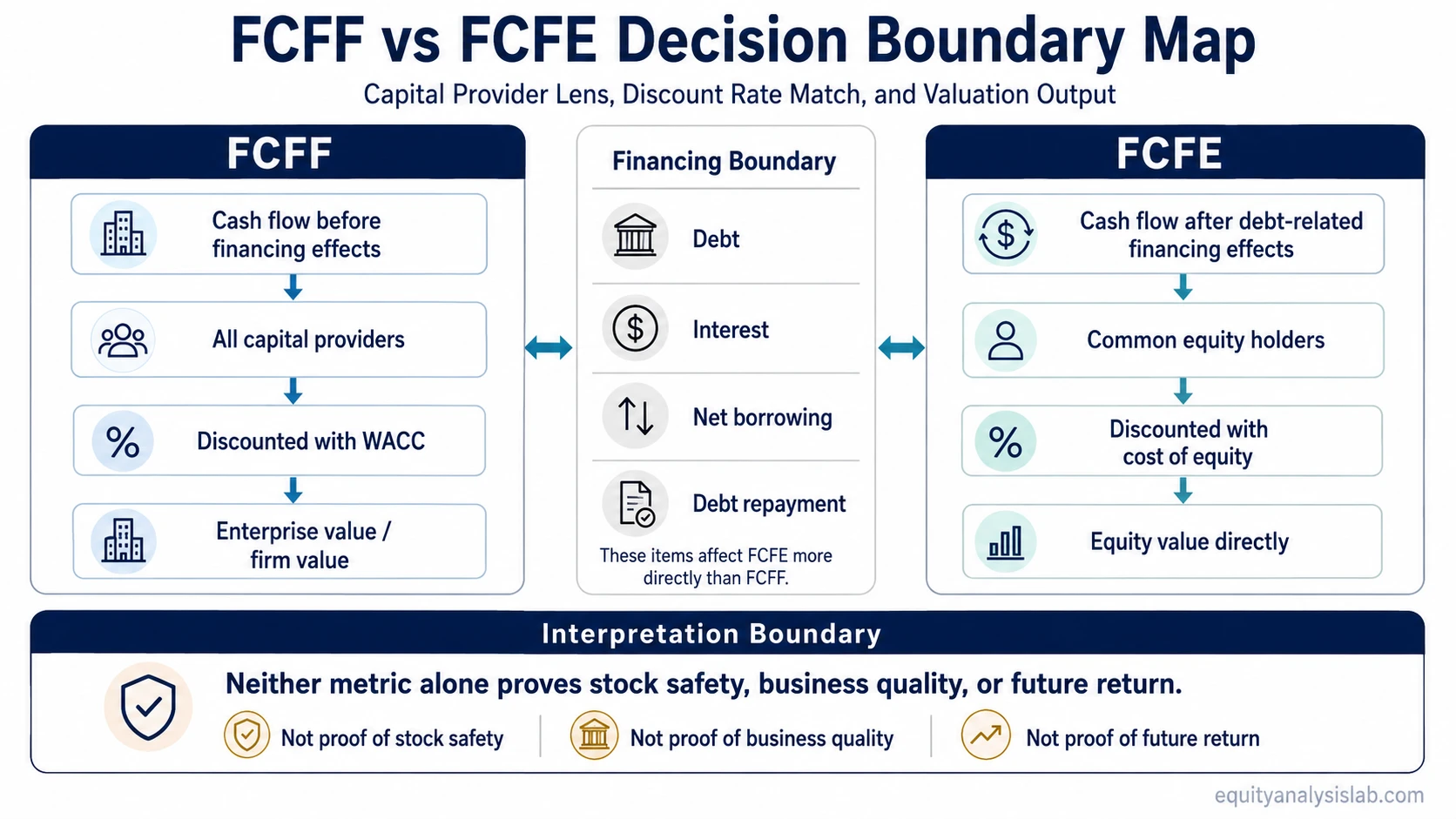

FCFF vs FCFE separates two cash-flow lenses: FCFF estimates cash flow available to all capital providers before financing effects, while FCFE estimates cash flow left for common equity holders after debt-related financing effects.

