Exit multiple is a valuation assumption that applies a selected multiple to a future operating metric, often EBITDA or EBIT, to estimate an implied terminal value.

The result is not a complete valuation verdict. It is one way to translate a final forecast year into a continuing value estimate, usually by asking what multiple a comparable business might reasonably deserve at the end of the forecast period.

What Is Exit Multiple?

An exit multiple is the valuation multiple assumed at the end of a forecast period. In a valuation model, it usually takes a future financial metric and multiplies it by a selected market or peer-based multiple.

For example, if a business is expected to generate final-year EBITDA of $100 million and the model applies a 9x exit multiple, the implied terminal value is $900 million before any discounting or additional model adjustments.

The term is common in discounted valuation work because many forecasts stop after a limited explicit period. The exit multiple provides one method for estimating what the business could be worth beyond that forecast window.

Where Exit Multiple Fits in Valuation

Exit multiple is most often used to estimate terminal value, the value assigned to the business after the explicit forecast period ends.

In a discounted cash flow model, an analyst may forecast cash flows for several years, estimate terminal value with an exit multiple, and then discount those future values back to the present.

The assumption matters because terminal value can represent a large share of the total valuation. A small change in the selected multiple can create a large change in the implied value, especially when the final-year metric is large or the forecast period is long.

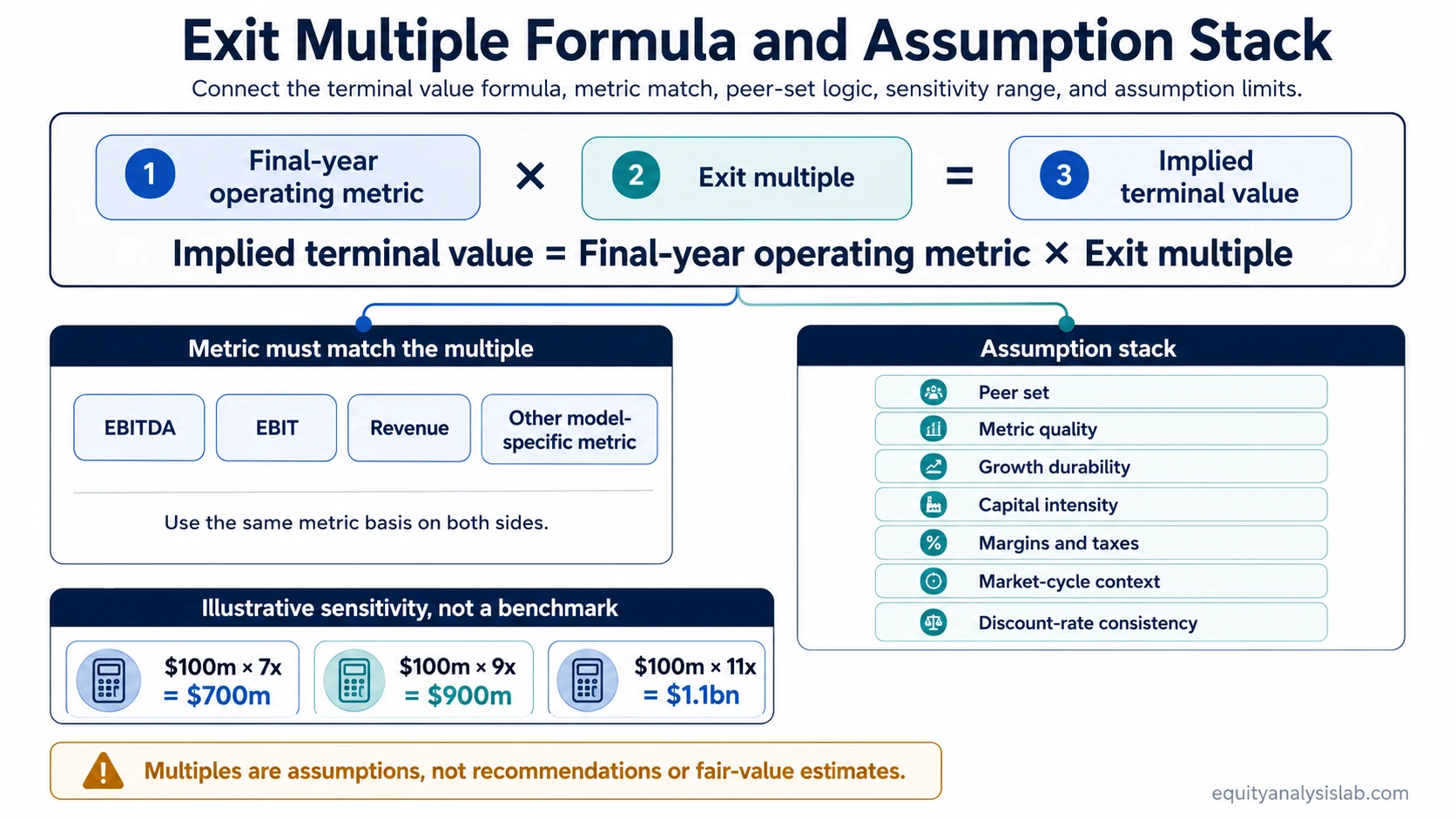

Exit Multiple Formula

The basic formula is:

Implied terminal value = Final-year operating metric × Exit multiple

The operating metric is usually EBITDA, EBIT, revenue, or another measure that fits the business model. The selected multiple should match the metric. An EBITDA-based terminal value should use an EBITDA-based multiple, not a revenue or earnings multiple.

