Free cash flow to the firm is not cash available only to common shareholders. It is a firm-level cash-flow measure that estimates cash available to all capital providers after operating needs, taxes, and reinvestment are considered. In valuation work, FCFF is usually matched with firm value or enterprise value logic, not direct shareholder cash flow. It is an analytical input, not proof that a company is safe, high quality, or likely to produce a future return.

Free cash flow to the firm, or FCFF, measures cash flow available to both debt and equity capital providers after the business funds operations and reinvestment needs. It is often called unlevered free cash flow because it looks at cash flow before separating the effects of debt financing from the value of the operating business.

What Free Cash Flow to the Firm Means

Free cash flow to the firm starts from the operating business rather than from the shareholder claim. That makes it different from broad free cash flow discussions that may focus more generally on cash left after capital spending.

The firm-level lens matters because the operating business is financed by more than common equity. Lenders, bondholders, preferred holders, and common shareholders can all have claims on the value created by the business. FCFF tries to measure the cash flow available to that full capital-provider base before deciding how value is split between them.

A positive FCFF number can indicate that a business produced operating cash after reinvestment needs. A negative FCFF number can appear when reinvestment, working-capital requirements, or weak operating results consume cash. Neither number is automatically good or bad without context.

Key points:

- FCFF is a firm-level cash-flow measure, not an equity-holder-only cash-flow measure.

- The common formula is NOPAT plus depreciation and amortization, minus capital expenditures and the increase in net working capital.

- FCFF is normally connected to firm value or enterprise value, not direct equity value.

- Working-capital timing, capital expenditure classification, and non-recurring items can distort interpretation.

- FCFF does not prove business quality, stock safety, or future return.

