EV/EBITDA is not proof that a stock is cheap or expensive. It is a valuation multiple that compares enterprise value with EBITDA, so its meaning depends on the company’s debt, cash, EBITDA quality, capital intensity, peer group, and business cycle position.

Direct answer: EV/EBITDA means enterprise value divided by EBITDA. It shows how much the market is assigning to the whole operating business relative to a proxy for operating earnings before interest, taxes, depreciation, and amortization.

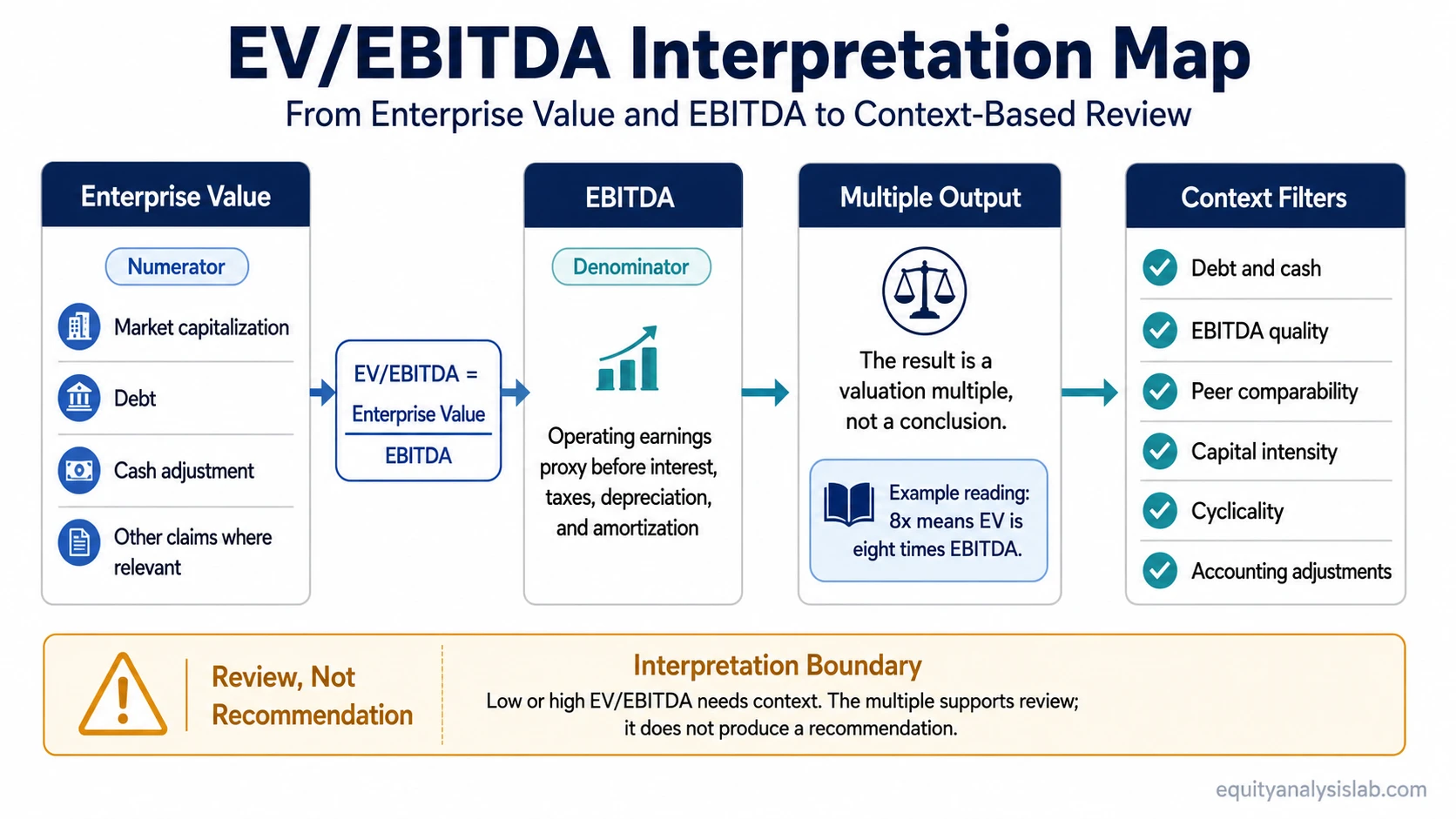

Formula: EV/EBITDA = Enterprise Value / EBITDA.

Key Points

- EV/EBITDA compares the value of the whole business with EBITDA, not just the equity market capitalization with net income.

- The multiple is most useful when comparing companies with similar business models, accounting profiles, capital intensity, and cycle exposure.

- EBITDA is an operating earnings proxy, not free cash flow, because it excludes items such as capital expenditure and working-capital needs.

- A low or high EV/EBITDA multiple needs context. Debt, cash, add-backs, cyclicality, peer selection, and business quality can all change the interpretation.

