CAC payback period measures how many months a SaaS company needs to recover customer acquisition cost through gross-margin-adjusted recurring revenue.

A shorter payback period points to faster recovery of acquisition spend, but the durability of that recovery depends on the customer base behind it. Retention quality, gross margin, customer segment, billing model, and sales-cycle length can all change the meaning of the same payback number.

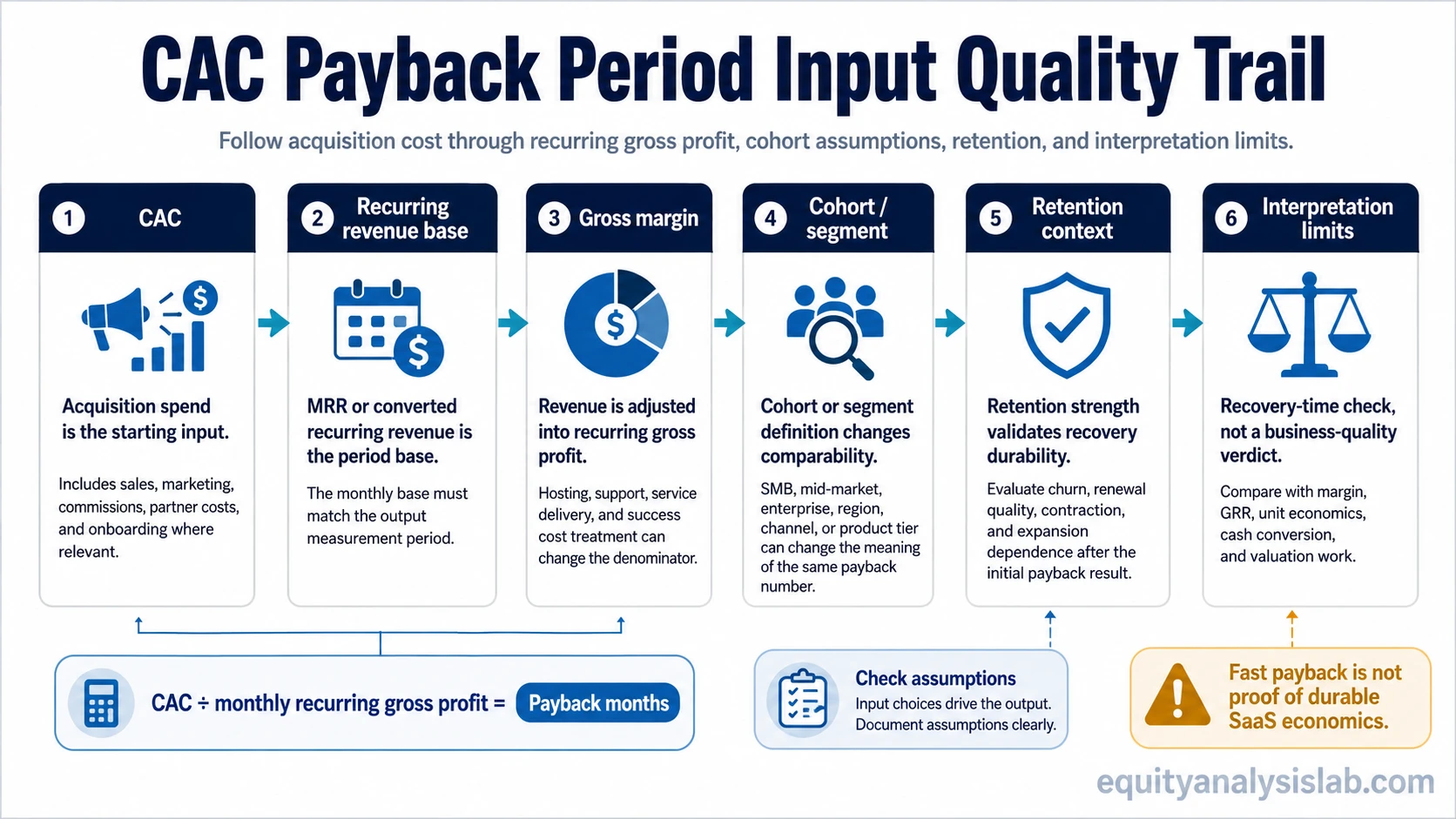

Definition: CAC payback period is a SaaS metric that estimates the time required to recover the cost of acquiring a customer from the gross profit generated by that customer or cohort.

