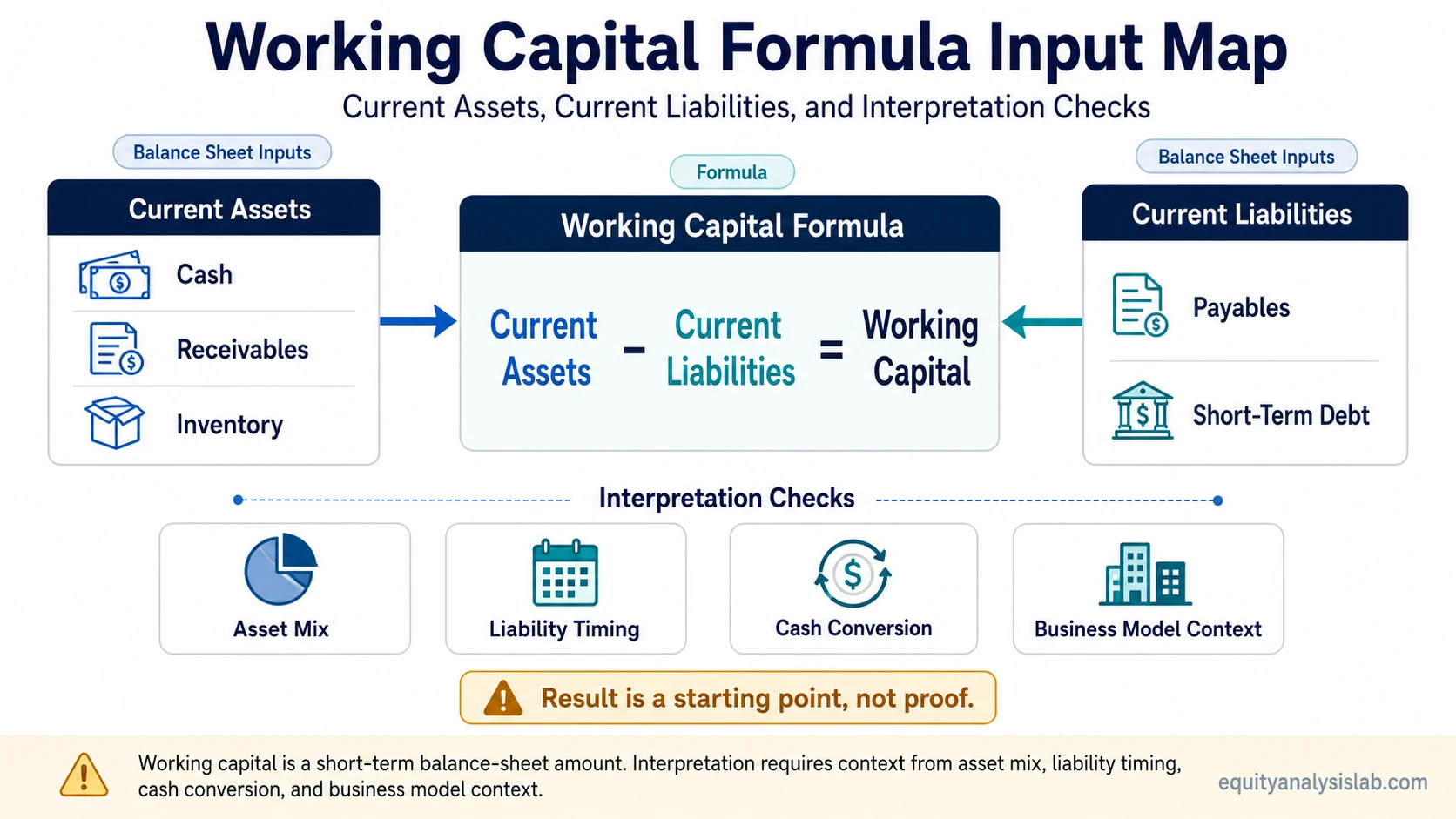

Working capital is current assets minus current liabilities. The inputs come from the balance sheet, but the number becomes useful for investors only after checking asset mix, liability timing, cash conversion, and business-model context.

Definition: Working capital measures the short-term resources left after a company’s current liabilities are deducted from its current assets.

A positive number can show that current assets exceed short-term obligations. A negative number can show that short-term obligations exceed current assets. The useful interpretation depends on what sits inside the current asset and current liability accounts.

Key Points

- Working capital is calculated as current assets minus current liabilities.

- The inputs come from the current sections of the balance sheet.

- A large positive number can still be low quality if receivables are slow to collect or inventory is building.

- A negative number can be risky in some businesses but normal in others with fast cash collection and favorable supplier timing.

- Working capital should be cross-checked against liquidity ratios, cash conversion timing, and operating efficiency.

Working Capital Formula

The working capital formula is:

Working Capital = Current Assets − Current Liabilities

Current assets are assets expected to be converted into cash, sold, used, or collected within the normal operating cycle or within one year. Current liabilities are obligations expected to be paid within the normal operating cycle or within one year.

The formula gives a dollar amount, not a ratio. That makes it useful for seeing the short-term funding cushion in absolute terms, but less useful when comparing companies of very different size without additional context.