What EV/EBITDA Means

EV/EBITDA compares enterprise value with EBITDA. Enterprise value is a debt-inclusive and cash-adjusted view of what the operating business is worth to all capital providers. EBITDA is a pre-interest, pre-tax operating earnings proxy that removes depreciation and amortization from the denominator.

The result is a multiple. A company trading at 8x EV/EBITDA is being valued at eight times its EBITDA, using enterprise value rather than equity value alone. That can make the ratio useful when two companies have different debt levels, cash balances, or capital structures.

The ratio does not remove all differences between companies. It only gives a cleaner starting point than equity-only valuation in some situations. A company with better margins, steadier demand, lower reinvestment needs, and more durable EBITDA may deserve a different multiple than a company with weaker earnings quality or heavier capital requirements.

EV/EBITDA Formula

EV/EBITDA = Enterprise Value / EBITDA

Enterprise value, simplified: market capitalization + debt – cash and cash equivalents.

Enterprise value, fuller review: market capitalization + debt + preferred equity + minority interest and other relevant claims – cash and cash equivalents.

| Formula part | What it represents | Interpretation risk |

|---|---|---|

| Enterprise value | The value of the operating business to equity and debt holders, usually adjusted for cash and debt. | Debt, cash, preferred equity, minority interest, and other claims can change the numerator. |

| EBITDA | Earnings before interest, taxes, depreciation, and amortization. | EBITDA can overstate economic earnings when capital expenditure, working capital, or aggressive add-backs are material. |

| EV/EBITDA multiple | The number of times enterprise value covers EBITDA. | The number is not meaningful without peer context, EBITDA quality, and business-cycle context. |

A simplified enterprise value calculation is often expressed as market capitalization plus debt minus cash. In more complete analysis, preferred equity, minority interest, leases, pension obligations, or other claims may also matter. The exact inputs should match the purpose of the comparison.

What EV/EBITDA Tells Investors

EV/EBITDA helps investors compare how the market values operating earnings across companies. Because enterprise value includes debt and adjusts for cash, the ratio can be more useful than equity-only metrics when companies have different financing structures.

The multiple is often used in relative valuation. An investor might compare several companies in the same sector, then ask whether one business has a lower or higher EV/EBITDA multiple because of growth, margins, leverage, capital intensity, cyclicality, or earnings quality.

The useful question is not simply whether the number is low or high. The better question is what the multiple is assuming about the durability of EBITDA, the quality of the business, the balance sheet, and the peer group being used.

Simple hypothetical example: Company A has an enterprise value of 4 billion and EBITDA of 500 million. Its EV/EBITDA multiple is 8x. Company B has the same EBITDA but a higher enterprise value because it carries more net debt or has a higher equity market value before net debt adjustments. Company B’s multiple would be higher even before asking whether its EBITDA is more durable, less capital intensive, or more cyclical.

EV/EBITDA Assumption Stack

EV/EBITDA is only as useful as the assumptions behind the numerator, the denominator, and the comparison set. The multiple can look precise while hiding very different business realities.

| Assumption layer | What to check | Why it changes interpretation |

|---|---|---|

| Enterprise value inputs | Debt, cash, preferred equity, minority interest, leases, and other claims. | The numerator can rise or fall even when the equity price has not changed much. |

| EBITDA quality | Recurring earnings, add-backs, margins, accounting adjustments, and one-off items. | A larger denominator can make the multiple look lower while overstating recurring operating earnings. |

| Capital intensity | Maintenance capex, depreciation pattern, asset age, and reinvestment needs. | EBITDA ignores capex, so capital-heavy businesses can look stronger than their cash economics suggest. |

| Cyclicality | Whether EBITDA is near a peak, trough, or normalized level. | Peak EBITDA can make the multiple look low, while trough EBITDA can make it look high. |

| Peer comparability | Business model, geography, margin profile, growth rate, leverage, and accounting treatment. | A multiple is more useful when compared against similar companies rather than unrelated businesses. |

| Growth and business quality | Revenue durability, pricing power, competitive position, and margin stability. | Higher-quality or faster-growing businesses may trade at different multiples for reasons that are not visible in the formula alone. |

When EV/EBITDA Is Useful

EV/EBITDA is most useful when the analyst is comparing businesses with similar operating models and reasonably positive EBITDA. It can help separate operating valuation from capital structure because enterprise value includes debt and adjusts for cash.

The ratio can be especially useful in peer comparison when net income is affected by interest expense, tax differences, or depreciation and amortization patterns. In that setting, EV/EBITDA can create a cleaner operating comparison than a metric based only on earnings available to common shareholders.

That does not make EV/EBITDA universally better than other multiples. If depreciation and amortization are economically important, EV/EBIT can give a stricter view because it keeps depreciation and amortization in the profit measure. If EBITDA is weak, negative, or unstable, an EV/Revenue multiple may sometimes be more useful as a rougher revenue-based comparison.

