SaaS customer acquisition cost measures the sales and marketing cost required to acquire a new paying SaaS customer over a defined period.

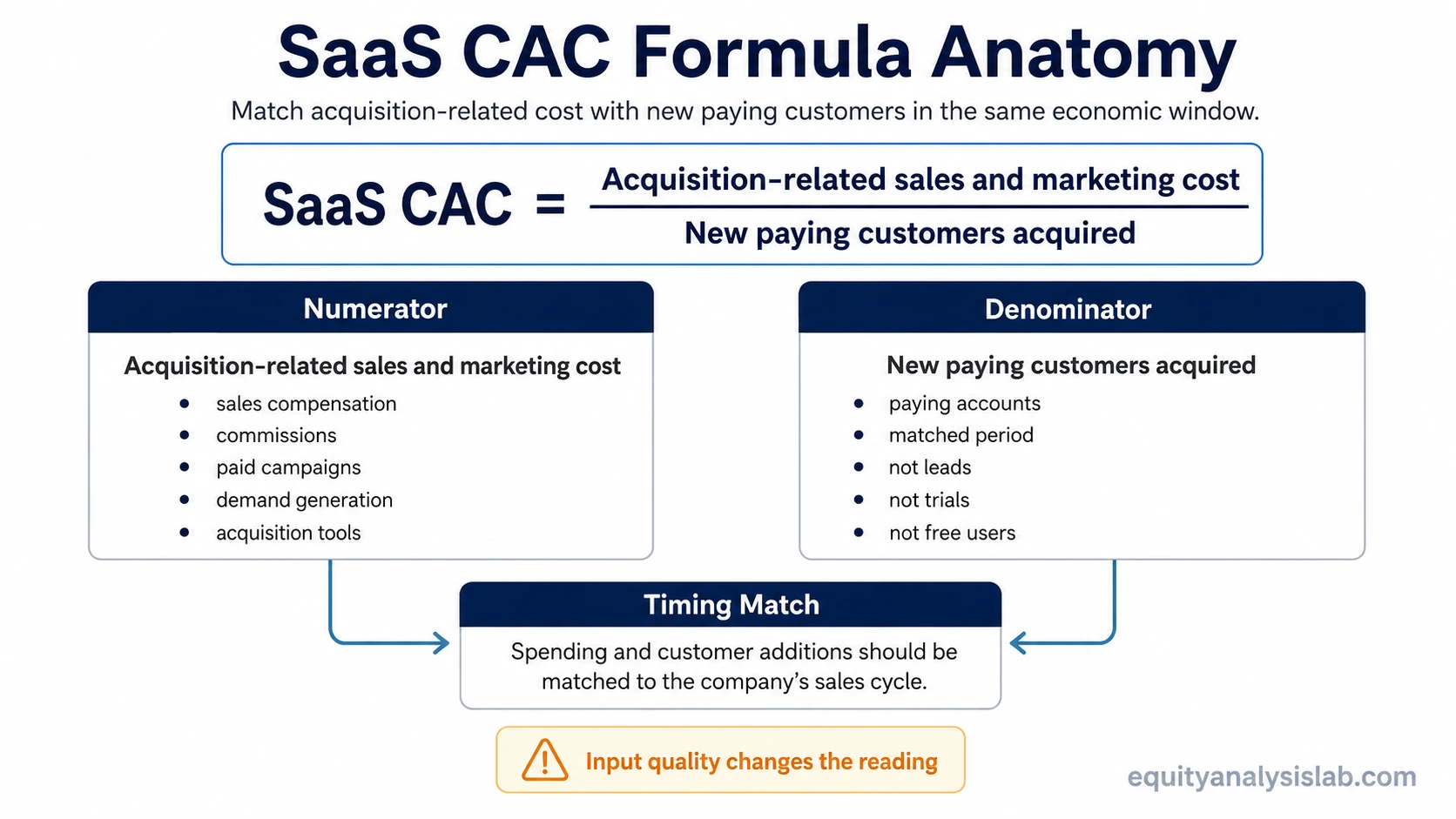

Definition: SaaS customer acquisition cost, often shortened to SaaS CAC, is calculated by dividing acquisition-related sales and marketing cost by the number of new paying customers acquired in the same matched period.

