Weighted average cost of capital, or WACC, is the blended rate a company is expected to pay to its capital providers, weighted by the mix of equity, debt, and other financing claims.

Definition: WACC combines the estimated cost of equity and the after-tax cost of debt into one company-level capital-cost rate. In valuation, it is commonly used as a discount-rate input when the cash flows being valued, the capital structure assumption, and the risk profile all match the rate being applied.

The blended rate is not a direct measure of business quality, stock attractiveness, or expected share-price return. It is a required-return estimate for the capital used to finance a business. The same number can mean different things when the business model, financing mix, tax treatment, and risk of the cash-flow stream change.

Key Points

- WACC blends the cost of equity and after-tax cost of debt according to capital structure.

- It is commonly used as a discount-rate or hurdle-rate input in valuation and capital budgeting.

- The formula is only as useful as the assumptions behind equity cost, debt cost, tax rate, and capital weights.

- WACC should not be used as a standalone investment screen or proof of company quality.

What Weighted Average Cost of Capital Means

WACC estimates the average return required by the providers of a company’s capital. Equity holders require compensation for ownership risk. Lenders require interest for providing debt capital. Because interest expense is often tax deductible, the debt portion is usually measured after tax.

The result is a blended rate that connects financing structure with valuation. A company funded mostly by equity will be more sensitive to the estimated cost of equity. A company with meaningful debt will also reflect borrowing cost, tax treatment, and the proportion of debt in total capital.

In practical valuation work, WACC is usually tied to enterprise-level cash flows. That makes the boundary important: a rate built from debt and equity capital should be matched with cash flows available to both debt and equity providers, not with equity-only cash flows unless the valuation frame has been adjusted.

WACC Formula and Inputs

The standard WACC formula is:

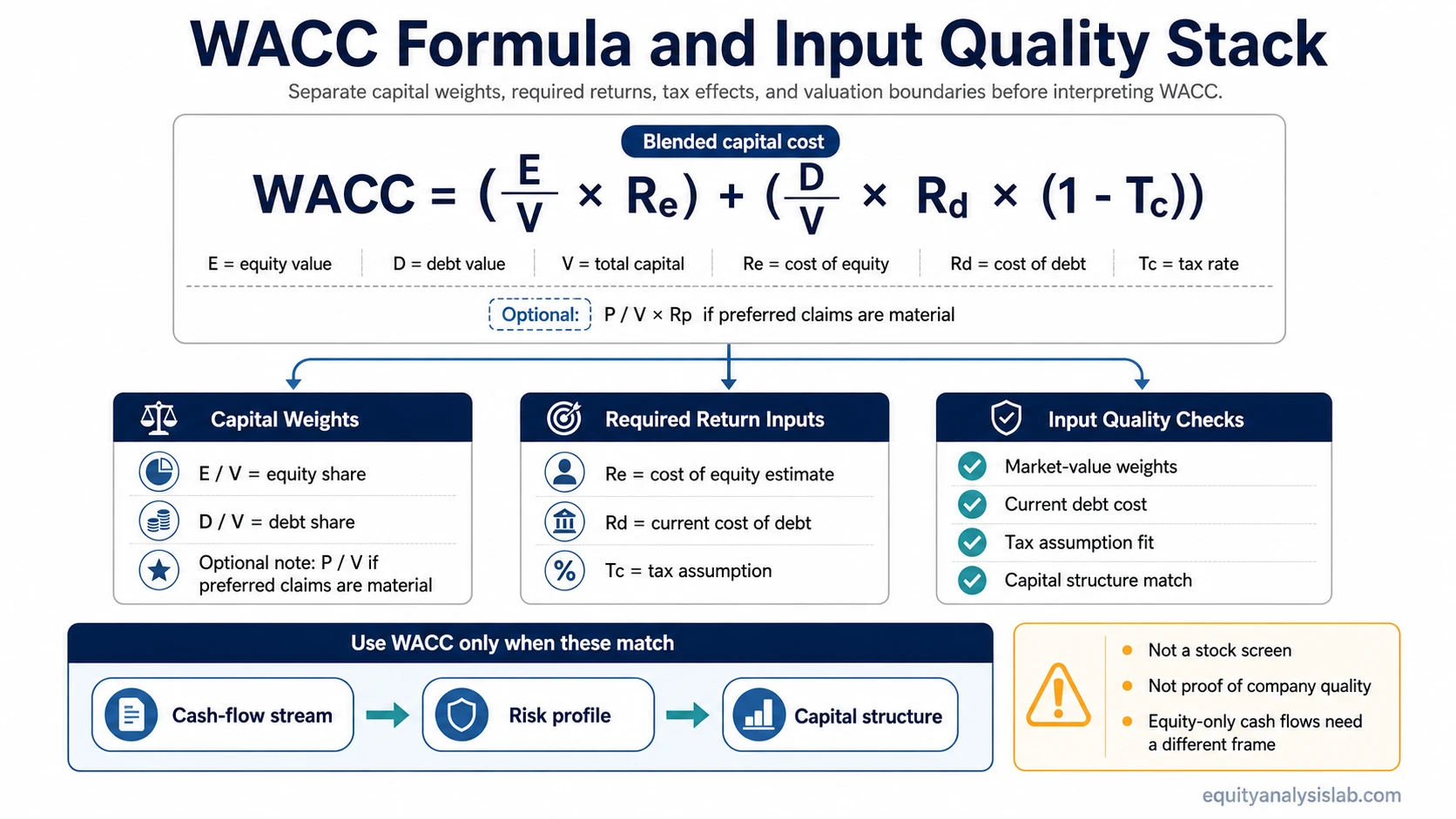

WACC = (E / V × Re) + (D / V × Rd × (1 – Tc))

