Free cash flow to equity is the cash flow available to common shareholders after operating needs, reinvestment, and debt-financing effects are included.

Direct definition: FCFE measures the cash that could theoretically be available to common equity holders after the company funds operations, maintains or grows its asset base, and accounts for net borrowing. It is also called levered free cash flow because it reflects debt issuance, debt repayment, and interest-bearing financing decisions.

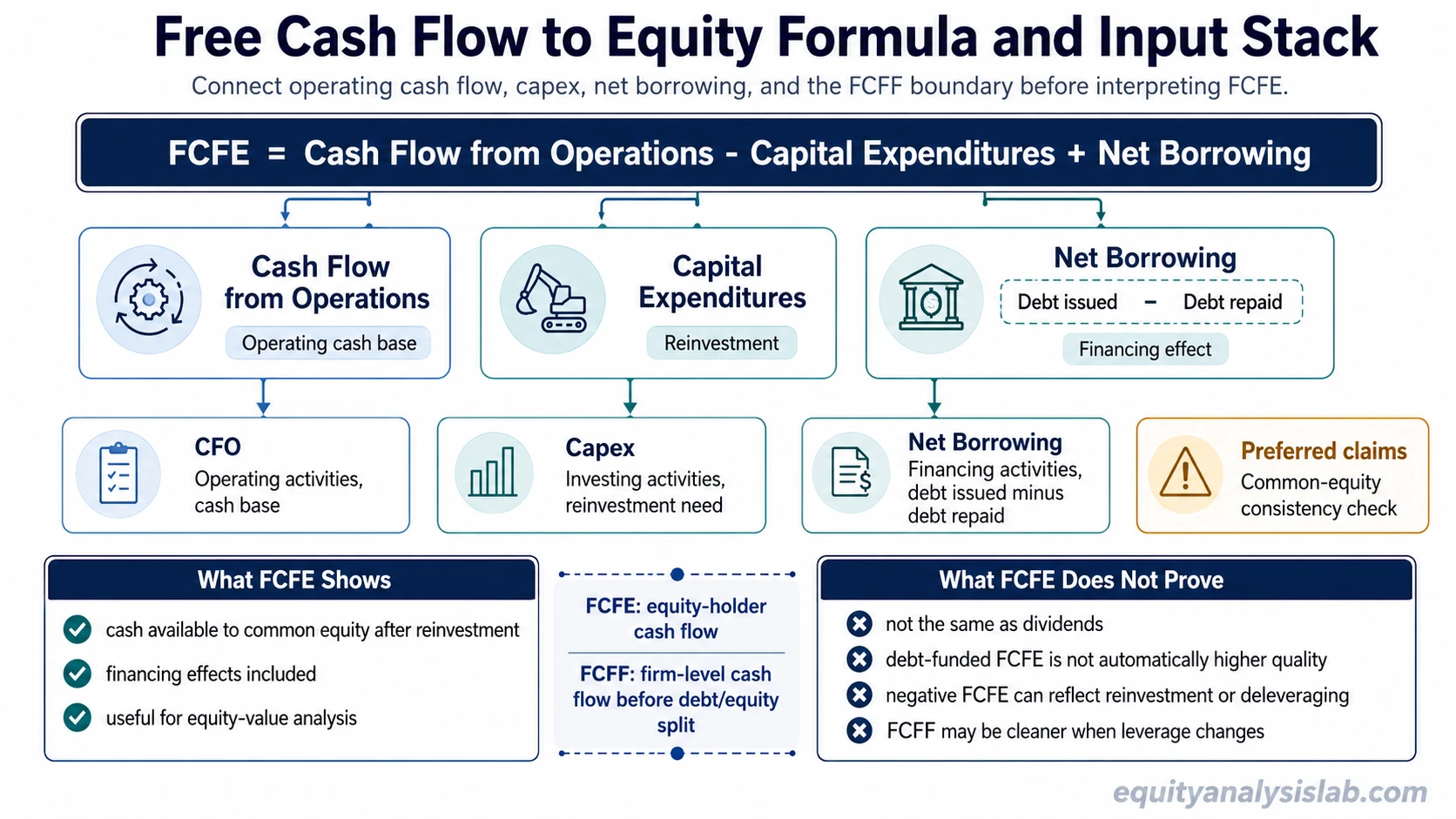

- FCFE is equity-holder cash flow, not total firm cash flow.

- Net borrowing can raise FCFE even when operating cash quality has not improved.

- Debt repayment can reduce FCFE even when the underlying business remains healthy.

