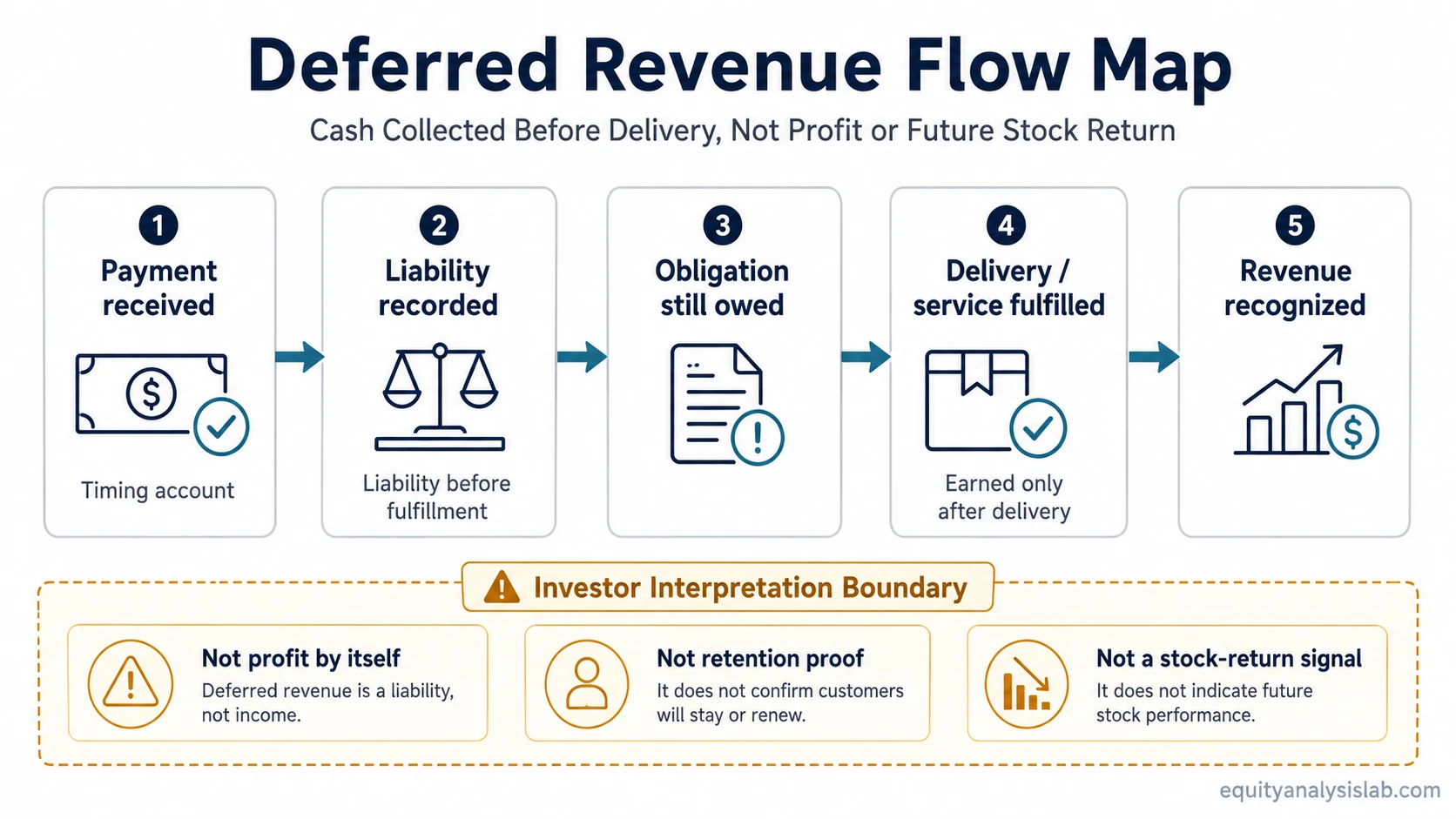

Deferred revenue is cash a company receives before it delivers goods or services. It is recorded as a liability until the company earns the revenue, so investors should read it as a timing and obligation account rather than proof of growth, retention, or future stock returns.

Definition: Deferred revenue is payment collected before the related product, service, subscription period, or contractual obligation has been fulfilled.