For EBITDA-based valuation work, the exit multiple is often related to an EV/EBITDA multiple. That does not mean the number can be copied mechanically. The peer group, growth profile, margin structure, capital intensity, and forecast assumptions still have to be comparable.

What the Exit Multiple Assumption Depends On

An exit multiple compresses several valuation judgments into one number. The multiple is not only a market quote. It reflects assumptions about future growth, business quality, reinvestment needs, profitability, and risk.

| Assumption area | Why it matters | Risk if ignored |

|---|---|---|

| Peer set | The selected multiple usually comes from comparable companies or transactions. | A weak peer group can make the terminal value look market-based while reflecting businesses with different economics. |

| Terminal-year metric quality | The final-year EBITDA, EBIT, or revenue figure must represent a sustainable level of performance. | A temporarily elevated metric can make the valuation look cheaper than it really is. |

| Growth durability | Higher multiples usually require stronger evidence that growth can continue beyond the explicit forecast. | A growth assumption may be double-counted if the forecast already assumes expansion and the exit multiple also assumes a premium. |

| Capital intensity | Companies with similar EBITDA can require very different reinvestment to maintain or grow that EBITDA. | An EBITDA multiple can overstate value when depreciation, maintenance capital expenditure, or working capital needs are high. |

| Margin and tax differences | Similar revenue or EBITDA multiples can hide differences in margins, taxes, and cash conversion. | Two companies can deserve different multiples even if they operate in the same sector. |

| Market-cycle context | Multiples can expand or compress with interest rates, liquidity, risk appetite, and sector sentiment. | A current market multiple may be too optimistic or too pessimistic for a future terminal year. |

| Discount-rate consistency | The discount rate and exit multiple should tell a coherent risk story. | A model can become internally inconsistent if it uses a high-risk discount rate and a premium terminal multiple without support. |

Exit Multiple Sensitivity Example

Assume a final-year EBITDA estimate of $100 million. The same operating metric can produce very different implied terminal values depending on the selected exit multiple.

| Final-year EBITDA | Exit multiple | Implied terminal value | Interpretation risk |

|---|---|---|---|

| $100m | 7x | $700m | May be conservative if peers trade higher for durable business reasons. |

| $100m | 9x | $900m | Base-case only if the peer set, growth profile, and margin structure are comparable. |

| $100m | 11x | $1.1bn | Aggressive if unsupported by margins, reinvestment needs, capital intensity, or cycle context. |

This is an illustrative sensitivity example only. The multiples are not benchmarks, recommendations, or fair-value estimates for any company or sector.

Why Exit Multiple Can Create False Precision

Exit multiple can look precise because the formula is simple. The fragile part is not the multiplication. The fragile part is deciding whether the metric, peer set, growth assumption, discount rate, and market context all support the same valuation story.

A higher exit multiple does not automatically mean a business is worth more in a useful analytical sense. It may simply mean the model is assuming stronger future conditions, better comparability, lower risk, or a more favorable market environment.

Exit Multiple vs Perpetual Growth Method

Exit multiple and the perpetual growth method are two common ways to estimate terminal value. The exit multiple approach uses a market-based multiple applied to a future operating metric. The perpetual growth method estimates continuing value from normalized cash flow and a long-term growth assumption.

The two methods can produce very different results. A useful valuation check asks whether both methods imply a reasonable story about growth, reinvestment, risk, and cash generation.

Common Mistakes When Using Exit Multiple

- Treating the multiple as a standalone verdict: the multiple is one assumption inside a valuation process, not a conclusion by itself.

- Borrowing a peer multiple without checking comparability: similar sector labels do not guarantee similar margins, growth, risk, or reinvestment needs.

- Applying a current multiple to a future year without adjustment: the terminal year may have different growth, rates, profitability, and market conditions.

- Using the wrong metric: EBITDA, EBIT, revenue, and earnings multiples answer different valuation questions.

- Assuming multiple expansion without a reason: a higher exit multiple needs support from business quality, growth durability, or lower risk.

- Mixing business-sale logic with public-equity valuation logic: advisory or transaction framing can differ from investor-focused valuation work.

- Ignoring capital intensity and taxes: EBITDA can miss cash demands that affect the value available to owners.

How Investors Can Interpret Exit Multiple

A useful exit multiple assumption should answer three questions: what metric is being capitalized, why the selected multiple fits that metric, and what would make the assumption too high or too low.

The strongest use is sensitivity analysis, not a single-point estimate. Comparing several plausible multiples helps show how much of the valuation depends on the final continuing-value assumption rather than near-term business performance.

When the valuation conclusion depends heavily on one optimistic exit multiple, the model may be more fragile than it appears. When the conclusion remains reasonable across a range of defensible multiples, the terminal-value assumption is less likely to dominate the analysis.

Related Valuation Concepts

Terminal value is the closest related concept because exit multiple is one way to estimate value beyond the explicit forecast period.

Discounted cash flow is the broader valuation structure where forecast cash flows, terminal value, and discounting are combined.

EV/EBITDA is one of the common multiple frameworks used when the exit multiple is based on EBITDA rather than revenue, EBIT, earnings, or free cash flow.