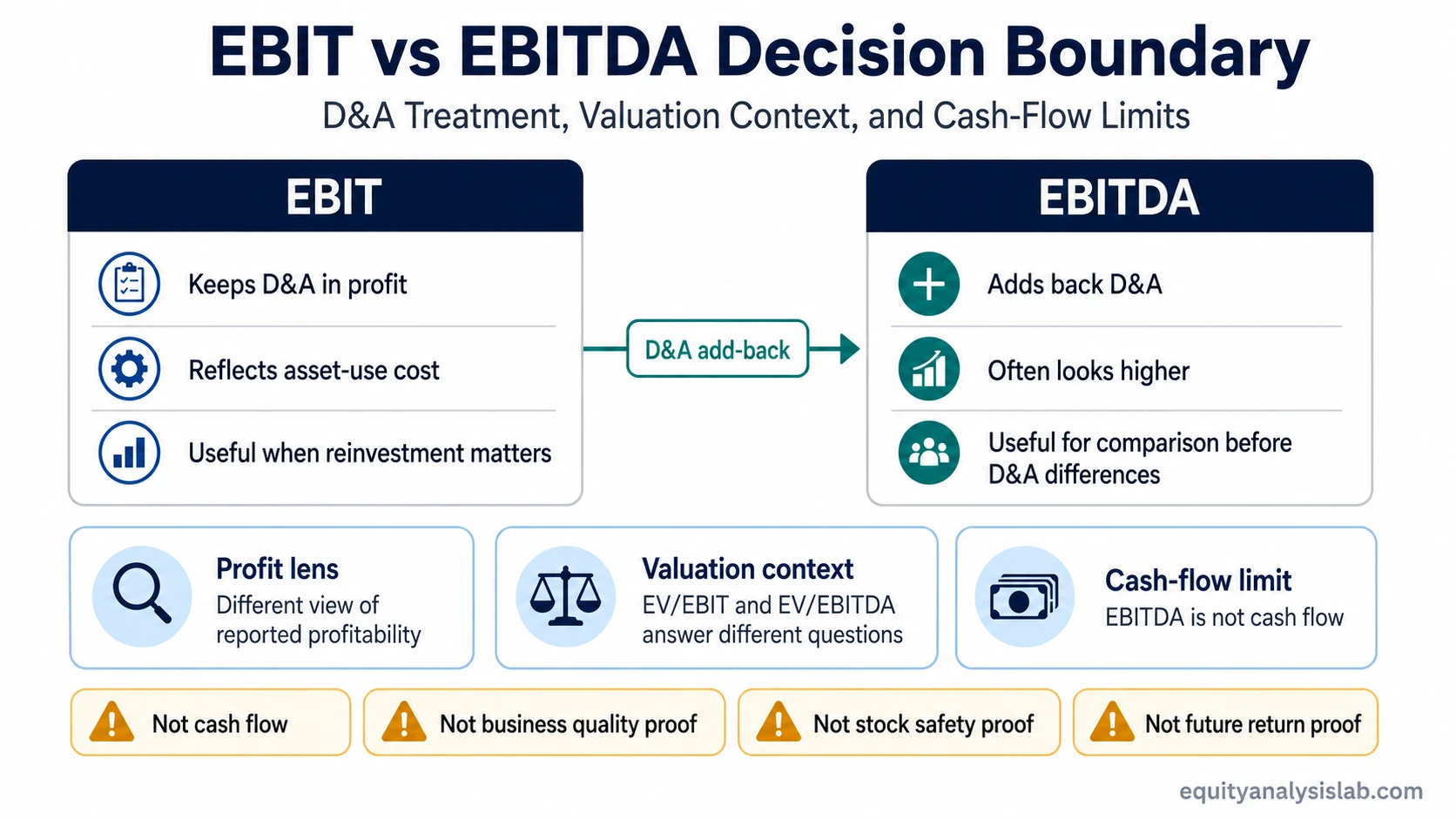

EBIT vs EBITDA compares two profitability measures that treat depreciation and amortization differently. EBIT keeps those costs in the profit picture, while EBITDA adds them back, so EBITDA can look stronger without proving better cash generation, business quality, or stock value.

