Cash conversion cycle measures how long cash is tied up as a company buys or produces inventory, sells that inventory, collects from customers, and pays suppliers. It combines days inventory outstanding, days sales outstanding, and days payable outstanding into one working-capital timing metric.

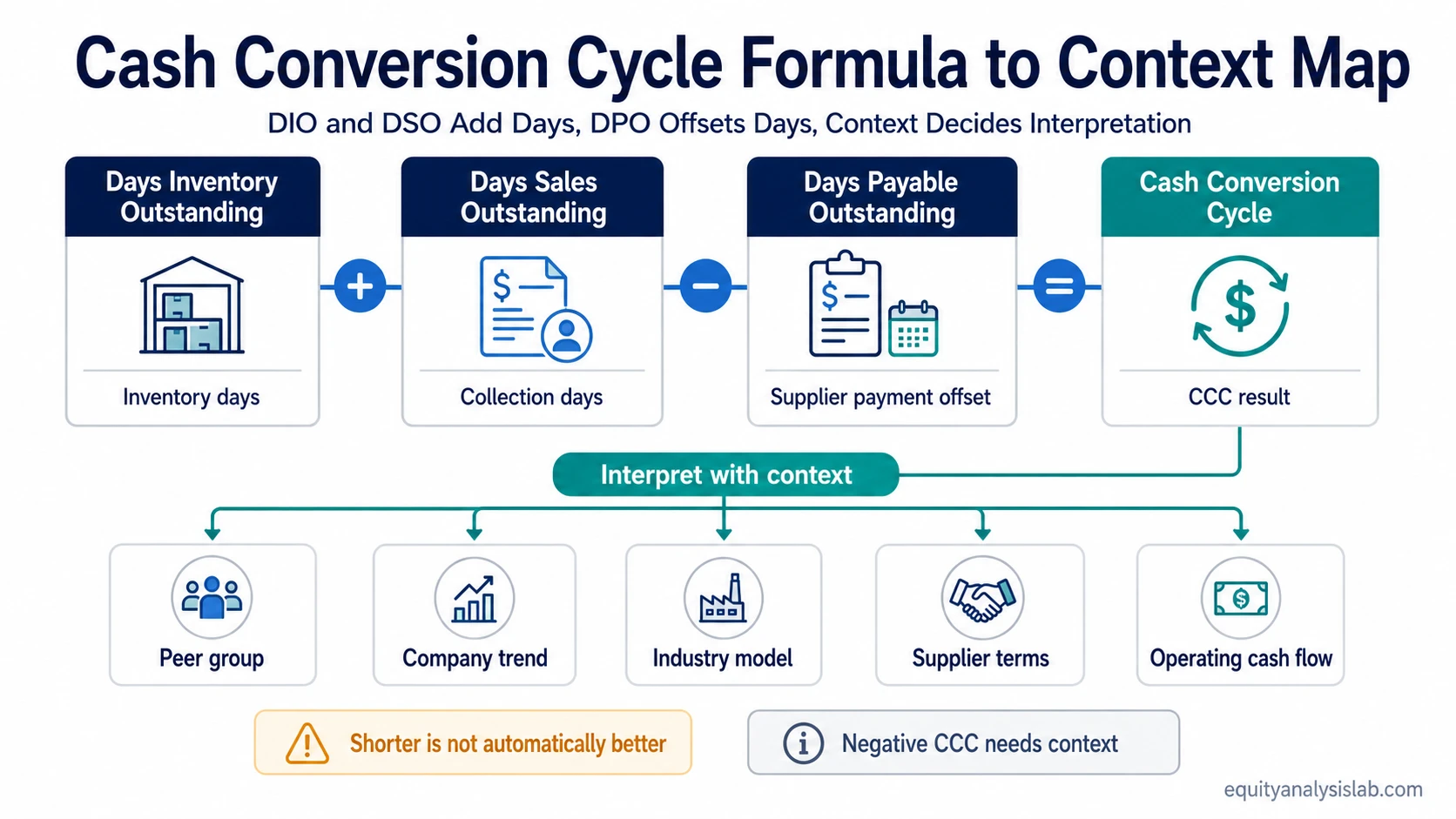

A shorter cash conversion cycle can suggest that cash moves back into the business faster, but the number is not proof of company quality by itself. It needs peer context, trend context, industry context, and a check against actual cash-flow strength before it can support an investor interpretation.