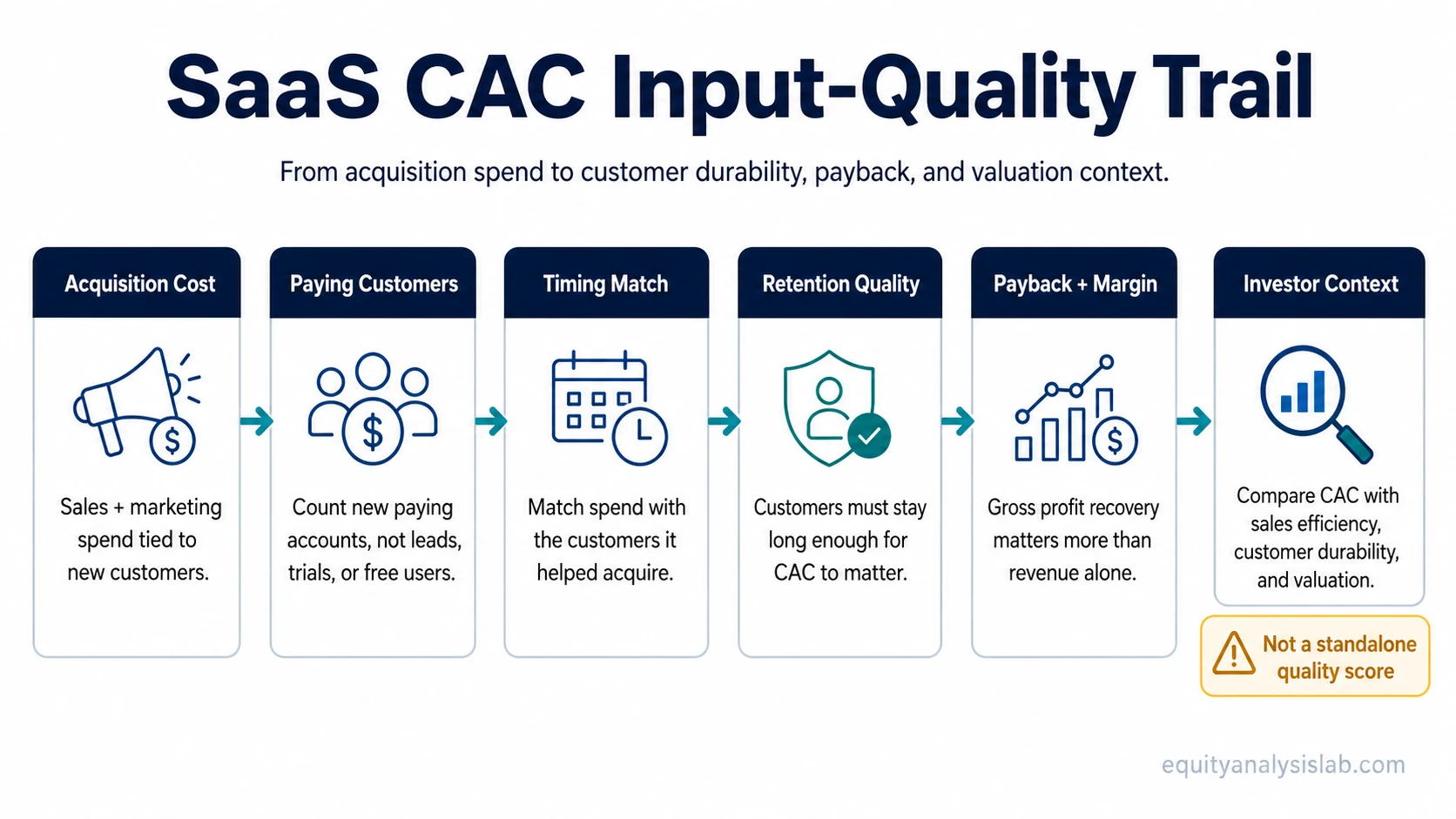

The metric matters because a SaaS company can report attractive recurring revenue growth while spending heavily to create that growth. A low or falling CAC can suggest improving acquisition efficiency, but it does not prove business quality by itself. The reading changes with retention, gross margin, payback time, customer segment, sales motion, and how consistently the company defines its inputs.

The basic formula is:

SaaS CAC = acquisition-related sales and marketing cost / new paying customers acquired in the same matched period

Key Points

- SaaS CAC is an acquisition-cost metric, not a standalone verdict on company quality.

- The numerator should focus on costs tied to acquiring customers, not every cost that happens to sit inside sales and marketing.

- The denominator should count new paying customers, not leads, free users, trials, demos, or marketing-qualified leads.

- Period matching is essential because B2B SaaS sales cycles can create a lag between spending and customer conversion.

- CAC becomes more useful when read with retention, gross margin, payback, churn, and sales efficiency context.