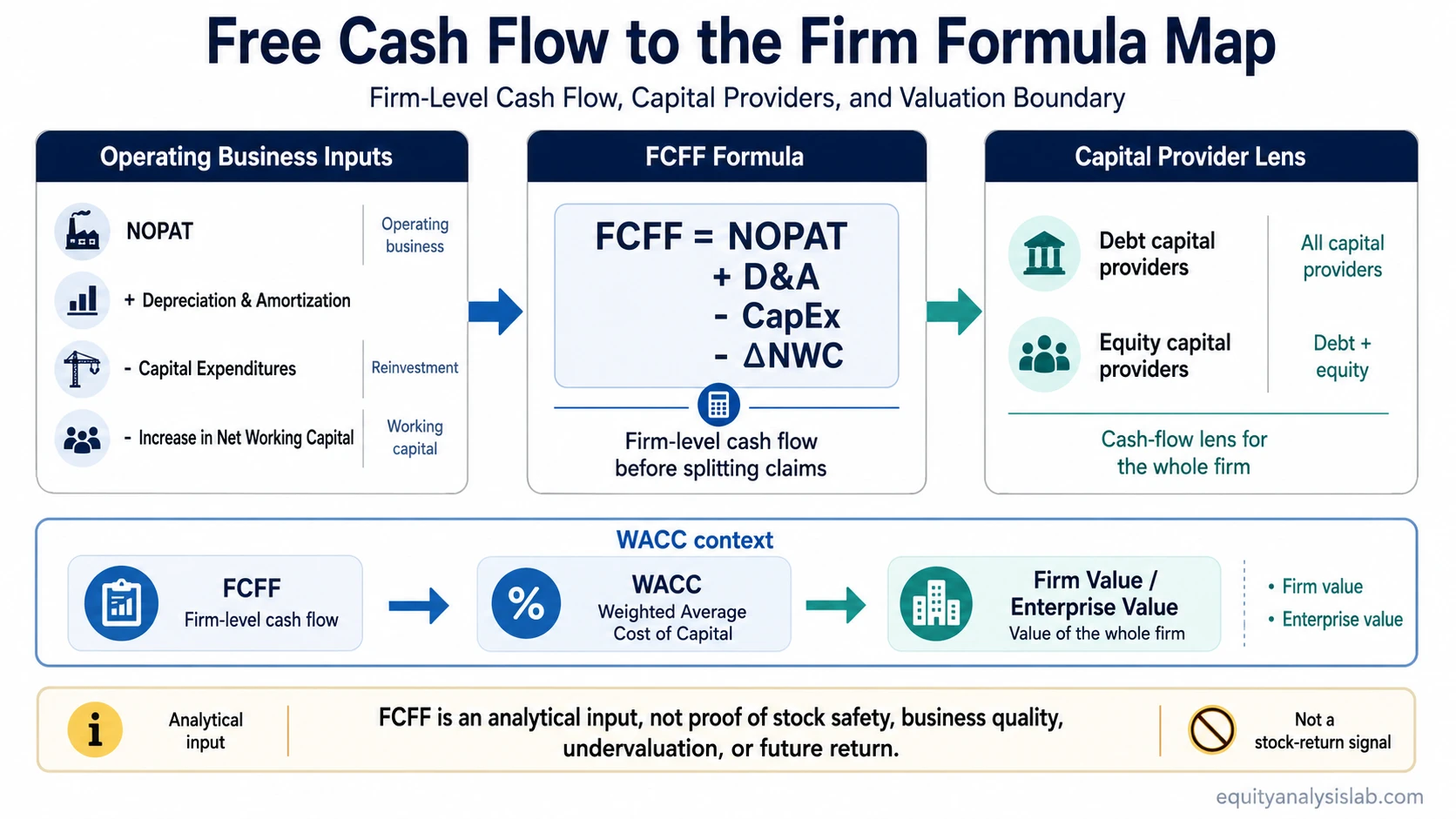

Free Cash Flow to the Firm Formula

Common FCFF formula:

FCFF = NOPAT + D&A - CapEx - ΔNWC

NOPAT means net operating profit after tax. It represents after-tax operating profit before the company is analyzed through the lens of financing choices. Depreciation and amortization are added back because they reduce accounting profit but do not directly consume cash in the current period. Capital expenditures are subtracted because they represent cash reinvested into long-term assets. The change in net working capital is subtracted when more cash is tied up in receivables, inventory, or other operating working-capital needs. If net working capital increases, it usually reduces FCFF because more cash is tied up in operations; if net working capital decreases, the effect can increase FCFF for the period.

| Formula input | What it represents | Interpretation caution |

|---|---|---|

| NOPAT | After-tax operating profit before financing effects | Tax assumptions and operating adjustments can change the result |

| D&A | Non-cash depreciation and amortization added back | High D&A may still point to real future reinvestment needs |

| CapEx | Cash spent on long-term operating assets | Maintenance and growth CapEx are not always separated clearly |

| ΔNWC | Change in operating working capital | Receivable, inventory, and payable timing can distort one period |

A simplified shortcut sometimes starts with operating cash flow and subtracts capital expenditures. That shortcut can be useful as a quick cash-flow view, but it is not always the same as a full FCFF build because financing effects, tax treatment, and working-capital classification still need to be checked.

FCFF and Enterprise Value

FCFF is usually paired with firm value because the cash-flow measure belongs to all capital providers. In a discounted cash flow model, FCFF is commonly discounted at a rate designed for the whole capital structure, then compared with enterprise value or used to estimate firm value.

This matching rule matters. A valuation model should not mix a firm-level cash-flow measure with an equity-only discount rate or an equity-only output without making the proper bridge. The cash flow, discount rate, and valuation output need to describe the same claim on the business.

Valuation boundary: FCFF can support firm-level valuation analysis, but it does not remove the need to check assumptions, reinvestment needs, discount-rate logic, capital structure, and business durability.