The practical accounting issue is timing. The company has already received cash, but it has not yet completed the work needed to treat that cash as earned revenue. Until that obligation is satisfied, deferred revenue usually sits on the balance sheet as a liability.

Key Points

- Deferred revenue is cash received before delivery.

- It is usually a liability because the company still owes goods or services.

- It becomes recognized revenue only as the obligation is fulfilled.

- It can appear in subscription, software, service, gift card, rent, deposit, and contract-based business models.

- It is not automatically positive or negative for investors.

- Rising deferred revenue needs context from billing terms, renewals, churn, contract length, revenue growth, and cash flow.

What Is Deferred Revenue?

Deferred revenue is unearned revenue. A customer has paid, but the company has not yet delivered enough value under the contract to recognize the payment as revenue on the income statement.

A simple example is a one-year software subscription paid upfront. The company receives cash at the start of the contract, but it does not earn the full amount on day one. As each month of service is provided, part of the liability is reduced and part of the payment becomes recognized revenue.

That distinction matters because cash collection and revenue recognition do not always happen at the same time. Deferred revenue keeps those two events separate.

Why Deferred Revenue Is a Liability

Deferred revenue is usually a liability because the company has an obligation after receiving payment. The obligation might be access to software, delivery of goods, completion of a service, use of a gift card, or another future performance requirement.

The liability exists because the customer has already paid for something the company still needs to provide. If the company does not fulfill the obligation, it may need to refund the payment, extend service, deliver replacement value, or otherwise settle the obligation under the contract.

Investor reading: deferred revenue is not the same as profit. It is a timing and obligation account. It can support future reported revenue if the company fulfills the obligation, but it does not by itself prove margin quality, customer retention, or valuation upside.

How Deferred Revenue Moves Through Financial Statements

Deferred revenue starts with cash collection and ends with revenue recognition. The key is that cash flow can appear before the income statement shows the related revenue.

| Step | What happens | Financial statement effect | Investor reading |

|---|---|---|---|

| Cash received | The customer pays before delivery or service completion. | Cash increases. | Cash collection has occurred, but revenue may not yet be earned. |

| Obligation exists | The company still owes goods, services, access, or another contractual benefit. | A deferred revenue liability is recorded. | The company has future work or delivery obligations tied to prior cash collection. |

| Product or service delivered | The company satisfies part or all of the obligation. | The deferred revenue liability declines. | Revenue recognition becomes supported by actual delivery. |

| Revenue recognized | The earned portion moves into revenue. | Revenue increases on the income statement. | Reported revenue catches up with the portion of the contract that has been earned. |

This sequence is one reason deferred revenue can be useful in company analysis. It connects cash collection, contract obligations, and later revenue recognition without treating all collected cash as already earned.

Deferred Revenue Journal Entry, in Plain Terms

The basic journal-entry idea is simple: when cash is received before delivery, cash increases and deferred revenue increases. As the company earns the revenue, deferred revenue decreases and revenue increases.

| Event | Plain-English accounting effect | What it means |

|---|---|---|

| Customer prepays | Cash goes up and deferred revenue goes up. | The company has received money but still owes delivery. |

| Company earns part of the contract | Deferred revenue goes down and recognized revenue goes up. | The company has fulfilled part of the obligation. |

This is enough for investor interpretation. Detailed accounting standards, revenue-recognition tests, and contract-specific treatment require source documents or accounting guidance beyond a general investing explanation.

A Simple Deferred Revenue Example

Illustrative example: A software company sells a 12-month subscription for $1,200 and collects the full amount upfront. At the start, the company has $1,200 of cash and $1,200 of deferred revenue. If service is provided evenly, $100 becomes recognized revenue each month and the deferred revenue balance declines by $100 each month.

This example is simplified, but it captures the core timing issue. Cash arrived before the full service period was complete. Revenue is recognized gradually as the service is delivered.

Subscription models often create deferred revenue because customers may pay before the full service period is provided. That does not make deferred revenue identical to recurring revenue. Recurring revenue describes the repeatable nature of the revenue model, while deferred revenue describes an accounting liability created by prepayment.