Key Points

- CAC payback period connects acquisition cost to gross-margin-adjusted recurring revenue.

- The formula depends on CAC allocation, revenue base, margin assumption, and cohort definition.

- Benchmarks need context because customer segment, contract value, billing terms, and sales motion can vary widely.

- A fast payback period can support cash recovery, but business quality still depends on retention, expansion, margin durability, and cash conversion.

CAC Payback Period Formula

The common CAC payback period formula divides customer acquisition cost by the monthly gross profit generated by the acquired customer or cohort.

Formula: CAC payback period = Customer acquisition cost ÷ monthly recurring revenue gross profit.

Expanded form: CAC payback period = CAC ÷ (monthly recurring revenue × gross margin).

The numerator should reflect the relevant acquisition cost. In many SaaS analyses, that includes relevant sales and marketing acquisition costs tied to the customer or cohort being measured. A separate SaaS customer acquisition cost analysis is useful when the CAC number mixes channels, sales teams, partner costs, or one-time campaigns.

The denominator should reflect recurring gross profit, not just headline revenue. If revenue is measured using monthly recurring revenue, the output is usually stated in months. If an annual revenue base is used, the calculation must be converted consistently before comparison.

Formula Inputs That Change the Reading

Two companies can report the same CAC payback period while using different assumptions. Input quality matters because the metric is a recovery-time lens, not a business-quality verdict.

| Input | What to check | Why it changes interpretation |

|---|---|---|

| CAC allocation | Sales, marketing, commissions, onboarding, partner costs, and timing of spend | Understated acquisition cost can make payback look faster than the economics support. |

| Recurring revenue base | MRR, ARR conversion, ARPA, or cohort revenue | Monthly and annual bases must be converted consistently before comparing companies. |

| Gross margin | Revenue after cost of service delivery, hosting, support, and customer success where relevant | Revenue without gross margin adjustment can overstate the cash recovered from each customer. |

| Cohort or segment | SMB, mid-market, enterprise, channel, region, or product tier | Different segments can have different ACV, sales cycles, churn, and payback timing. |

| Billing model | Monthly billing, annual prepayment, discounts, implementation fees, and contract terms | Cash collection timing can differ from revenue recognition and reported recurring revenue. |

| Retention context | Churn, contraction, renewal quality, and expansion dependence | Fast payback is less useful if the customer base does not remain durable after acquisition. |

Simple CAC Payback Period Example

Illustrative example: A SaaS company spends $1,200 to acquire one customer. That customer pays $200 in monthly recurring revenue, and the product has a 75% gross margin.

Monthly recurring gross profit equals $200 × 75%, or $150. CAC payback period equals $1,200 ÷ $150, or 8 months.

The 8-month result means the company recovers the acquisition cost through gross profit in roughly eight months under those assumptions. The number changes if CAC excludes commissions, if gross margin is lower, if onboarding costs are material, or if the customer churns before enough gross profit is earned.

When revenue is framed through annual recurring revenue, the calculation still needs a monthly gross-profit base if the output is expressed in months. Annualized revenue can make the metric easier to compare at a high level, but the payback calculation depends on the period used in the denominator.

What a Short or Long Payback Period Can Mean

A short CAC payback period points to faster recovery of acquisition spend. That can give a SaaS company more flexibility to reinvest because less cash is tied up for long periods before customer gross profit repays the initial acquisition cost.

Benchmark ranges are most useful when the comparison group has similar customer segments, contract values, gross margins, billing terms, and sales-cycle length.

A long CAC payback period may reflect a heavier acquisition model, slower sales cycles, weaker gross-margin economics, lower revenue per customer, or an enterprise motion where larger contracts require more upfront selling effort. Long payback is not automatically poor, but it increases the burden on retention, expansion, cash reserves, and sales execution.

Investor-use boundary: CAC payback period is most useful as a recovery-time check. It does not replace margin analysis, retention analysis, unit economics, free cash flow, or valuation work.