EBIT means earnings before interest and taxes. EBITDA means earnings before interest, taxes, depreciation, and amortization. The difference is not cosmetic. It changes the question an investor is asking: EBIT is closer to operating profit after the cost of using long-lived assets, while EBITDA removes depreciation and amortization to compare earnings before those non-cash charges.

Key Points

- EBIT includes the effect of depreciation and amortization; EBITDA adds those charges back.

- EBITDA is usually higher than EBIT, but higher does not automatically mean better.

- EBIT can be more useful when asset intensity, reinvestment needs, and depreciation matter.

- EBITDA can help compare companies before D&A differences, but it is not the same as cash flow.

What EBIT Measures

EBIT measures profit before interest and taxes, while still reflecting operating expenses and the effect of depreciation and amortization. It is often used to look at operating profitability before financing structure and tax differences affect the result.

Definition: EBIT is earnings before interest and taxes. It can be viewed as operating profit before financing and tax effects, but after depreciation and amortization have affected reported profit.

Because depreciation and amortization remain inside EBIT, the metric can be more sensitive to asset-heavy business models. A company that needs factories, fleets, equipment, or capitalized software may report lower EBIT than EBITDA because the cost of those assets flows through depreciation or amortization over time.

What EBITDA Measures

EBITDA starts with earnings before interest and taxes, then adds back depreciation and amortization. The result shows profit before financing, taxes, and the accounting charges tied to long-lived assets and intangible assets.

Definition: EBITDA is earnings before interest, taxes, depreciation, and amortization. A common formula is EBITDA = EBIT + depreciation + amortization.

This can be useful when comparing companies with different depreciation schedules, acquisition histories, or asset bases. The limitation is that the add-back does not remove the economic need to maintain or replace assets. EBITDA can make a company look more profitable than EBIT even when the business still requires heavy reinvestment.

Companies often present adjusted EBITDA as a non-GAAP measure when they add back items beyond depreciation and amortization. Those adjustments can improve comparability in some cases, but they can also make the metric less conservative if recurring costs are excluded too aggressively.

EBIT vs EBITDA Comparison Table

| Comparison point | EBIT | EBITDA |

|---|---|---|

| Full meaning | Earnings before interest and taxes. | Earnings before interest, taxes, depreciation, and amortization. |

| D&A treatment | Depreciation and amortization remain reflected in profit. | Depreciation and amortization are added back. |

| Profitability lens | Shows operating profit after the accounting cost of long-lived assets. | Shows earnings before the D&A burden is applied. |

| Capital intensity sensitivity | More sensitive to asset-heavy business models. | Can flatter companies with large depreciation or amortization charges. |

| Valuation use | Often used when asset costs and reinvestment intensity are central to the analysis. | Often used for broader cross-company comparison before D&A differences. |

| Cash-flow limitation | Still not free cash flow because it excludes interest, taxes, working capital, and CapEx timing. | Not cash flow because it ignores CapEx, working capital, leverage, and other cash demands. |

| Risk if misread | Can be treated as a complete profitability answer when financing and taxes still matter. | Can create false comfort by making earnings look stronger than cash economics justify. |

EBIT vs EBITDA Formula Difference

The formula difference is mainly the D&A add-back. EBIT can be reached from operating income in many presentations, or from net income by adding back interest and taxes. EBITDA then adds depreciation and amortization to EBIT.

| Metric | Formula path |

|---|---|

| EBIT | Net income + interest + taxes, or operating income when the presentation already aligns with EBIT. |

| EBITDA | EBIT + depreciation + amortization. |

The inputs usually come from the statement where revenue, expenses, and reported profit are organized, with depreciation and amortization sometimes disclosed in the cash flow statement or notes depending on the company’s reporting format.

