LTV/CAC ratio compares the lifetime value of a customer with the cost required to acquire that customer. It helps investors read customer economics, but the result depends on the LTV basis, CAC scope, margin assumption, cohort, and time period used in the calculation.

Definition: LTV/CAC ratio is a customer-economics ratio that divides estimated customer lifetime value by customer acquisition cost. A higher ratio means estimated customer value is larger relative to acquisition cost, but the number is reliable only when the numerator and denominator are built on comparable assumptions.

Key Points

- LTV/CAC is calculated as customer lifetime value divided by customer acquisition cost.

- The ratio can change materially depending on whether LTV is revenue-based, gross-margin-based, or contribution-based.

- CAC must be checked for scope because some calculations include only marketing spend while others include sales salaries, commissions, tools, partners, or onboarding costs.

- A strong headline ratio does not prove business quality unless retention, margin, cohort, expansion revenue, and cash timing also support the interpretation.

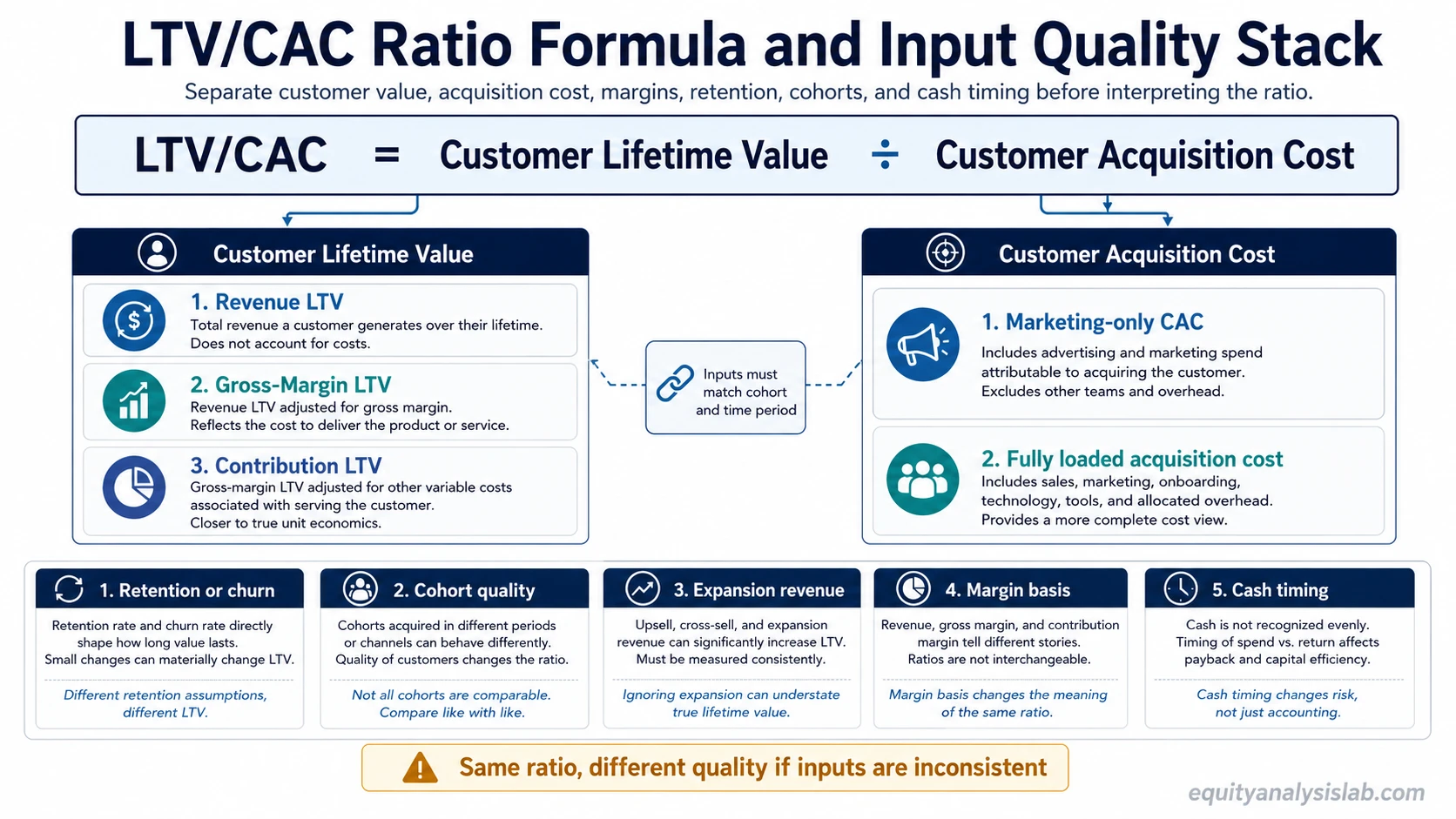

LTV/CAC Formula

The basic formula is:

LTV/CAC = Customer Lifetime Value ÷ Customer Acquisition Cost

If customer lifetime value is $3,000 and customer acquisition cost is $1,000, the LTV/CAC ratio is 3.0x. Under those assumptions, estimated customer value is three times the acquisition cost.

The calculation becomes less useful when the lifetime value estimate and the acquisition-cost estimate are not built on the same customer group, margin basis, or time period.

What Lifetime Value Means in the Numerator

The numerator is lifetime value, usually shortened to LTV. It estimates how much value a customer may generate over the expected customer relationship.

Revenue LTV measures expected customer revenue. Gross-margin LTV adjusts that revenue for direct costs. Contribution LTV goes further by considering variable costs needed to serve the customer. These versions are not interchangeable.

