Operating cycle is the number of days a company’s cash is tied up in inventory and receivables before it is collected from customers. It measures the timing from inventory purchase or production through sale and collection.

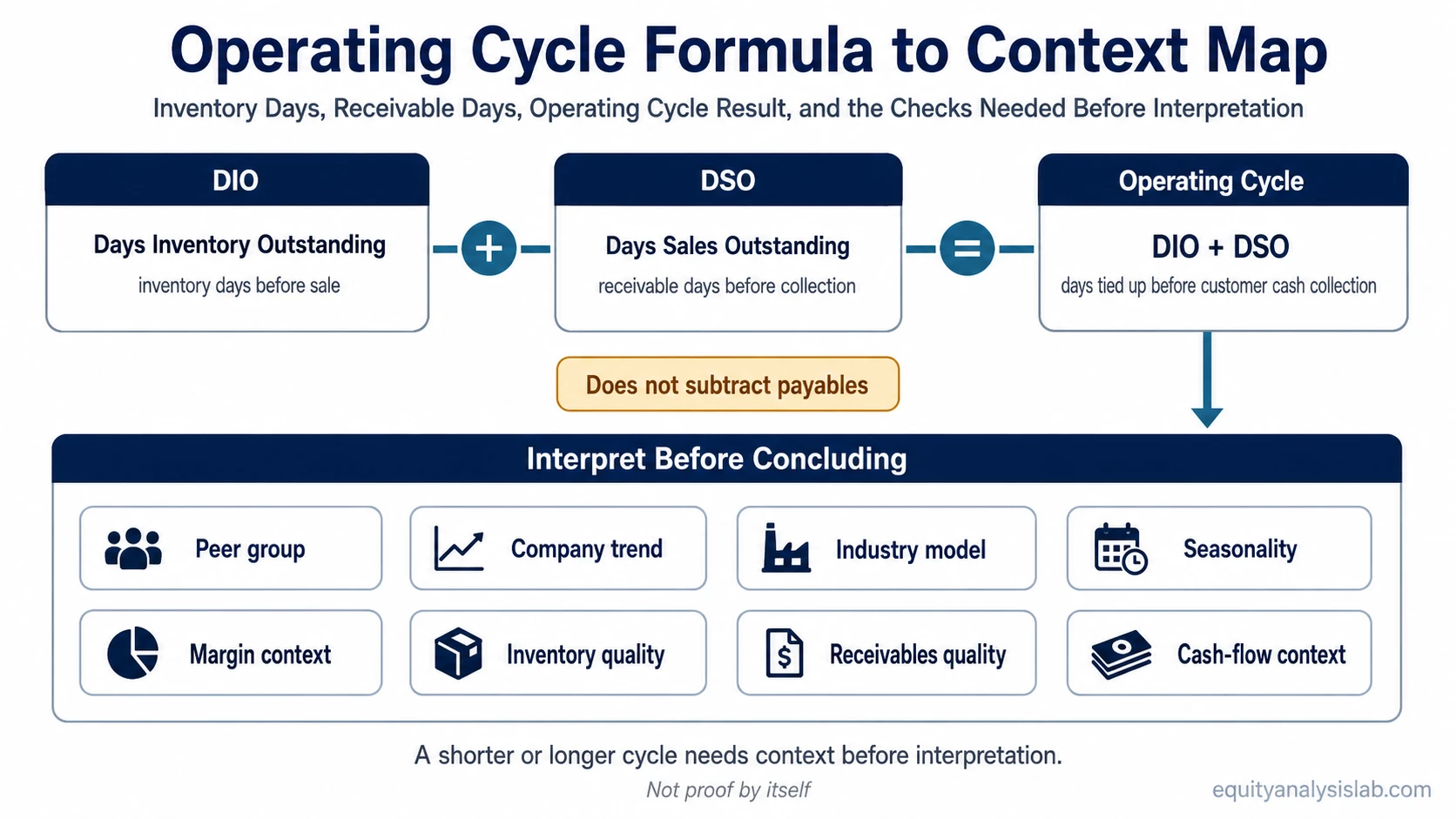

Operating cycle does not subtract supplier-payment timing and does not prove business quality by itself.