How to Calculate SaaS Customer Acquisition Cost

The cleanest version of SaaS CAC matches acquisition cost and customer additions over the same measurement window. If a company spends on sales and marketing during one quarter but those campaigns convert customers over the next two quarters, a simple same-quarter formula can overstate or understate true acquisition efficiency.

| Formula part | What it should include | Investor interpretation risk |

|---|---|---|

| Acquisition-related sales cost | Sales payroll, commissions, outbound sales support, sales tools, events, and other costs tied to winning new customers. | Including renewal or account-management costs can make new-customer acquisition look more expensive than it really is. |

| Acquisition-related marketing cost | Paid campaigns, content programs, demand generation, marketing software, agency spend, brand spend where it supports acquisition, and allocated marketing labor. | Broad brand or retention marketing can blur the metric if it is mixed with direct acquisition spend without disclosure. |

| New paying customers | Customers who became paying SaaS accounts during the matched period. | Counting trials, leads, free users, or demos makes CAC look artificially low. |

| Measurement period | A month, quarter, or year that matches spending with the customers that spending helped acquire. | Long enterprise sales cycles can make a short-period CAC number noisy. |

The calculation is useful only after the investor checks which customers were acquired, how long they stay, what gross margin they produce, and how quickly acquisition spend is recovered.

What Belongs in the CAC Numerator

The numerator should capture the cost of acquiring new paying customers. In SaaS, that usually includes sales compensation, sales commissions, marketing campaigns, acquisition tools, agencies, events, and allocated labor tied to new-customer generation.

Reported sales and marketing expense can serve more than one job. Some spending creates new customers. Some supports renewals. Some supports expansion inside existing accounts. Some builds long-term brand visibility. If those costs are combined without explanation, the CAC figure becomes harder to compare across companies.

Public companies may not disclose CAC in a standardized format, so investors often need to compare definitions, reporting periods, and sales-and-marketing classifications before relying on the figure.

Input-quality warning: A higher CAC is not automatically bad if the company is acquiring larger, stickier, higher-margin customers. A lower CAC is not automatically good if the customers churn quickly, expand poorly, or require heavy support after purchase.

What Belongs in the CAC Denominator

The denominator should count new paying customers acquired during the matched period. It should not count leads, website signups, free accounts, product-qualified users, demos, trials, or marketing-qualified leads unless the company clearly explains why those users represent paying customer acquisition.

This distinction is especially important for freemium and product-led SaaS models. A company may create many free users at low cost, but the investor still needs to know how many of those users become paying customers and whether the converted customers produce enough gross profit to justify the acquisition spend.

Common mistake: Treating user growth as customer acquisition can make CAC look better than the economics of the paying customer base. For investor analysis, the denominator has to connect to revenue-producing customers.

Why Period Matching Changes the Reading

SaaS CAC becomes less reliable when spending and customer additions are measured over mismatched periods. This is common in B2B SaaS because the sales process can run through prospecting, demo, procurement, security review, contract negotiation, onboarding, and eventual activation.

A quarter with heavy hiring or campaign investment may show weak CAC if the customers arrive later. A later quarter may show unusually strong CAC if customers convert from spending that happened earlier. One period should not be treated as a durable efficiency signal unless the pattern holds across several reporting periods and the company’s sales cycle supports the comparison.

New CAC vs Blended CAC

New CAC focuses on the cost of acquiring new customers. Blended CAC can mix new-customer acquisition, upsell, cross-sell, renewal support, and broader sales and marketing activity. Both can be useful, but they answer different questions.

| CAC view | What it answers | Where investors should be careful |

|---|---|---|

| New customer CAC | How much the company spends to acquire a new paying customer. | It can ignore expansion economics if existing customers later grow materially. |

| Blended CAC | How much sales and marketing spend supports customer growth across the business. | It can hide whether new-logo acquisition is becoming less efficient. |

| Segment-level CAC | How acquisition cost differs by customer type, channel, geography, or sales motion. | It may not be disclosed consistently enough for clean peer comparison. |

For a mature SaaS company, blended CAC may look reasonable because expansion from existing customers is efficient. For an earlier-stage company, new customer CAC may matter more because new-logo acquisition still drives the revenue base. The useful reading depends on the company’s stage and revenue mix.

How Investors Should Interpret SaaS CAC

SaaS CAC is most useful when it is read as part of an input-quality trail. The number starts with acquisition cost, then moves into retention, gross margin, payback, sales efficiency, and customer durability.

