Net working capital is the difference between a company’s current assets and current liabilities. It is calculated from balance sheet inputs and helps investors read short-term liquidity, cash tied up in operations, and account-quality risk without treating the number as proof of business quality.

Definition: Net working capital is a dollar amount that compares resources expected to turn into cash within a year with obligations expected to come due within a year.

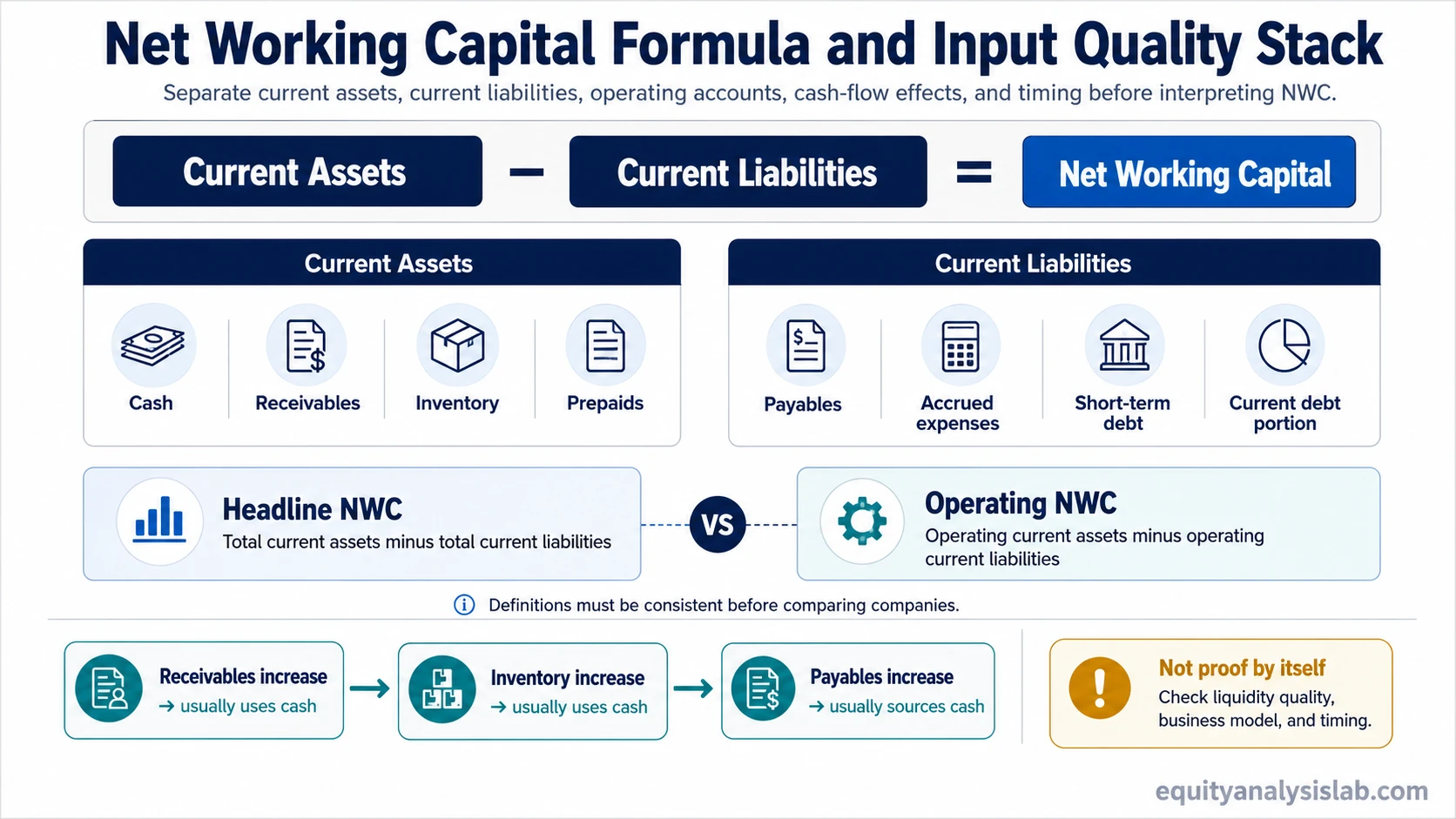

Formula: Net Working Capital = Current Assets – Current Liabilities

A positive number means current assets exceed current liabilities. A negative number means current liabilities exceed current assets. The useful interpretation depends on the account mix, collection speed, inventory quality, debt timing, and business model.

Net Working Capital Formula

The formula subtracts current liabilities from current assets. It is a dollar amount, not a ratio, so it shows the size of the short-term surplus or shortfall rather than the proportion of coverage.

| Formula part | What it includes | Interpretation note |

|---|---|---|

| Current assets | Cash, accounts receivable, inventory, prepaid expenses, and other assets expected to convert to cash or be used within the operating cycle | Higher current assets can improve flexibility, but receivables may be slow to collect and inventory may be hard to sell at expected value. |

| Current liabilities | Accounts payable, accrued expenses, short-term debt, current portion of long-term debt, and other obligations due soon | Higher current liabilities can create pressure, although some operating liabilities, such as accounts payable, may also reflect supplier financing. |

| Net working capital | Current assets minus current liabilities | The result gives a short-term liquidity snapshot, not a complete test of solvency, profitability, or business quality. |

Where Net Working Capital Appears on the Balance Sheet

Net working capital is calculated from current asset and current liability lines. The exact line items vary by company, but the calculation usually starts with the current section rather than long-term assets, long-term debt, equity, or income statement accounts.