- Negative FCFE can reflect reinvestment or deleveraging, not only distress.

FCFE is narrower than broader free cash flow because it focuses on what remains for equity holders after financing effects. It also differs from FCFF, which looks at cash flow available to all capital providers before separating debt and equity claims.

What Free Cash Flow to Equity Means

FCFE answers a specific valuation question: how much cash flow belongs to common shareholders after the business has paid for operating activity, reinvestment, and net debt financing. That makes it useful in equity valuation, dividend capacity analysis, buyback context, and shareholder cash-flow interpretation.

A positive FCFE number does not automatically mean the company is distributing cash to shareholders. Dividends and buybacks are management decisions. FCFE estimates cash capacity after the required operating and financing adjustments.

The financing layer is the main distinction. A company may report higher FCFE because it issued debt, not because the core business generated more cash. Another company may report lower FCFE because it repaid debt or invested heavily, not because the operating model failed.

Free Cash Flow to Equity Formula

Cash-flow-statement formula:

FCFE = Cash Flow from Operations - Capital Expenditures + Net Borrowing

Net-income formula:

FCFE = Net Income + Depreciation and Amortization - Capital Expenditures - Increase in Net Working Capital + Net Borrowing

The cash-flow-statement formula often reduces reconciliation work because cash flow from operations already reflects net income, non-cash charges, and working-capital movements. Capital expenditures are then subtracted because they represent reinvestment in the asset base. Net borrowing is added because debt issuance increases cash available to equity holders, while debt repayment reduces it.

Net borrowing is normally calculated as debt issued minus debt repaid. If the company issued $30 million of debt and repaid $10 million, net borrowing is $20 million. If the company repaid more debt than it issued, net borrowing becomes negative.

Preferred claim nuance: When FCFE is calculated for common shareholders, preferred dividends or other preferred claims may need to be subtracted if they are not already captured in the starting point. The key is claim consistency: common-equity cash flow should not include cash that belongs to preferred holders.

Where FCFE Inputs Come From

The formula is simple, but the interpretation depends on where each input comes from and what changed during the period. The same FCFE number can mean different things depending on whether it came from stronger cash conversion, lower reinvestment, new borrowing, or delayed debt repayment.

| Input | Statement location | Why it changes FCFE | Common investor mistake |

|---|---|---|---|

| Cash flow from operations | Cash flow statement, operating activities | Raises or lowers the operating cash base before reinvestment and financing adjustments. | Assuming higher CFO always means better quality without checking working-capital timing. |

| Capital expenditures | Cash flow statement, investing activities | Reduces FCFE because cash is reinvested into property, equipment, software, or other long-term assets. | Treating lower capex as automatically positive when it may reflect underinvestment. |

| Net borrowing | Cash flow statement, financing activities | Increases FCFE when debt issuance exceeds debt repayment and reduces FCFE when repayments exceed issuance. | Reading debt-funded FCFE as operating improvement. |

| Debt repayment / debt issuance | Cash flow statement, financing activities | Debt issuance adds cash available to equity holders; debt repayment absorbs cash before equity holders can use it. | Penalizing a company for lower FCFE when the decline came from deleveraging. |

| Working capital changes | Cash flow statement, operating activities, often linked to balance sheet movements | Receivables, inventory, payables, and other working-capital items can pull cash into or out of operations. | Ignoring temporary timing effects that can make one period look unusually strong or weak. |

| Preferred dividends or preferred claims | Financing notes, income statement presentation, or equity section depending on reporting format | May reduce cash truly available to common shareholders if preferred holders have prior claims. | Mixing common-equity FCFE with cash flows that belong to preferred investors. |

| Shareholder distributions | Cash flow statement, financing activities | Dividends and buybacks show how cash was used, not the core FCFE formula itself. | Assuming FCFE equals dividends or buybacks instead of treating distributions as capital-allocation decisions. |

FCFE vs FCFF

FCFE: cash flow available to common equity holders after debt-financing effects.

FCFF: cash flow available to all capital providers before separating debt and equity claims.

FCFE is commonly used when the valuation target is equity value. FCFF is commonly used when the valuation starts from enterprise value because it measures cash flow before allocating value between debt and equity holders.