What it is: a days-based working-capital timing measure that combines inventory holding time and customer collection time.

What it is not: a valuation metric, a stock-selection signal, proof of cash-flow quality, or a complete cash conversion measure that includes payables.

For investors, the operating cycle is useful because it shows how long operating capital can remain inside inventory and accounts receivable before it returns as cash. The result is most useful when compared with the company’s own history, similar peers, industry norms, and the quality of the underlying inventory and receivables.

Operating Cycle Formula

The standard operating cycle formula is:

Operating Cycle = Days Inventory Outstanding + Days Sales Outstanding

The same idea is sometimes written as:

Operating Cycle = Inventory Period + Accounts Receivable Period

Days inventory outstanding measures how long inventory stays in the business before it is sold. Days sales outstanding measures how long receivables remain uncollected after the sale. Adding the two gives the total operating days tied up before customer cash collection.

What the Formula Inputs Mean

The operating cycle depends on two timing measures: DIO and DSO. Each measure uses an income-statement flow item and an average balance-sheet item, so the quality of the calculation depends on using the right input base.

DIO = Average Inventory / Cost of Goods Sold × Period Days

DSO = Average Accounts Receivable / Credit Sales × Period Days

| Formula part | Common input | What it measures | Interpretation caveat |

|---|---|---|---|

| Days Inventory Outstanding | Average inventory, cost of goods sold, period days | How many days inventory is held before sale | Ending inventory can distort the result if inventory levels changed sharply near period end. |

| Days Sales Outstanding | Average accounts receivable, credit sales or revenue proxy, period days | How many days customer receivables take to convert into cash | Revenue may be used as a proxy when credit sales are not disclosed, but it may be less precise. |

| Period days | Usually 365 for annual analysis or about 90 for quarterly analysis | Converts turnover into days | Use a consistent period when comparing companies or trends. |

Average inventory and average accounts receivable usually mean the average of beginning and ending balances for the period. More detailed averages can be useful for seasonal businesses, but the same method should be applied consistently across comparisons.

Operating Cycle vs Cash Conversion Cycle

Operating cycle and cash conversion cycle are related, but they are not the same formula. Operating cycle adds inventory days and receivable days. Cash conversion cycle then subtracts days payable outstanding.

| Metric | Formula logic | What it includes | What it excludes |

|---|---|---|---|

| Operating cycle | DIO + DSO | Inventory timing and receivable collection timing | Supplier-payment timing |

| Cash conversion cycle | DIO + DSO – DPO | Inventory, receivables, and payables timing | Broader profitability, valuation, or stock return analysis |

This difference matters because two companies can have the same operating cycle but different cash conversion cycles if one company receives longer supplier-payment terms. Operating cycle focuses on inventory and receivables. It does not show how much supplier financing offsets that timing.

Operating Cycle Example

A simplified example can show how the calculation works. Suppose a company holds inventory for 45 days before sale and then collects receivables 30 days after the sale.

| Step | Amount | Meaning |

|---|---|---|

| Days Inventory Outstanding | 45 days | Inventory is held for about 45 days before sale. |

| Days Sales Outstanding | 30 days | Receivables are collected about 30 days after sale. |

| Operating cycle | 75 days | Cash is tied up for about 75 days before customer collection. |

The 75-day result is not automatically good or bad. It depends on the company’s business model, inventory type, customer terms, margins, financing needs, and comparison set.

How to Interpret Operating Cycle

A shorter operating cycle usually means inventory and receivables convert into cash more quickly. A longer operating cycle usually means cash remains tied up in operations for more time. But the interpretation is not mechanical.

- Peer group: compare the result with companies that have similar products, credit terms, and inventory models.

- Company trend: review whether the cycle is improving or worsening over several periods.

- Industry model: some industries naturally carry more inventory or offer longer customer terms.

