Sector metrics should not be mixed mechanically across business models. A metric that is central for a SaaS company may be secondary or irrelevant for a bank, utility, retailer, or commodity producer.

How to Use Short Definitions Safely

Short definitions are useful for identifying a term, but investing analysis requires context. A term can name the metric, formula, or concept without telling the reader whether the business is strong, weak, cheap, expensive, improving, or deteriorating.

Definition-use boundary: no single investing term should be treated as a complete answer. A valuation term needs business-quality context. A profitability term needs cash-flow context. A risk term needs portfolio context. A sector metric needs business-model context.

The safer pattern is to move from definition to use case: what the term measures, where it appears, what question it helps answer, and what it cannot answer alone. That prevents a lookup from turning into a one-metric conclusion.

FAQ

What is the difference between an investing glossary and a financial glossary?

A financial glossary can include many broad money, banking, personal-finance, accounting, and regulatory terms. An investing glossary is narrower: it focuses on terms investors use to understand securities, companies, valuation, portfolios, financial statements, risk, and market context.

Are glossary definitions enough to analyze a stock?

No. A definition identifies a term, but stock analysis requires context such as trend, quality, comparability, business model, valuation, balance-sheet strength, share structure, and portfolio role.

Why are some sector terms separated from general investing terms?

Sector terms are separated because business models differ. SaaS retention metrics, bank capital terms, and capital-intensive cash-flow terms answer different investor questions and should not be interpreted as interchangeable signals.