FCFF vs FCFE

FCFF and FCFE answer related but different questions. FCFF asks how much cash flow the operating business may generate for all capital providers. FCFE asks how much cash flow may be available to equity holders after financing effects are considered.

| Measure | Main lens | Typical valuation connection |

|---|---|---|

| FCFF | Cash flow available to debt and equity capital providers | Firm value or enterprise value |

| FCFE | Cash flow available to common equity holders | Equity value |

The difference is especially important when debt, interest expense, borrowing, repayment, and capital-structure changes are material. FCFF keeps the analysis focused on the operating business before financing allocation. FCFE moves closer to the shareholder claim after those financing effects are considered.

How FCFF Is Used in DCF Valuation

In DCF valuation, FCFF is often projected over a forecast period, discounted back to present value, and combined with a terminal value assumption. The result is usually a firm-level value estimate before adjustments for net debt or other claims needed to reach common equity value.

This does not make FCFF a complete valuation answer by itself. Forecast assumptions can dominate the output. A small change in margin, reinvestment rate, growth, terminal value, or discount rate can produce a very different value estimate even when the starting FCFF number is the same.

Practical limitation: FCFF is a valuation input. It is not a buy signal, not a quality score, and not a guarantee that the market will recognize value in a specific timeframe.

What FCFF Can Show and What It Can Hide

FCFF is most useful when it is treated as a bridge between operating performance, reinvestment, and valuation. It becomes weaker when the number is accepted without checking how it was produced.

A useful FCFF review checks the operating cash source first, then the reinvestment claim, working-capital movement, one-off items, and capital-structure context.

| FCFF can show | FCFF can hide | What to cross-check |

|---|---|---|

| Whether operating profit is turning into cash after reinvestment | Temporary boosts from working-capital timing | Receivables, inventory, payables, and cash conversion pattern |

| How much cash remains after capital expenditure | Underinvestment that temporarily lifts cash flow | Maintenance CapEx, growth CapEx, asset age, and competitive needs |

| Whether a firm-level DCF input is available | Overconfidence from aggressive forecasts | Forecast horizon, terminal value, margin assumptions, and discount rate |

| How financing-neutral operating cash flow behaves | Debt burden and refinancing risk after firm value is estimated | Net debt, interest coverage, maturity profile, and leverage trend |

Common Mistakes When Reading FCFF

A common mistake is treating positive FCFF as proof of a safe stock. FCFF can be positive because the company is genuinely cash generative, but it can also be temporarily lifted by low reinvestment, favorable working-capital timing, asset sales, or one-off operating conditions.

Another mistake is comparing FCFF across companies without checking business model, capital intensity, industry cycle, and accounting classification. A capital-light software company and a capital-intensive industrial company can have very different reinvestment patterns even when both report positive FCFF.

FCFF also should not be separated from the balance sheet. A company may produce FCFF at the firm level while equity holders still face leverage, dilution, refinancing, or claim-priority issues. The FCFF number belongs to the firm first; the shareholder result depends on what remains after other claims are considered.

FAQ

What is free cash flow to the firm?

Free cash flow to the firm is cash flow available to debt and equity capital providers after operating costs, taxes, reinvestment, capital expenditures, and working-capital needs are considered.

What is the FCFF formula?

A common FCFF formula is NOPAT plus depreciation and amortization, minus capital expenditures, minus the change in net working capital. Other versions can start from EBIT or operating cash flow, but the adjustments must follow the same firm-level valuation lens.

Why is FCFF called unlevered free cash flow?

FCFF is often called unlevered free cash flow because it looks at cash flow before focusing on the effects of debt financing. It is intended to represent cash flow generated by the operating business for the full capital structure.

What is the difference between FCFF and FCFE?

FCFF measures cash flow available to debt and equity capital providers. FCFE focuses on cash flow available to equity holders after financing effects are considered.

Does positive FCFF mean a stock is undervalued?

No. Positive FCFF can support valuation work, but the stock price still depends on assumptions, growth durability, reinvestment needs, risk, capital structure, and the valuation multiple or discount rate used.