A revenue-based LTV can overstate customer economics when margins are thin, churn is high, or expansion revenue applies only to a small customer group.

What Customer Acquisition Cost Means in the Denominator

The denominator is customer acquisition cost, or CAC. It measures how much a company spends to acquire a customer.

A narrow CAC figure may include only paid marketing spend. A broader CAC figure may include sales salaries, commissions, software, agency fees, partner incentives, onboarding, and other costs required to turn prospects into paying customers.

For investor analysis, the denominator should match the customer group being evaluated. Blended CAC may help with a company-wide overview, but it can hide whether newer customers are becoming more expensive to acquire.

How to Calculate LTV/CAC

If a customer is expected to generate $3,000 of lifetime value and it costs $1,000 to acquire that customer, the calculation is:

LTV/CAC = $3,000 ÷ $1,000 = 3.0x

The 3.0x result means the estimated customer value is three times acquisition cost. The interpretation still depends on whether the LTV figure is based on revenue or margin, whether CAC includes the full acquisition cost base, and whether the same customer cohort is being measured.

How to Interpret LTV/CAC Without Universal Thresholds

A low LTV/CAC ratio can suggest that a company is spending heavily to acquire customers relative to expected customer value. It may also reflect early-stage investment, weak retention, low pricing power, or a temporary acquisition push.

A balanced ratio can suggest that acquisition spending and customer value are more aligned, but the cash profile still matters. The ratio may look acceptable while payback is slow, margins are weak, or newer cohorts are less profitable than older cohorts.

A very high LTV/CAC ratio is not automatically better. It can reflect strong customer economics, but it can also reflect underinvestment in growth, optimistic LTV assumptions, excluded acquisition costs, or a small mature customer base that is not representative of future growth.

LTV/CAC Input Quality and Comparability Checks

| Input or assumption | What it measures | What can distort interpretation |

|---|---|---|

| Revenue LTV | Expected customer revenue over the relationship | Can overstate economics when direct costs or service costs are high |

| Gross-margin LTV | Customer value after direct costs | Depends on accurate gross margin assumptions |

| Contribution LTV | Customer value after direct and variable service costs | May differ from revenue LTV when support, hosting, success, or implementation costs are material |

| CAC scope | Cost required to acquire a customer | Can be understated if sales labor, commissions, tools, partners, or onboarding are excluded |

| Retention and churn | How long customers stay and keep paying | Small changes in retention assumptions can materially change estimated LTV |

| Cohort | The customer group being measured | Older cohorts may look better than newer cohorts if acquisition costs are rising or retention is weakening |

| Time period | The period used for revenue, cost, and retention assumptions | Mixing periods can make the ratio look cleaner than the underlying economics |

| Expansion revenue | Additional revenue from existing customers | Can make LTV look stronger if expansion applies only to the best customer segments |

Why the Same LTV/CAC Ratio Can Mean Different Things

Two companies can report the same LTV/CAC ratio while having different customer economics. One may use margin-based LTV and full CAC. Another may use revenue LTV and exclude part of the sales cost base.

The same headline ratio can also hide cohort differences. A mature customer base with strong retention may support a high LTV estimate, while newer customers may be more expensive to acquire and less likely to renew.

That is why LTV/CAC should be read as an input-quality diagnostic, not as a standalone proof of company quality.

Common LTV/CAC Mistakes

- Treating one benchmark as universal: A ratio that looks healthy in one business model may be weak or unrealistic in another.

- Mixing revenue LTV with full-cost CAC: The numerator and denominator may not reflect the same economic basis.

- Ignoring margin quality: Strong revenue growth does not always create strong customer value if gross margin or contribution margin is weak.

- Using blended averages too casually: Company-wide averages can hide weaker recent cohorts.

- Forgetting cash timing: A high ratio can still be less attractive if acquisition cost is paid upfront and customer value arrives slowly.

How Investors Should Use LTV/CAC

LTV/CAC is most useful when it is connected to unit economics, retention, margin structure, acquisition efficiency, and cash generation. It can help show whether growth spending has a reasonable economic basis.

The ratio becomes weaker when it is used as a shortcut for valuation or business quality. A company can show attractive customer economics while still facing dilution, weak cash flow, slowing growth, poor capital allocation, or a valuation that already prices in optimistic assumptions.

The strongest use is comparative: check whether the same formula basis, CAC scope, cohort period, and margin definition are being used before comparing companies or periods.

Related Concepts

LTV/CAC connects customer value, acquisition cost, margin quality, retention, and unit economics. Lifetime value explains the numerator, customer acquisition cost explains the denominator, gross margin helps test the quality of the value estimate, and unit economics provides the broader business-model context.

LTV/CAC Ratio FAQ

What is the LTV/CAC ratio?

LTV/CAC ratio compares estimated customer lifetime value with customer acquisition cost. It shows how much customer value is estimated for each dollar spent to acquire a customer.

How do you calculate LTV/CAC?

Divide customer lifetime value by customer acquisition cost. If LTV is $3,000 and CAC is $1,000, the LTV/CAC ratio is 3.0x.

What is a good LTV/CAC ratio?

There is no universal good ratio. The interpretation depends on margin basis, CAC scope, retention assumptions, customer cohort, cash payback, and business model.

Is CAC/LTV the same as LTV/CAC?

No. LTV/CAC divides lifetime value by acquisition cost. CAC/LTV reverses the relationship and shows acquisition cost as a share of lifetime value.

Why can two companies with the same LTV/CAC ratio have different business quality?

The ratio can be the same even when the economics differ. Margin basis, CAC scope, churn, cohort mix, expansion revenue, cash payback, and accounting definitions can all change the quality of the same headline number.