Deferred Revenue vs Accrued Revenue and Accounts Receivable

Deferred revenue is often confused with accrued revenue and accounts receivable because all three involve timing differences between cash, billing, delivery, and revenue recognition.

| Concept | Cash timing | Revenue timing | Typical balance-sheet classification |

|---|---|---|---|

| Deferred revenue | Cash received before delivery. | Revenue recognized later as obligations are fulfilled. | Liability. |

| Accrued revenue | Cash not yet received. | Revenue has been earned before cash collection. | Asset, depending on presentation and collection rights. |

| Accounts receivable | Cash not yet received. | Revenue has usually been billed or earned. | Asset. |

The clean distinction is direction. Deferred revenue starts with cash before earned revenue. Accrued revenue and accounts receivable usually start with earned or billable revenue before cash collection.

Deferred Revenue in Subscription and SaaS Businesses

Deferred revenue is common in subscription and SaaS businesses because customers may pay monthly, quarterly, annually, or multi-year in advance. The accounting balance depends on how much cash has been collected before the related service period has been completed.

This is why deferred revenue can look similar to SaaS operating metrics but should not be treated as the same thing. For example, ARR-style subscription metrics are used to describe recurring contract value, while deferred revenue is an accounting liability tied to cash received before revenue is earned.

A company can have meaningful deferred revenue because customers prepay, because billing terms changed, because contract lengths increased, or because acquisitions added liabilities. Those causes have different implications, so the line item needs context.

How Investors Should Interpret Deferred Revenue

Deferred revenue can be useful because it shows that some cash has arrived before reported revenue recognition. In a recurring or contract-based model, that can help investors understand billing structure, customer prepayment behavior, and the timing bridge between cash flow and reported revenue.

The strongest interpretation usually comes from comparing deferred revenue against several nearby signals:

| What to compare | Why it matters |

|---|---|

| Revenue growth | Deferred revenue is more useful when it connects to actual recognized revenue over time. |

| Operating cash flow | Cash collection quality matters more than the liability balance alone. |

| Renewals and churn | Prepayment is stronger when customers renew rather than disappear after the paid period. |

| Billing terms | Longer or more upfront billing can lift deferred revenue without a matching improvement in demand. |

| Peer group | Deferred revenue levels are more meaningful when compared with similar business models. |

For investors, deferred revenue is best treated as a context signal. It can support analysis of revenue timing and business model structure, but it should not be isolated from margins, cash conversion, retention, and the quality of future obligations.

When Deferred Revenue Can Mislead

Limitation: rising deferred revenue can be positive, neutral, or misleading. It can reflect healthy prepayments, but it can also reflect billing-term changes, longer contracts, acquisitions, seasonal timing, or obligations that are expensive to fulfill.

A rising balance may look encouraging because customers have paid before revenue is recognized. That reading is incomplete if renewals are weakening, churn is rising, cash flow quality is poor, or the company must spend heavily to deliver the promised product or service.

Deferred revenue can also create false comfort when investors treat it as a guaranteed revenue pipeline. The liability still has to be earned. If delivery quality, customer satisfaction, renewal behavior, or contract economics deteriorate, the accounting balance alone does not protect the investment case.

What Deferred Revenue Does Not Prove

Deferred revenue does not prove that a company is undervalued. It does not prove that customers will renew. It does not prove high earnings quality. It does not predict stock performance.

It also does not automatically mean the business has better economics than a company with lower deferred revenue. Some business models collect upfront. Others bill after delivery. The accounting pattern must be interpreted alongside the company’s contracts, cash flow, margins, and customer behavior.

Common mistake: treating deferred revenue as already earned revenue. The cash has been collected, but the revenue becomes earned only as the company satisfies the related obligation.

FAQ

Is deferred revenue a liability?

Yes. Deferred revenue is usually recorded as a liability because the company has received cash before delivering the related goods or services.

Is deferred revenue good or bad?

Deferred revenue is not automatically good or bad. It can reflect useful customer prepayment, but it needs context from billing terms, renewals, churn, delivery obligations, revenue growth, and cash flow.

When does deferred revenue become revenue?

Deferred revenue becomes recognized revenue as the company delivers the goods or services and satisfies the obligation tied to the customer payment.

What is the difference between deferred revenue and accounts receivable?

Deferred revenue means cash was received before revenue was earned. Accounts receivable usually means revenue has been earned or billed, but cash has not yet been collected.

Does deferred revenue prove recurring revenue?

No. Deferred revenue can appear in subscription models, but it is an accounting liability from prepayment. Recurring revenue describes the repeatable nature of revenue, not just the timing of cash collection.