- Seasonality: period-end balances can shift sharply around holidays, production cycles, or ordering seasons.

- Margin context: a longer cycle can be more acceptable if margins and pricing power compensate for working-capital intensity.

- Inventory quality: slow movement can reflect normal product cycles or potential obsolescence.

- Receivables quality: rising DSO can reflect customer growth, looser credit, billing delays, or collection risk.

- Cash-flow context: operating-cycle analysis should be checked against operating cash flow and working-capital movement.

The most useful reading comes from separating normal business-model timing from deterioration in inventory movement or customer collections.

Common Interpretation Mistakes

Mistake 1: treating a shorter operating cycle as automatically superior. A short cycle can be efficient, but it can also reflect understocking, weak sales terms, or a business model with limited inventory needs.

Mistake 2: comparing companies across different industries without adjustment. A grocery retailer, software company, equipment manufacturer, and luxury-goods business can have very different normal operating cycles.

Mistake 3: ignoring balance-sheet quality. A stable operating cycle can hide aging inventory or receivables that are becoming harder to collect.

Mistake 4: confusing operating cycle with cash conversion cycle. Payables are not part of the operating cycle formula.

What Changes the Operating Cycle

Operating cycle can change for operational, accounting, and business-model reasons. Investors should look for the driver before interpreting the result.

| Change | Possible explanation | Question to ask |

|---|---|---|

| DIO rises | Inventory is moving more slowly, inventory build is intentional, or demand is weaker than expected. | Is inventory build linked to growth, seasonality, or unsold product? |

| DIO falls | Inventory is selling faster, inventory levels are leaner, or supply is constrained. | Is the company more efficient, or is it risking stockouts? |

| DSO rises | Customers are paying more slowly, credit terms are looser, or revenue recognition and collection timing diverge. | Are receivables growing faster than sales? |

| DSO falls | Collections are faster, customer mix changed, or payment terms became tighter. | Is collection improvement sustainable without hurting sales? |

Operating Cycle and Related Efficiency Ratios

Operating cycle is part of a broader operating-efficiency toolkit. It should be read alongside ratios that isolate inventory movement, receivable collection, payable timing, and operating cash-flow support.

| Metric | Main question | How it relates to operating cycle |

|---|---|---|

| Days Inventory Outstanding | How long does inventory stay before sale? | First part of the operating cycle. |

| Days Sales Outstanding | How long does customer collection take? | Second part of the operating cycle. |

| Days Payable Outstanding | How long does the company take to pay suppliers? | Not part of operating cycle, but used in cash conversion cycle. |

| Accounts payable turnover ratio | How quickly are supplier obligations being paid? | Useful for supplier-payment context, but not included in operating cycle. |

| Operating cash flow ratio | How well does operating cash flow cover current liabilities? | Helps check whether working-capital timing is supported by cash generation. |

Limitations of Operating Cycle

Operating cycle is a timing measure, not a complete judgment of company quality. It does not show profitability, pricing power, debt risk, supplier financing, capital intensity, or valuation.

It can also be distorted by seasonality, acquisitions, changing product mix, large customer contracts, one-time inventory builds, and unusual period-end balance-sheet levels.

For that reason, operating cycle should be used as a diagnostic tool. It is strongest when it helps identify the next question: whether changes in inventory and receivables reflect normal business activity, improved efficiency, or emerging working-capital pressure.

FAQ

Does operating cycle include payables?

No. Operating cycle does not include payables. Payables are included in the cash conversion cycle, which subtracts days payable outstanding from inventory days plus receivable days.

Is a shorter operating cycle always better?

No. A shorter operating cycle can indicate faster cash recovery, but it is not automatically better. The result must be interpreted with peer comparison, company trend, industry model, margins, inventory quality, and receivable quality.

Why can operating cycle change over time?

Operating cycle can change because inventory moves faster or slower, customers pay more quickly or more slowly, seasonality changes balance-sheet levels, or the business changes its stocking, production, or credit policies.