What Cash Conversion Cycle Measures

The cash conversion cycle, often shortened to CCC, measures the number of days between cash being committed to inventory and cash being recovered from customer collections, after accounting for the delay created by supplier payment terms.

The metric connects three working-capital movements that investors often read separately: inventory movement, customer collection speed, and supplier-payment timing. A company with slow inventory turnover, slow customer collections, or weak supplier terms may show a longer cash conversion cycle even if revenue is growing.

CCC is most useful as a diagnostic timing measure. It helps answer whether cash is being absorbed or released by the operating cycle, but it does not prove that a business is cheap, durable, high quality, or attractive as an investment.

Cash Conversion Cycle Formula

The standard cash conversion cycle formula is:

Cash Conversion Cycle = Days Inventory Outstanding + Days Sales Outstanding – Days Payable Outstanding

Days inventory outstanding measures how long inventory remains in the business before it is sold. Days sales outstanding measures how long it takes to collect cash from customers after a sale. Days payable outstanding measures how long the company takes to pay suppliers.

| Component | What it measures | Effect on CCC | What can mislead interpretation |

|---|---|---|---|

| Days inventory outstanding | How many days inventory is held before sale | Higher DIO increases CCC | Seasonal inventory builds, strategic stocking, or temporary demand weakness can distort the reading |

| Days sales outstanding | How many days it takes to collect from customers | Higher DSO increases CCC | Customer mix, credit terms, billing timing, or delayed collections can change the number |

| Days payable outstanding | How many days the company takes to pay suppliers | Higher DPO reduces CCC | Extended supplier terms can help liquidity, but may also reflect pressure on suppliers or short-term working-capital management |

DPO is the payables offset in the formula. Because the metric subtracts supplier-payment time, a company that pays suppliers later can show a shorter CCC even if inventory and receivable timing have not improved. That is why the payables side should be read alongside the accounts payable turnover ratio rather than treated as a standalone improvement.

Cash Conversion Cycle and Operating Cycle

Cash conversion cycle is closely related to the operating cycle, but the two are not identical. The operating cycle measures the inventory-to-cash process before the supplier-payment offset. CCC then subtracts DPO to show how much of that process must be financed by the company after payables timing is considered.

Cash Conversion Cycle = Operating Cycle – Days Payable Outstanding

This distinction matters because two companies can have similar inventory and collection timing but different CCC readings if one has more favorable supplier terms. For that reason, CCC should not be read as only an inventory or receivables metric. It is a combined working-capital timing measure that starts with the operating cycle and then adjusts for supplier-payment timing.

How to Interpret Cash Conversion Cycle

A lower cash conversion cycle usually means cash is tied up for fewer days before returning to the business. A higher cash conversion cycle usually means more cash is committed to inventory and receivables before supplier-payment timing offsets that commitment. The interpretation is useful, but only when the business model is comparable.

| CCC reading | Possible interpretation | What to check before concluding |

|---|---|---|

| Shorter CCC | Cash may be moving through working capital more quickly | Check whether the improvement comes from real inventory and collection efficiency or from stretched supplier payments |

| Longer CCC | More cash may be tied up in inventory and receivables | Check whether the increase reflects growth investment, seasonality, weak demand, or collection pressure |

| Positive CCC | The company generally funds part of the working-capital cycle before cash is collected | Compare against peers and the company’s own history rather than using a universal threshold |

| Negative CCC | The company may collect cash before it needs to pay suppliers | Check whether the structure is sustainable, industry-normal, or dependent on unusual supplier terms |

A negative CCC can be attractive in some business models, especially where customers pay quickly and suppliers are paid later. It is still not automatically a superior-business signal. The key question is whether the structure comes from a durable operating model or from timing that could reverse.

Cash Conversion Cycle Example

A simple CCC calculation can start with three working-capital timing inputs: 60 days of inventory outstanding, 35 days of sales outstanding, and 45 days of payables outstanding.