The distinction matters because the valuation object changes. FCFF is used when the investor is valuing the whole firm before separating debt and equity claims. FCFE is used when the investor is valuing the cash flow available to common shareholders after the company’s financing structure has already affected the cash-flow picture.

Both measures sit inside the broader idea of free cash flow, but they should not be treated as interchangeable labels. The issue is not which number is larger, but whether the cash flow matches the correct capital claim and valuation output.

Key Points

- FCFF is a firm-level cash-flow measure before financing effects and is normally used to estimate enterprise value.

- FCFE is an equity-holder cash-flow measure after debt-related financing effects and is normally used to estimate equity value directly.

- FCFF usually pairs with WACC, while FCFE usually pairs with the cost of equity.

- The right measure depends on the valuation question, not on which cash-flow number appears higher.

- Neither FCFF nor FCFE alone proves business quality, stock safety, or future return.

FCFF vs FCFE: The Core Difference

FCFF stands for free cash flow to the firm. It looks at cash flow available to the entire capital structure, including both debt holders and equity holders. Because it is a firm-level measure, it is usually connected to enterprise value.

FCFE stands for free cash flow to equity. It looks at cash flow available to common equity holders after interest, debt borrowing, and debt repayment effects are considered. Because it is an equity-holder measure, it connects more directly to the value of the common equity claim.

The boundary is capital-provider perspective. FCFF asks what cash flow the operating business can support before financing claims are split. FCFE asks what remains for shareholders after the financing structure has changed the cash-flow path.

FCFF vs FCFE Comparison Table

| Criterion | FCFF | FCFE | Investor Interpretation |

|---|---|---|---|

| Full name | Free cash flow to the firm | Free cash flow to equity | The names describe different capital claims, not two versions of the same output. |

| Capital provider lens | Debt and equity holders together | Common equity holders | FCFF is firm-level; FCFE is shareholder-level. |

| Financing treatment | Before financing effects | After debt-related financing effects | Debt structure affects FCFE more directly than FCFF. |

| Typical valuation output | Enterprise value or firm value | Equity value directly | The cash-flow measure must match the value being estimated. |

| Typical discount rate | WACC | Cost of equity | Using the wrong discount rate can mix firm value and equity value logic. |

| Debt sensitivity | Less directly affected by debt issuance or repayment | Directly affected by net borrowing and debt repayment | FCFE can move because financing changed, even when operating performance did not improve. |

| Common mistake | Discounting FCFF with cost of equity | Discounting FCFE with WACC | The error usually comes from matching the right cash flow to the wrong value base. |

Why the Capital Provider Lens Changes the Valuation Output

FCFF starts with the business before the final split between creditors and shareholders. That is why it is usually discounted at WACC, because WACC reflects the blended required return of the firm’s capital providers.

FCFE starts after the debt claim has already affected the cash flow available to shareholders. That is why it is usually discounted at the cost of equity, because the remaining cash flow belongs to equity holders rather than to the whole capital structure.

The same operating business can therefore produce two different valuation paths. One path estimates firm value first and then adjusts for debt and non-equity claims. The other path estimates the value attributable to common shareholders more directly.

How Debt, Interest, and Net Borrowing Affect FCFF and FCFE

FCFF is often described as unlevered free cash flow because it tries to separate operating cash flow from the company’s financing choices. A common formula path starts with after-tax operating profit, then adds back non-cash charges and subtracts capital expenditures and working-capital investment.

Compact formula logic: FCFF is commonly framed as EBIT after tax plus depreciation and amortization, minus capital expenditures and increases in working capital. Another cash-flow-statement path can start from operating cash flow, add back after-tax interest, and subtract capital expenditures.

FCFE is more directly affected by the financing path. A common formula path starts with net income, adds back non-cash charges, subtracts capital expenditures and working-capital investment, then adds net borrowing or subtracts net debt repayment.

Compact formula logic: FCFE is commonly framed as net income plus depreciation and amortization, minus capital expenditures and increases in working capital, plus net borrowing. Net borrowing means debt issued minus debt repaid, so net debt repayment reduces FCFE.

Interest treatment is one reason the two measures can be confused. Interest expense is already reflected in net income and operating cash flow, but FCFF often adjusts for after-tax interest to move back toward a pre-financing firm-level view. FCFE keeps the shareholder-level effect of the financing structure.