Where CAC Payback Period Can Mislead

CAC payback period can look clean while the underlying economics remain weak. The most common problem is a formula that treats early revenue as durable without checking how long customers stay, whether they expand, and how much service cost is needed to keep them.

Limitation: A fast payback period can still mislead when churn is high, gross margin is overstated, customer success cost is excluded, or new customers come from a segment with weaker renewal behavior.

Retention quality is especially important. Gross revenue retention helps separate acquisition recovery from the durability of the recurring revenue base before expansion revenue is added.

| Issue | How the metric can look better than reality | What to compare next |

|---|---|---|

| Unburdened CAC | Sales commissions, partner costs, or onboarding costs are excluded. | Fully loaded CAC by channel or cohort. |

| Weak retention | Customers recover CAC quickly but leave before long-term value builds. | GRR, churn, renewal rates, and cohort behavior. |

| Expansion dependence | Base revenue does not recover CAC unless later upsell is assumed. | Base retention versus expansion-driven net retention. |

| Segment mix shift | Blended payback hides weak economics in one customer segment. | Payback by SMB, mid-market, enterprise, region, or product tier. |

| Billing timing | Annual prepayment improves cash timing, while revenue economics may be different. | Cash collection, revenue recognition, and deferred revenue movement. |

| Sales rep ramp | Recent hiring can make CAC appear temporarily inefficient or temporarily undercounted. | Sales capacity, quota productivity, and cohort maturity. |

CAC Payback Period vs Related SaaS Metrics

CAC payback period overlaps with several SaaS metrics, but it answers a narrower question: how long acquisition cost takes to return through recurring gross profit.

| Metric | Main question | How it differs from CAC payback period |

|---|---|---|

| CAC payback period | How long does acquisition cost take to recover? | Focuses on recovery time through recurring gross profit. |

| Customer acquisition cost | How much does it cost to acquire a customer? | Measures the cost input, not the recovery period. |

| ARR | How large is the annualized recurring revenue base? | Measures recurring revenue scale, not acquisition cost recovery. |

| GRR | How much recurring revenue remains before expansion? | Measures revenue durability, not payback timing. |

| LTV:CAC ratio | How does estimated lifetime value compare with acquisition cost? | LTV:CAC ratio compares value to cost over a longer expected customer life, while CAC payback period focuses on time to recover CAC. |

| SaaS Magic Number | How efficiently does sales and marketing spend translate into recurring revenue growth? | Looks at growth efficiency from spend, not direct payback months for a customer or cohort. |

Common Mistakes When Comparing Companies

Comparable CAC payback analysis requires more than placing two reported numbers side by side. The same headline result can mean different things when companies sell to different customer segments, use different gross-margin methods, or recognize revenue under different contract structures.

Common mistake: Treating a single benchmark as universal can flatten the economics of very different SaaS models. A self-serve product, a sales-assisted mid-market product, and an enterprise platform may have different CAC intensity, sales cycles, implementation work, retention profiles, and contract sizes.

| Comparison area | Question to ask | Why it matters |

|---|---|---|

| Customer segment | Are the companies selling to similar customer types? | Enterprise sales may require more upfront spend but can also involve larger contracts. |

| ACV | Is average contract value similar? | Higher ACV may support longer payback when retention and expansion remain strong. |

| Sales cycle | How long does the selling process take? | Long sales cycles can delay cash recovery and distort period comparisons. |

| Gross margin method | Are support, hosting, and success costs treated consistently? | Different margin definitions change the denominator. |

| Cohort maturity | Are new and mature cohorts being compared? | Young cohorts may not yet reveal churn, expansion, or full payback behavior. |

| Cash collection | Does billing create upfront cash before revenue is recognized? | Cash timing can make the funding burden different from accounting revenue. |

FAQ

Is a shorter CAC payback period always better?

A shorter payback period can support faster cash recovery, but it is not better by itself. Retention, gross margin, customer quality, sales motion, and long-term cash conversion still matter.

Why does gross margin matter in CAC payback period?

Gross margin matters because revenue is not the same as recovered acquisition cost. The metric should use the gross profit available after the cost of delivering the product or service.