When EV/EBITDA Can Mislead

EV/EBITDA can mislead when the denominator does not reflect durable operating economics. EBITDA excludes capital expenditure, working-capital needs, interest, taxes, depreciation, and amortization, so it should not be treated as the same thing as free cash flow.

Common mistake: A low EV/EBITDA multiple can reflect risk rather than opportunity. It may point to leverage, weak EBITDA quality, heavy reinvestment needs, declining demand, cyclicality, or a peer group mismatch.

The ratio is also less useful when EBITDA is negative, highly cyclical, or heavily adjusted. For financial companies, enterprise value and EBITDA may not map cleanly to the economics of the business because debt can function more like operating capital than ordinary financing.

Adjusted EBITDA requires particular care. Add-backs can be reasonable when they remove genuine one-time items, but they can also make recurring earnings look stronger than they are. The more adjustments are needed to make EBITDA usable, the more the multiple depends on judgment rather than a simple formula.

EV/EBITDA Sensitivity Mini-Table

The same EV/EBITDA number can carry different meanings when the inputs change. A sensitivity check helps prevent the ratio from becoming a shortcut.

| Change in input or context | What happens to EV/EBITDA | Why interpretation changes |

|---|---|---|

| Higher debt, same EBITDA | The multiple rises. | Enterprise value increases even if the equity price is unchanged. |

| Higher cash, same EBITDA | The multiple falls. | Cash reduces enterprise value when it is subtracted from the numerator. |

| Aggressive EBITDA add-backs | The multiple may look lower. | The denominator may overstate recurring operating earnings. |

| Heavy maintenance capex | The multiple may look more attractive than cash economics justify. | EBITDA excludes capital expenditure needed to sustain the business. |

| Peak-cycle EBITDA | The multiple may appear low. | The denominator may be temporarily inflated by favorable cycle conditions. |

| Stronger growth or business quality | The company may trade at a higher multiple. | The market may assign more value to durability, reinvestment prospects, or pricing power. |

What Is a Good EV/EBITDA Ratio?

There is no universal good EV/EBITDA ratio. A reasonable multiple depends on the industry, peer group, leverage, cash balance, growth profile, margin durability, accounting quality, and capital intensity of the business being compared.

A lower multiple can look attractive only if EBITDA is durable, the balance sheet is manageable, and the business is not facing structural deterioration. A higher multiple can be reasonable if the company has stronger growth, more stable margins, better cash conversion, or lower business risk than peers.

Growth context should not replace the core EV/EBITDA analysis, but it can help explain why two companies with similar current EBITDA may trade differently. A separate growth-adjusted earnings lens can be useful when the main question is whether earnings growth changes the interpretation of an earnings multiple.

EV/EBITDA vs P/E

EV/EBITDA and P/E answer different valuation questions. EV/EBITDA compares the value of the whole business with an operating earnings proxy. P/E compares equity market value with earnings available to common shareholders.

Useful boundary: EV/EBITDA is usually more focused on enterprise value and operating earnings before financing effects. P/E is more focused on equity value and net income after interest, taxes, depreciation, amortization, and other below-operating-line items.

Neither ratio is automatically superior. EV/EBITDA may be more useful for capital-structure comparison, while P/E may be more useful when the focus is common-shareholder earnings. Both can mislead when used without business quality, accounting, balance-sheet, and peer context.

How to Read EV/EBITDA Without Turning It Into a Shortcut

A useful EV/EBITDA review starts with the formula, but it does not stop there. The analyst needs to ask whether enterprise value is measured consistently, whether EBITDA is recurring, whether the peer group is comparable, and whether the business requires heavy reinvestment to maintain earnings.

The ratio is strongest as a comparison tool, not as a standalone verdict. It can help identify valuation differences worth investigating, but the explanation usually comes from the assumptions behind the multiple rather than the number alone.

Interpretation rule: Treat EV/EBITDA as an assumption check. The multiple becomes more useful when enterprise value inputs are clean, EBITDA is durable, capital intensity is understood, and peers are genuinely comparable.

FAQ

What does EV/EBITDA mean?

EV/EBITDA means enterprise value divided by EBITDA. It compares the value of the whole operating business with earnings before interest, taxes, depreciation, and amortization.

What does EV/EBITDA tell investors?

EV/EBITDA can show how the market values operating earnings relative to enterprise value. It is most useful for peer comparison when companies have similar business models and comparable EBITDA quality.

Is a lower EV/EBITDA always better?

No. A lower EV/EBITDA multiple can reflect business risk, leverage, weak EBITDA quality, heavy capital expenditure, cyclical peak earnings, or poor peer comparability.

When is EV/EBITDA misleading?

EV/EBITDA can be misleading when EBITDA is negative, highly adjusted, cyclical, or not supported by cash generation. It can also mislead for capital-intensive or financial businesses where EBITDA does not capture the main economic drivers.

How is EV/EBITDA different from P/E?

EV/EBITDA compares enterprise value with an operating earnings proxy. P/E compares equity market value with net income available to common shareholders.