Same-Company Example: Firm Value vs Equity Cash Flow

Consider a hypothetical company with operating cash flow of 120, capital expenditures of 40, and after-tax interest of 6. If the company also repays 20 of debt during the period, the operating base can look healthy while the equity-holder cash-flow lens changes materially.

| Step | FCFF Lens | FCFE Lens |

|---|---|---|

| Operating cash flow | 120 | 120 |

| Capital expenditures | -40 | -40 |

| After-tax interest adjustment | +6 | Already reflected in shareholder-level cash flow |

| Net debt repayment | Not deducted in the firm-level lens | -20 |

| Illustrative cash-flow result | 86 | 60 |

The example does not show that FCFF is better than FCFE. It shows that the two measures answer different questions. FCFF is asking what cash flow the firm can support before financing claims are separated. FCFE is asking what cash flow remains for equity holders after debt effects.

Common FCFF and FCFE Confusion Traps

Trap 1: Treating FCFF and FCFE as interchangeable. They are not interchangeable because one is a firm-level measure and the other is an equity-holder measure.

Trap 2: Pairing FCFF with the cost of equity. FCFF normally belongs with WACC because it represents cash flow available to the whole capital structure.

Trap 3: Pairing FCFE with WACC. FCFE normally belongs with the cost of equity because it represents cash flow available to common equity holders.

Trap 4: Assuming the larger number is the better metric. A larger FCFF or FCFE number does not automatically mean a better company, safer stock, or stronger valuation case.

Trap 5: Ignoring debt movement inside FCFE. Debt issuance can increase FCFE, while debt repayment can reduce it. That movement can reflect financing activity rather than improved operating quality.

When FCFF vs FCFE Can Mislead

FCFF can be useful when comparing companies with different capital structures, but it can still mislead if operating cash flow is temporarily inflated, working-capital movement is unusual, capital expenditure needs are understated, or the WACC assumption is too optimistic.

FCFE can be useful when the investor wants a direct equity-holder cash-flow lens, but it can become volatile when debt issuance, debt repayment, refinancing, or leverage changes dominate the period. A high FCFE figure may partly reflect borrowing rather than durable operating strength.

Limitation: FCFF and FCFE are valuation inputs, not complete investment conclusions. Neither measure proves earnings quality, balance-sheet safety, competitive advantage, management quality, or future stock return.

FCFF vs FCFE in a DCF Model

In a discounted cash flow model, the cash-flow measure and discount rate need to describe the same claim. FCFF points toward firm value, so it is usually discounted with WACC. FCFE points toward equity value, so it is usually discounted with the cost of equity.

The model can break logically when those pairings are mixed. Discounting FCFF at the cost of equity can over-focus on shareholder return while still using firm-level cash flow. Discounting FCFE at WACC can treat shareholder-level cash flow as if it belongs to all capital providers.

Related Valuation Concepts

FCFF and FCFE become easier to separate once the surrounding valuation terms are clear. Free cash flow defines the broader cash-flow family. Enterprise value explains the firm-level valuation base. Equity value explains the shareholder claim after debt and other claims. Discounted cash flow explains how future cash flows are converted into present value.

The practical boundary is simple: use FCFF when the valuation starts with the whole firm, and use FCFE when the valuation starts with cash flow available to common equity holders.

FAQ

What is the main difference between FCFF and FCFE?

FCFF measures cash flow available to all capital providers before financing effects, while FCFE measures cash flow available to common equity holders after debt-related financing effects.

Is FCFF better than FCFE?

FCFF is not automatically better than FCFE. FCFF is better suited to firm-level valuation, while FCFE is better suited to equity-holder cash-flow valuation. The correct choice depends on the valuation question.

Why is FCFF usually discounted using WACC?

FCFF is usually discounted using WACC because it represents cash flow available to the full capital structure, including debt and equity providers.

Why is FCFE usually discounted using cost of equity?

FCFE is usually discounted using cost of equity because it represents cash flow remaining for common equity holders after debt-related financing effects.

Can FCFE be higher because of borrowing?

Yes. FCFE can increase when a company raises more debt than it repays. That does not automatically mean operating quality improved, because the increase may come from financing activity.