A company can spend heavily and still create value if acquired customers remain for many years, expand their subscriptions, and produce high gross profit. Another company can report a low CAC and still destroy value if customers churn quickly or require discounts, implementation support, and account-management effort that the CAC calculation does not fully capture.

The CAC payback period helps test how quickly acquisition spend is recovered through gross profit. SaaS churn rate helps test whether acquired customers remain long enough for the CAC to make economic sense. The SaaS Magic Number adds a sales and marketing efficiency lens by comparing revenue growth with prior sales and marketing spend.

When SaaS CAC Can Mislead

SaaS CAC can mislead when the formula is technically correct but the business context changes the meaning. The most common problem is treating CAC as a clean quality score instead of testing the inputs behind it.

| Misread | Why it matters | Better investor question |

|---|---|---|

| Low CAC means strong business quality | Low acquisition cost is less valuable if customers churn, downgrade, or fail to expand. | Do customers stay long enough and generate enough gross profit to justify the spend? |

| High CAC means poor acquisition efficiency | Enterprise SaaS can have high upfront acquisition cost but larger contracts and longer customer lives. | Is the company acquiring durable, high-value customers or overpaying for growth? |

| One quarter shows the true trend | Hiring, campaign timing, sales-cycle lag, and seasonality can distort short periods. | Does the pattern persist across enough periods to reflect real acquisition economics? |

| Peer CAC is directly comparable | Different sales motions, customer sizes, accounting choices, and disclosure quality can change the number. | Are the companies acquiring similar customers through similar channels? |

SaaS CAC and LTV:CAC

CAC shows acquisition cost. LTV:CAC compares the value of a customer relationship with the cost to acquire that customer. The distinction matters because CAC alone does not tell the investor whether the customer base is valuable enough to support the spending.

A company with a high CAC may still have attractive economics if customer lifetime value is high, gross margin is strong, churn is low, and expansion revenue is meaningful. A company with a low CAC may still have weak economics if customers leave quickly or require heavy discounting. The ratio between customer value and acquisition cost is the next layer, not a replacement for checking CAC input quality.

SaaS CAC, Rule of 40, and Valuation Quality

Investors often connect SaaS CAC to broader quality metrics because acquisition efficiency affects growth durability. A company that grows revenue through efficient customer acquisition may support stronger operating leverage over time. A company that needs ever-higher acquisition spend to maintain growth may face margin pressure even if headline revenue is still rising.

CAC focuses on the efficiency of acquired growth, while the Rule of 40 combines growth and profitability into a broader operating balance. The Rule of 40 can help frame the tradeoff between growth and profitability, but it should not turn CAC into a single quality verdict. CAC explains part of the growth input. Gross margin, retention, expansion, cash flow, dilution, and the price paid for the business still matter.

Investor use: SaaS CAC is strongest as a diagnostic input. It helps test whether growth is being acquired efficiently, but the investment conclusion depends on customer durability, margin structure, balance-sheet flexibility, and valuation.

Simple SaaS CAC Example

Example: A hypothetical SaaS company spends $1,200,000 on acquisition-related sales and marketing during a quarter. During the same matched period, it acquires 400 new paying customers. Its SaaS CAC is $3,000 per new paying customer.

Calculation: $1,200,000 / 400 = $3,000.

The number is only the starting point. If those customers have high gross margin, low churn, and strong expansion potential, the $3,000 CAC may be reasonable. If customers churn quickly or require heavy support, the same $3,000 CAC may be a warning sign.

Practical Reading Checklist

Before relying on a SaaS CAC number, test the inputs and the surrounding business model.

- Cost boundary: Does the numerator include only acquisition-related sales and marketing cost, or does it mix renewal and expansion activity?

- Customer boundary: Does the denominator count new paying customers rather than leads, trials, free users, or demos?

- Timing boundary: Does the measurement period match spending with the customers that spending helped acquire?

- Retention boundary: Do customers remain long enough for acquisition spend to make sense?

- Margin boundary: Does gross profit, not just revenue, support the payback logic?

- Valuation boundary: Is the market paying for growth that depends on rising acquisition spend?

FAQ

Is a lower SaaS CAC always better?

No. A lower SaaS CAC can be attractive, but only if customers stay, pay enough, expand over time, and generate enough gross profit. A low CAC with weak retention can still be poor business quality.

Why does SaaS CAC need retention context?

Retention determines whether the company has enough time to recover acquisition spend and earn profit from the customer relationship. CAC without retention can make growth look efficient even when customers leave too quickly.