EBITDA means earnings before interest, taxes, depreciation, and amortization, so it shows profit before financing costs, tax effects, and non-cash D&A charges, but it does not show how much cash the business actually produced.

EBITDA definition: EBITDA is an accounting-based profitability measure that starts with earnings and adds back interest, taxes, depreciation, and amortization. Investors use it to compare operating earnings before capital structure, tax position, and certain non-cash accounting charges affect the result.

EBITDA can help when comparing companies with different debt levels, tax situations, or depreciation schedules. It becomes less useful when the comparison ignores capital intensity, working capital needs, lease structure, maintenance spending, or the difference between reported earnings and actual cash conversion.

Key points about EBITDA

- EBITDA adds back interest, taxes, depreciation, and amortization.

- It is usually read as a pre-financing, pre-tax, pre-D&A earnings measure.

- It is not the same as cash flow, free cash flow, net income, EBIT, or EV/EBITDA.

- It is most useful when the peer set, period, accounting base, leverage, and capital intensity are comparable.

What EBITDA means in company analysis

In company analysis, EBITDA is a profitability diagnostic. It tries to isolate earnings before financing choices, tax position, and depreciation or amortization charges. That can make it easier to compare operating earnings across companies that use different debt structures or own assets with different accounting lives.

The metric is still incomplete. A company can report rising EBITDA while cash generation weakens because receivables build, inventory rises, capital spending increases, or debt service consumes more of the operating result. EBITDA is therefore a starting point for comparison, not a verdict on business quality.

A stronger EBITDA read usually checks the source line, the period, the peer group, the accounting treatment, and whether the earnings translate into cash. Without those checks, EBITDA can make an asset-heavy or highly leveraged company look cleaner than the economics actually are.