The FCFE approach can work well when capital structure is stable and debt policy is understandable. FCFF may be more stable when leverage is changing quickly, debt repayments are lumpy, or net borrowing is large enough to distort the equity-holder cash-flow picture.

| Question | FCFE | FCFF |

|---|---|---|

| Whose cash flow is measured? | Common equity holders | All capital providers |

| Debt financing included? | Yes, through net borrowing | No, before debt and equity allocation |

| Typical valuation output | Equity value | Enterprise value before net debt adjustments |

| Most useful when | Leverage is stable and equity cash flow is the focus | Capital structure is unstable or firm-level cash flow is cleaner |

How Investors Interpret FCFE

FCFE is useful because shareholders are residual claimants. After operating costs, reinvestment, lenders, and preferred claims are considered, common shareholders are left with the remaining cash-flow capacity. That makes FCFE a direct input for equity-focused valuation work.

The number should be read in layers. First, check whether cash flow from operations is recurring or temporarily helped by working-capital timing. Second, check whether capital expenditures are maintenance needs, growth investment, or temporarily suppressed spending. Third, separate cash generated by the business from cash added through debt issuance.

Interpretation sequence:

- Start with operating cash generation.

- Subtract reinvestment needs.

- Identify whether debt issuance or repayment changed the result.

- Compare FCFE with dividends, buybacks, leverage trends, and reinvestment requirements.

- Use FCFF instead when debt policy makes FCFE too noisy.

A company with steady FCFE, modest leverage, and disciplined reinvestment may have more flexibility for dividends, buybacks, or balance-sheet strengthening. A company with high FCFE driven mostly by borrowing gives a weaker signal because financing activity can make shareholder cash flow look better than the operating business alone would support.

FCFE Limitations

FCFE is not a standalone verdict on business quality. It can be distorted by financing decisions, reinvestment timing, working-capital swings, and capital-structure changes.

- Net borrowing can inflate FCFE: debt issuance adds cash to the formula even when the operating business has not improved.

- Debt repayment can depress FCFE: deleveraging may reduce FCFE in the current period while improving balance-sheet risk.

- Negative FCFE is not always a failure signal: it can reflect heavy reinvestment, working-capital investment, or debt repayment.

- Unstable leverage reduces comparability: two companies with similar operations can report very different FCFE because their debt policies differ.

- Capital-light and capital-intensive firms should not be compared casually: capex needs can change the meaning of shareholder cash-flow capacity.

The strongest FCFE analysis separates operating cash quality from financing effects. A higher FCFE number is more useful when it comes from durable cash generation rather than short-term borrowing.

Simple FCFE Example

A hypothetical company reports $120 million in cash flow from operations, spends $40 million on capital expenditures, issues $30 million of debt, and repays $10 million of debt.

Net borrowing = $30 million - $10 million = $20 million

FCFE = $120 million - $40 million + $20 million = $100 million

The first layer is the cash generated after reinvestment: $120 million of operating cash flow minus $40 million of capex equals $80 million. The second layer is financing: $20 million of net borrowing raises FCFE to $100 million.

The interpretation is not simply that shareholders received $100 million of higher-quality cash. The company generated $80 million after capex and added another $20 million through net debt financing. If the same company had repaid $20 million more debt than it issued, FCFE would fall to $60 million even though the operating and capex numbers were unchanged.

| Scenario | CFO | Capex | Net borrowing | FCFE | Interpretation |

|---|---|---|---|---|---|

| Debt issuance exceeds repayment | $120m | $40m | +$20m | $100m | FCFE is helped by financing activity. |

| Debt repayment exceeds issuance | $120m | $40m | -$20m | $60m | FCFE is reduced by deleveraging. |

Related Cash-Flow and Valuation Concepts

Broader cash-flow base: Free cash flow helps separate cash generation from accounting profit before narrowing the analysis to equity-holder cash flow.

Equity valuation output: Equity value is the relevant valuation destination when FCFE is discounted directly to common shareholders.

Firm-level boundary: FCFF becomes more useful when the investor wants a capital-structure-neutral view or when leverage changes make FCFE too volatile.

FAQ

Is FCFE the same as free cash flow?

No. Free cash flow is often used as a broader cash-flow concept. FCFE is narrower because it focuses on cash available to common equity holders after reinvestment and debt-financing effects.

Why can FCFE rise when operating quality does not improve?

FCFE can rise because net borrowing increased. New debt adds cash to the formula, so investors need to separate operating cash generation from financing activity before reading the result as an improvement.

Can FCFE be negative for a healthy company?

Yes. FCFE can be negative when a company reinvests heavily, builds working capital, or repays debt. The interpretation depends on whether the cash use supports growth, reduces risk, or reflects operating pressure.

Is FCFE the same as dividends?

No. FCFE estimates cash flow available to common shareholders. Dividends are a distribution decision. A company can have positive FCFE and still retain cash, repay debt, buy back shares, or invest more heavily.