Same Company, Different Investor Question

A single company can look different depending on whether the investor focuses on EBIT or EBITDA. Assume a hypothetical industrial company reports $100 million of revenue, $25 million of EBIT, and $12 million of depreciation and amortization.

| Hypothetical item | Amount | Interpretation |

|---|---|---|

| Revenue | $100 million | Top-line sales before expenses. |

| EBIT | $25 million | Profit after operating costs and D&A impact, before interest and taxes. |

| Depreciation and amortization | $12 million | Non-cash accounting charges linked to asset use or acquired intangibles. |

| EBITDA | $37 million | EBIT plus the D&A add-back. |

The company looks more profitable on EBITDA because EBITDA removes the $12 million D&A charge. That does not mean the company is automatically better. The EBIT question is closer to: how much profit remains after the accounting cost of assets? The EBITDA question is closer to: how much earnings power appears before those accounting charges?

Example interpretation: If the company must keep spending heavily to maintain plants and equipment, the EBITDA number may overstate the comfort an investor should take from the business. If D&A mainly reflects old acquisition accounting and current reinvestment needs are modest, EBITDA may help normalize comparison across companies. The metric is useful only after the underlying business question is clear.

When Investors Use EBIT vs EBITDA

Investors often use EBIT when they want a profit measure that still reflects depreciation and amortization. This is especially relevant when comparing companies where asset wear, reinvestment needs, or operating margin quality matter. The related valuation multiple is EV/EBIT, which compares enterprise value with earnings before interest and taxes.

EBITDA is more useful when the goal is to compare companies before D&A differences affect reported profit. This can be useful across companies with different asset ages, accounting histories, or acquisition profiles. The related valuation multiple is enterprise value to EBITDA, which compares enterprise value with earnings before interest, taxes, depreciation, and amortization.

Decision boundary: EBIT is usually more conservative when depreciation and amortization represent real economic asset use. EBITDA can be useful for comparability, but it becomes risky when it is treated as proof of cash generation or business quality.

EBITDA Limitations and False Comfort

EBITDA is not cash flow. It excludes several cash pressures that can matter to investors, including capital expenditures, working capital needs, interest burden, taxes, lease obligations, and debt maturity risk. A company can report strong EBITDA and still convert little of that figure into free cash flow.

Limitation: EBITDA can create false comfort when the business is capital intensive, highly leveraged, or dependent on recurring reinvestment. The add-back removes depreciation and amortization from the metric, but it does not remove the economic reality that assets may need to be maintained, replaced, or upgraded.

The same caution applies to adjusted EBITDA. Removing unusual items can make a comparison cleaner when the adjustment is genuinely non-recurring. But if similar charges appear repeatedly, the adjustment may hide normal business costs rather than clarify performance.

Strong EBITDA also does not prove customer retention, recurring revenue quality, stock safety, or future return. It is one profitability lens. It becomes more useful when combined with cash conversion, reinvestment needs, debt load, margin durability, and the valuation multiple being applied.

EBIT vs EBITDA vs EBITA

EBITA sits between EBIT and EBITDA. EBITA means earnings before interest, taxes, and amortization. It adds back amortization but not depreciation. That can matter when amortization from acquired intangible assets is large, but depreciation from physical assets should still remain visible.

For the main EBIT vs EBITDA distinction, the most important boundary remains simple: EBIT keeps depreciation and amortization in the profit picture, while EBITDA adds both back.

FAQ

What is the main difference between EBIT and EBITDA?

The main difference is depreciation and amortization. EBIT includes the effect of depreciation and amortization, while EBITDA adds those charges back.

Is EBITDA always better than EBIT?

No. EBITDA is usually higher, but that does not make it better. EBIT may be more useful when asset intensity, depreciation, and reinvestment needs are important to the company analysis.

Is EBITDA the same as cash flow?

No. EBITDA is not cash flow. It excludes capital expenditures, working capital changes, interest, taxes, and other cash demands that can materially affect what the business actually produces for investors.

When should investors use EV/EBIT instead of EV/EBITDA?

EV/EBIT can be more useful when depreciation and amortization reflect meaningful economic costs. EV/EBITDA can be useful for comparison before D&A differences, but it can be misleading when reinvestment needs are high.