Common current asset inputs include cash and cash equivalents, accounts receivable, inventory, and prepaid expenses. Common current liability inputs include accounts payable, accrued expenses, short-term borrowings, and the current portion of long-term debt.

Classification matters because not every current asset has the same liquidity value. Cash is already liquid. Receivables depend on customer collection. Inventory depends on demand, pricing, and obsolescence risk. Prepaids may reduce future expense, but they are not usually cash available for debt repayment.

Headline NWC vs Operating NWC

Headline net working capital uses total current assets and total current liabilities. Operating net working capital narrows the view to operating current assets and operating current liabilities, often excluding cash, short-term investments, short-term debt, and the current portion of long-term debt.

Headline NWC: useful for a broad short-term liquidity snapshot.

Operating NWC: useful for understanding how receivables, inventory, payables, and other operating accounts affect cash tied up in the business.

| Measure | Typical focus | What can distort it |

|---|---|---|

| Headline net working capital | Total current assets minus total current liabilities | Large cash balances, short-term debt, or current debt maturities can dominate the result. |

| Operating net working capital | Operating current assets minus operating current liabilities | Different companies classify operating accounts differently, so comparisons require consistent definitions. |

Operating NWC is not a replacement for the headline calculation. It is a narrower lens for separating financing and cash balances from the working capital needed to run the business.

How Changes in Net Working Capital Affect Cash Flow

A change in net working capital helps explain why accounting profit and cash flow can move differently. When more cash is tied up in receivables or inventory, near-term operating cash flow can weaken even if sales or reported earnings look stronger.

| Account movement | Typical cash-flow effect | Why it matters |

|---|---|---|

| Accounts receivable increases | Usually uses cash | Revenue may have been recognized before cash was collected from customers. |

| Inventory increases | Usually uses cash | Cash may be tied up in goods before they are sold or converted back into cash. |

| Accounts payable increases | Usually sources cash | The company may be delaying cash payment to suppliers while keeping goods or services already received. |

A rising NWC balance can signal business expansion, but it can also mean cash is being absorbed by receivables or inventory. A falling NWC balance can release cash, but the reason matters. Supplier stretch, inventory liquidation, or weaker collection quality can create very different readings.

What Positive or Negative Net Working Capital Can Mean

Positive net working capital can indicate that a company has more current assets than current liabilities. That can support short-term flexibility, especially when the current assets are cash or receivables that are likely to be collected on time.

Negative net working capital can indicate liquidity pressure when obligations are coming due faster than assets can convert into cash. The reading becomes more concerning when short-term debt, overdue payables, weak collections, or obsolete inventory drive the shortfall.

Some business models can operate with low or negative net working capital without immediate distress. A company that collects cash from customers before paying suppliers can show negative NWC while still producing operating cash. That is different from a shortfall driven by debt maturities, stretched payables, or poor collections.

Liquidity Quality and Comparability Limits

Liquidity quality: A large NWC balance is weaker if receivables are slow to collect, inventory is hard to sell, or current liabilities are fixed and near-term.

Business-model comparability: Retailers, software companies, manufacturers, distributors, and subscription businesses can carry very different working-capital structures.

Period comparison: One balance sheet date can be misleading if seasonality, payment timing, or inventory buildup temporarily changes current accounts.

The stronger analysis asks which accounts drive the number, whether the change repeats across periods, and whether the account mix is normal for the company’s business model.

Simple Net Working Capital Example

A company reports $180 million of current assets and $120 million of current liabilities.

Net Working Capital = $180 million – $120 million = $60 million

The company has positive net working capital of $60 million. The result looks better if the current assets are mostly cash and collectible receivables. It looks weaker if most of the balance is slow-moving inventory or receivables that may not be collected on time.

Net Working Capital Interpretation Checklist

- Is net working capital positive or negative?

- Which current asset and current liability accounts drive the result?

- Did the balance rise or fall versus the prior period?

- Did accounts receivable, inventory, or accounts payable explain most of the change?

- Is the account mix comparable across companies with different business models?

- Does the cash-flow statement confirm or challenge the balance sheet reading?

Related Concepts

Net working capital works best when it is read beside nearby financial statement and liquidity concepts.

| Concept | Use it for | How it differs from net working capital |

|---|---|---|

| Balance sheet | Finding current assets, current liabilities, debt, equity, and asset structure | Net working capital is calculated from selected current sections of the statement. |

| Current ratio | Comparing current assets with current liabilities as a ratio | Net working capital gives a dollar amount, while the ratio gives proportional coverage. |

| Cash conversion cycle | Reading how inventory, receivables, and payables affect operating timing | Net working capital gives a balance; the cycle focuses on timing and efficiency. |

FAQ

Is net working capital the same as working capital?

In many finance contexts, net working capital and working capital are used to mean current assets minus current liabilities. Some analysis uses narrower operating definitions, so the included accounts should be checked before comparing companies.

Is negative net working capital always bad?

No. Negative net working capital can signal pressure, especially when near-term liabilities exceed liquid assets. It can also be normal for some business models that collect cash before paying suppliers. The account mix and business model determine the interpretation.

How does net working capital affect cash flow?

Increases in receivables or inventory usually use cash, while increases in accounts payable usually provide cash. The cash-flow effect depends on which account changed and why it changed.