EBITDA formula

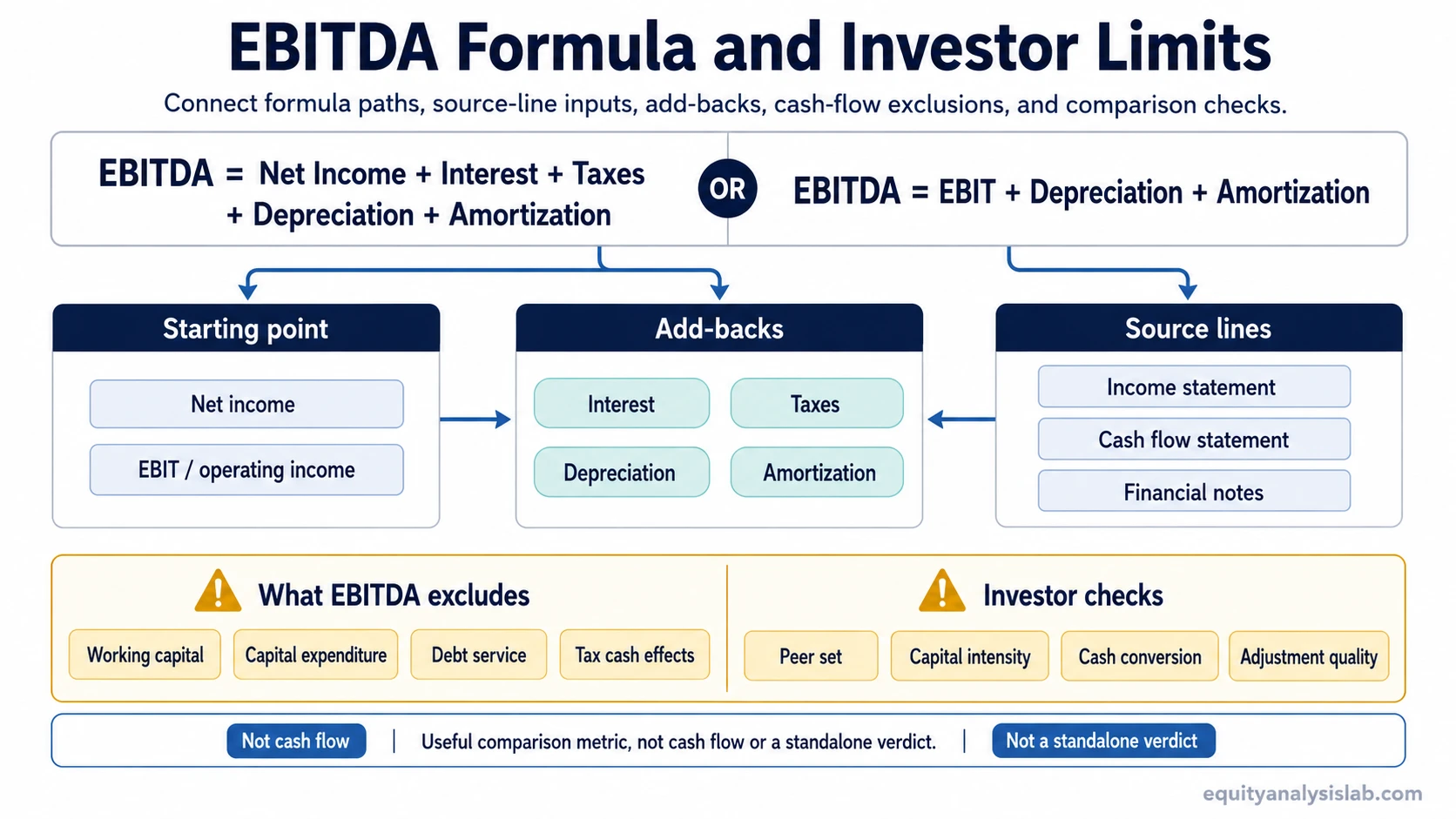

There are two common formula paths. One starts from net income and adds back the items EBITDA is designed to exclude. The other starts from EBIT or operating income and adds back depreciation and amortization.

| Formula path | Formula | What the path shows |

|---|---|---|

| From net income | EBITDA = Net income + Interest expense + Taxes + Depreciation + Amortization | Starts from the bottom-line profit figure and reverses financing, tax, and D&A effects. |

| From EBIT or operating income | EBITDA = EBIT + Depreciation + Amortization | Starts from operating profit before interest and taxes, then removes D&A charges. |

The add-backs do not mean the excluded costs are irrelevant. Interest still affects equity holders, taxes still affect after-tax value, and depreciation can reflect real asset wear even though it is a non-cash charge in the current period.

Where EBITDA inputs come from

EBITDA is usually built from the income statement, cash flow statement, and financial statement notes. The exact source depends on how the company presents operating profit, depreciation, amortization, interest expense, and tax expense.

| Input | Common statement location | Why it is added back | Investor caution |

|---|---|---|---|

| Net income | Income statement | Starting point for the full add-back formula. | Includes financing, tax, and non-operating effects that may need review. |

| Interest expense | Income statement or notes | Removes financing cost to compare pre-financing earnings. | High interest expense still matters for equity value and solvency risk. |

| Taxes | Income statement or tax note | Removes tax effects that may differ across jurisdictions or periods. | Temporary tax benefits can make after-tax earnings look stronger than recurring economics. |

| Depreciation | Cash flow statement, notes, or cost detail | Adds back a non-cash accounting charge for tangible asset use. | Depreciation may still represent real maintenance capital needs over time. |

| Amortization | Cash flow statement, notes, or intangible asset detail | Adds back a non-cash accounting charge for intangible assets. | Amortization can be tied to acquisition accounting and may affect comparability. |

Simple EBITDA calculation example

Assume a company reports net income of $120 million, interest expense of $30 million, tax expense of $40 million, depreciation of $25 million, and amortization of $10 million.

EBITDA calculation: $120 million + $30 million + $40 million + $25 million + $10 million = $225 million.

That $225 million result is not the same as free cash flow. The company may still need to fund capital expenditure, working capital, debt repayment, leases, taxes, or other cash obligations that EBITDA does not capture.