CCC = 60 + 35 – 45 = 50 days

This means cash is tied up for about 50 days across the inventory, receivables, and payables timing chain. If DIO rises from 60 to 75 while DSO and DPO stay the same, CCC rises to 65 days. That could indicate slower inventory movement, but it could also reflect a planned inventory build before a seasonal sales period.

If DSO rises from 35 to 50 while the other inputs remain unchanged, CCC also rises by 15 days. That points toward slower customer collection. If DPO rises from 45 to 60, CCC falls by 15 days, but the improvement comes from paying suppliers later, not necessarily from better inventory or collection efficiency.

When Cash Conversion Cycle Can Mislead

Cash conversion cycle can mislead when it is treated as a universal quality score. A short CCC in one industry may be normal, while a longer CCC in another industry may simply reflect inventory-heavy operations, production lead times, or customer credit terms.

Seasonality can also distort the metric. A retailer may carry more inventory before a major selling season, which can temporarily lift DIO and CCC. A manufacturer may show a longer cycle because production and delivery happen over a longer period. A software or subscription business may have a very different working-capital pattern because inventory is less central to the model.

Accounting timing matters as well. Balance-sheet snapshots can capture temporary changes in receivables, inventory, or payables. A single-period CCC reading should therefore be checked against multi-period trends, peer norms, and the company’s actual cash generation. When the question is whether operating cash flow covers near-term obligations, the operating cash flow ratio is a better boundary metric than CCC.

Cash Conversion Cycle vs Related Metrics

Cash conversion cycle overlaps with several operating-efficiency metrics, but each answers a different question. CCC combines inventory, receivables, and payables timing into one day-based measure. Operating cycle focuses on the inventory-to-cash process before the payables offset. Accounts payable turnover focuses on supplier-payment activity. Operating cash flow ratio focuses on cash-flow coverage of current liabilities.

| Metric | Main question answered | Boundary against CCC |

|---|---|---|

| Cash conversion cycle | How long is cash tied up in the full inventory, receivables, and payables timing chain? | Combines DIO, DSO, and DPO into one working-capital timing measure |

| Operating cycle | How long does the inventory-to-cash process take before supplier payment timing? | Does not subtract the payables offset in the same way CCC does |

| Accounts payable turnover ratio | How actively does the company pay suppliers relative to purchases or cost of goods sold? | Focuses on payables behavior rather than the full cash-timing chain |

| Operating cash flow ratio | How well does operating cash flow cover current liabilities? | Measures cash-flow coverage, not working-capital timing in days |

For investors, CCC is most useful when it is read as part of a broader operating-efficiency picture. The metric can highlight where cash is being absorbed or released, but it should be tested against margins, revenue growth, working-capital changes, supplier terms, cash-flow statements, and peer norms before any business-quality conclusion is drawn.

Key Points

- Cash conversion cycle measures working-capital timing across inventory, receivables, and payables.

- The formula is DIO plus DSO minus DPO.

- A shorter CCC can suggest faster cash recovery, but the source of the change matters.

- A negative CCC can be structurally favorable in some models, but it is not automatically proof of business quality.

- CCC should be compared against peers, company history, industry norms, and cash-flow evidence.

FAQ

What is the cash conversion cycle?

The cash conversion cycle is a working-capital timing metric that measures how many days cash is tied up across inventory, customer collections, and supplier payments.

What is the cash conversion cycle formula?

The formula is Cash Conversion Cycle = Days Inventory Outstanding + Days Sales Outstanding – Days Payable Outstanding.

Is a negative cash conversion cycle good?

A negative cash conversion cycle can be favorable when a company collects from customers before it pays suppliers, but it still needs business-model, supplier-term, and cash-flow context.

How is cash conversion cycle different from operating cycle?

Operating cycle measures the inventory-to-cash process before payables timing. Cash conversion cycle subtracts days payable outstanding to show the timing burden after supplier-payment terms are considered.

Does a shorter cash conversion cycle always mean a better company?

No. A shorter cash conversion cycle can reflect faster cash recovery, but it can also reflect stretched supplier payments or business-model differences. It should not be treated as proof of company quality by itself.