Where Working Capital Appears on the Balance Sheet

Working capital is not usually shown as one required line item. It is calculated from the current asset and current liability sections of the balance sheet.

| Input | Common items | Investor interpretation issue |

|---|---|---|

| Current assets | Cash, short-term investments, accounts receivable, inventory, prepaid expenses | Not every current asset has the same liquidity quality or collection certainty. |

| Current liabilities | Accounts payable, accrued expenses, short-term debt, current lease obligations, current tax liabilities | Payment timing can change the working-capital number without changing long-term business quality. |

| Working capital result | Current assets minus current liabilities | The final amount needs composition, timing, and business-model checks before interpretation. |

The same working-capital figure can have different meanings depending on whether it is supported by cash and collectible receivables or inflated by slow-moving inventory and delayed collections.

How Investors Interpret Working Capital

Positive working capital means current assets exceed current liabilities. That can support operating flexibility, but it does not prove strong liquidity quality. A company may report positive working capital because receivables have increased faster than cash collections or because inventory has accumulated ahead of demand.

Negative working capital means current liabilities exceed current assets. That can be a warning sign when the company lacks cash, depends on short-term debt, or faces near-term refinancing pressure. In some business models, however, negative working capital can appear when customers pay quickly and suppliers are paid later.

Limitation: Working capital is a balance-sheet amount, not a complete quality test. It does not prove solvency, business strength, valuation attractiveness, stock safety, or future return potential on its own.

The better interpretation starts with the direction and size of the number, then checks whether the change came from cash, receivables, inventory, payables, short-term debt, or seasonal timing.

Working Capital Example

A hypothetical company reports current assets of 120 and current liabilities of 80. Its working capital is 40.

Example: 120 of current assets minus 80 of current liabilities equals 40 of working capital.

That 40 cushion looks stronger if most of the current assets are cash and receivables that are collected on time. It looks weaker if the increase came mainly from inventory buildup, overdue receivables, or prepaid items that cannot easily fund near-term obligations.

A second company could also report 40 of working capital but have a different risk profile because its current liabilities include more short-term debt or because its receivables turn into cash more slowly. The number is the starting point; the composition explains the quality.

Working Capital vs Current Ratio

Working capital measures liquidity as an absolute dollar amount. The current ratio measures liquidity as current assets divided by current liabilities.

| Metric | Formula | Best use |

|---|---|---|

| Working capital | Current assets − current liabilities | Shows the short-term resource cushion in dollar terms. |

| Current ratio | Current assets ÷ current liabilities | Shows the relationship between current assets and current liabilities as a ratio. |

A large company can have more working capital than a smaller company while still having a weaker ratio. That is why the dollar amount and the ratio answer related but different questions.

What Working Capital Can Hide

Working capital can look comfortable even when the underlying current assets are becoming less useful. Slow receivable collection, excess inventory, and rising prepaid balances can make current assets look larger without creating the same cash flexibility as cash itself.

Current liabilities also need timing context. A rise in payables may preserve cash in the short term, but it can also reflect delayed supplier payments, seasonal purchasing, or changing payment terms. The cash conversion cycle helps connect receivables, inventory, and payables into a timing view rather than treating working capital as a single static number.

| Cross-check | Question to ask | Why it matters |

|---|---|---|

| Receivables quality | Are receivables growing faster than sales or taking longer to collect? | Reported current assets may not convert into cash as quickly as the balance sheet suggests. |

| Inventory quality | Is inventory rising because of planned growth, weak demand, or product obsolescence risk? | Inventory is usually less liquid than cash and may require markdowns or write-downs. |

| Payables timing | Are suppliers being paid later than usual? | Delayed payments can temporarily support cash but may not reflect durable operating strength. |

| Short-term debt | Are near-term obligations rising faster than cash generation? | Working capital can deteriorate quickly when debt maturities or current borrowings increase. |

| Business model | Does the company normally collect cash before or after it must pay suppliers? | Retail, subscription, manufacturing, and project-based businesses can have very different normal working-capital profiles. |

Working Capital and Operating Efficiency

Working capital is a balance-sheet amount at a point in time. It does not show how much revenue the company generates from that working-capital base.

When the question shifts from liquidity cushion to efficiency, the analysis moves toward how much revenue is produced from the working-capital base. That distinction matters because two companies can hold similar working-capital amounts while using them very differently.

A static working-capital amount is most useful when paired with trend, composition, and efficiency checks. Rising working capital can support growth, but it can also signal cash tied up in receivables or inventory. Falling working capital can improve efficiency, but it can also create pressure if near-term obligations are rising faster than liquid assets.

What Working Capital Can and Cannot Show

| Working capital can show | Working capital cannot show alone |

|---|---|

| Whether current assets exceed current liabilities in dollar terms | Whether every current asset is high quality or quickly collectible |

| The size of the short-term balance-sheet cushion | Whether the company is attractively valued |

| Changes in near-term operating funding needs | Whether positive working capital is good or negative working capital is bad |

| Potential pressure from short-term obligations | Whether the stock is safe or likely to produce future returns |

FAQ

What is working capital in simple terms?

Working capital is the amount left after a company subtracts current liabilities from current assets. It shows the short-term balance-sheet cushion in dollar terms.

Is positive working capital always good?

No. Positive working capital can be useful, but it may be less attractive if it comes from slow receivables, excess inventory, or other assets that do not convert into cash easily.

Is negative working capital always bad?

No. Negative working capital can be risky when liquidity is weak, but it can be normal in some businesses that collect cash quickly and pay suppliers later.

How is working capital different from current ratio?

Working capital is a dollar amount calculated as current assets minus current liabilities. Current ratio is a ratio calculated as current assets divided by current liabilities.