What EBITDA includes and excludes

EBITDA includes the earnings generated before the selected add-backs. It excludes several items that may still be economically important. That is why the metric should be read beside cash flow and balance-sheet context.

| Included or excluded | Item | How to interpret it |

|---|---|---|

| Included | Revenue and operating costs before add-backs | Shows the operating base that supports the earnings measure. |

| Excluded | Interest expense | Improves pre-financing comparison, but debt cost still matters. |

| Excluded | Taxes | Improves pre-tax comparison, but after-tax value still depends on tax outcomes. |

| Excluded | Depreciation and amortization | Removes non-cash charges, but asset replacement and acquisition quality still matter. |

| Not captured directly | Working capital and capital expenditure | These can create a large gap between EBITDA and cash generation. |

EBITDA limitations investors should check

EBITDA can be useful, but it can also overstate economic strength when important cash demands are ignored. The main risk is treating a pre-financing, pre-tax, pre-D&A measure as if it were cash available to owners.

- Capital expenditure: Asset-heavy companies may need large reinvestment just to maintain capacity.

- Working capital: Receivables, inventory, and payables can make reported EBITDA differ from cash conversion.

- Debt service: Interest is added back, but lenders still have to be paid.

- Lease structure: Lease accounting can affect comparability across companies and periods.

- Adjustments: Adjusted EBITDA can exclude real recurring costs if management add-backs are too aggressive.

EBITDA vs related metrics

EBITDA is one member of a wider earnings and cash-flow toolkit. It becomes more useful when it is compared with related measures rather than read in isolation.

| Metric | Main focus | How it differs from EBITDA |

|---|---|---|

| Net income | Bottom-line accounting profit | Includes interest, taxes, depreciation, amortization, and other below-operating effects. |

| EBIT | Operating profit before interest and taxes | Keeps depreciation and amortization inside the profit measure. |

| Operating cash flow | Cash generated by operations | Includes working-capital effects that EBITDA excludes. |

| Free cash flow | Cash left after capital expenditure | Captures reinvestment needs that EBITDA does not directly capture. |

| EV/EBITDA | Valuation multiple | Uses EBITDA as the denominator, but adds enterprise value and valuation context. |

How investors should use EBITDA

EBITDA is most useful as a comparison metric, not as a standalone answer. It can help normalize differences in financing structure, tax position, and depreciation or amortization schedules, but it should be checked against cash conversion and reinvestment needs.

Practical investor check: Read EBITDA beside operating cash flow, free cash flow, capital expenditure, working-capital movement, leverage, interest coverage, and the company’s adjustment policy.

For peer comparisons, the strongest read usually comes from companies in the same industry with similar accounting rules, asset intensity, lease structures, and business models. Comparing EBITDA across unrelated sectors can produce misleading conclusions because the same EBITDA number can represent very different economics.

EBITDA FAQ

What does EBITDA stand for?

EBITDA stands for earnings before interest, taxes, depreciation, and amortization. It is an accounting-based earnings measure used to compare profit before financing costs, tax effects, and D&A charges.

Is EBITDA profit?

EBITDA is a profit measure, but it is not the same as net income or cash profit. It removes selected expenses and non-cash charges, so it can make earnings look cleaner than the amount ultimately available to shareholders.

Is EBITDA the same as cash flow?

No. EBITDA excludes working-capital movements and capital expenditure. A company can report positive EBITDA while cash flow is weaker because cash is tied up in receivables, inventory, maintenance spending, or debt service.

Can EBITDA be negative?

Yes. EBITDA can be negative when operating losses are large enough that adding back depreciation and amortization does not bring the metric above zero. Negative EBITDA usually requires closer review of revenue quality, cost structure, cash burn, and financing risk.

What is a good EBITDA?

There is no universal good EBITDA number. Interpretation depends on company size, sector, growth rate, margin structure, leverage, capital intensity, accounting treatment, and whether EBITDA converts into cash.