In this formula, equity and debt are weighted by their share of total capital. The cost of debt is adjusted for taxes because debt interest may reduce taxable income. If a company has preferred stock or other hybrid financing claims, a separate preferred component may be added when it is material.

| Input | Meaning | Input quality check |

|---|---|---|

| E | Market value of equity | Use market value when the goal is an investor-facing capital-cost estimate, not a stale book-value shortcut. |

| D | Market value of debt | Debt value should reflect the financing claim being priced, especially when debt trades far from book value. |

| V | Total capital value, usually E + D | The denominator must match the included capital claims. If preferred stock is included, total capital should include it too. |

| Re | Cost of equity | This is an estimate, not an observable coupon. It is often estimated with the capital asset pricing model or another required-return method. |

| Rd | Cost of debt | This should reflect the company’s current borrowing cost or debt yield, not only historical interest expense. |

| Tc | Corporate tax rate | The tax adjustment should match the jurisdiction and tax assumptions used in the valuation. |

| P / Rp | Preferred stock value and preferred cost, if relevant | Use only when preferred or hybrid claims are material enough to affect the capital-cost estimate. |

When preferred stock is material, the expanded version can be written as:

WACC = (E / V × Re) + (D / V × Rd × (1 – Tc)) + (P / V × Rp)

How Investors Use WACC in Valuation

Investors most often use WACC as a discount-rate input. A higher WACC reduces the present value of future cash flows, all else equal. A lower WACC increases that present value, all else equal. The interpretation depends on whether the rate properly reflects the risk and financing structure behind those cash flows.

WACC can also act as a hurdle-rate reference. If a company evaluates a project, acquisition, or reinvestment plan, the expected return should be compared with a capital-cost rate that matches the risk of that decision. A mature core-business project may deserve a different rate than a speculative expansion, even if both sit inside the same company.

Illustrative scenario: A stable company may have one company-level WACC, but a new business line with uncertain demand can carry a higher risk profile than the legacy business. Using the same company-level WACC for both cash-flow streams can make the riskier project look more attractive than it really is. The stronger valuation test separates the cash-flow stream, the financing assumption, and the risk profile before selecting the rate.

When WACC Is the Right Lens

WACC works best when the valuation is focused on cash flows available to all capital providers. That is why it is often paired with enterprise-value frameworks, where both debt and equity claims matter.

| Question | Why it matters | Cleaner interpretation |

|---|---|---|

| Are the cash flows enterprise-level? | WACC blends debt and equity capital costs. | Use WACC when the cash flows are available to both debt and equity providers. |

| Does the risk profile match? | A company-wide rate can understate or overstate project-level risk. | Adjust the rate or use a separate project rate when the project is materially different from the business. |

| Is the capital structure stable enough? | The weights in the formula can change as debt, equity value, or financing plans change. | Use assumptions that match the expected financing structure, not only the latest balance-sheet snapshot. |

| Are market-value weights available? | Book values may not reflect investor-required returns. | Prefer market-value weights when estimating the current opportunity cost of capital. |

| Are special financing claims material? | Preferred stock, convertibles, and hybrid claims can change the capital stack. | Include material claims instead of forcing the company into a simple debt-and-equity formula. |

When WACC Can Mislead

Limitation: WACC can mislead when the rate does not match the cash flows being valued. A company-level WACC is not automatically valid for every project, segment, acquisition, or equity-only valuation.

One common mistake is applying WACC to equity cash flows. If the cash flow belongs only to common shareholders after debt costs, the discount rate usually needs to reflect the cost of equity rather than a blended debt-and-equity rate.

Another mistake is treating the cost of equity as precise. Unlike debt interest, cost of equity is estimated. Small changes in equity risk assumptions can change the final WACC enough to affect valuation conclusions.

WACC can also become unstable for distressed companies, highly leveraged firms, financial institutions, or businesses with rapidly changing financing needs. In those cases, debt cost, tax shields, capital weights, and equity risk may change at the same time.

Common WACC Mistakes

- Using book-value weights when the valuation requires market-value weights.

- Assuming a lower WACC automatically means a better investment.

- Applying one company-wide WACC to projects with different risk profiles.

- Ignoring preferred stock, convertibles, leases, or other material financing claims.

- Using WACC as a stock screen instead of a valuation assumption.

WACC Compared With Related Concepts

WACC is one expression of cost of capital, but it is not the whole concept. Cost of capital can refer broadly to the required return on different financing sources, while WACC specifically blends those sources by capital structure.

| Concept | How it differs from WACC | Boundary |

|---|---|---|

| Cost of capital | Broader term for the return required by capital providers. | WACC is one weighted company-level version of that broader idea. |

| CAPM | A method often used to estimate the cost of equity. | CAPM can feed one WACC input, but it is not the full WACC formula. |

| Discount rate | The rate used to convert future cash flows into present value. | WACC can be a discount rate when the valuation frame fits. |

| Required return | The return an investor or capital provider demands for risk. | WACC blends required returns across financing sources. |

| DCF | A valuation method based on discounted future cash flows. | WACC may be used inside a DCF, but WACC is not the DCF model itself. |

FAQ

Is WACC the same as cost of capital?

No. WACC is one weighted version of cost of capital. Cost of capital is the broader idea, while WACC blends the estimated cost of equity and after-tax cost of debt according to capital structure.

Is a lower WACC always better?

No. A lower WACC can increase valuation mathematically, but it does not automatically prove that a company is higher quality or that an investment is attractive. The rate must be judged alongside risk, cash-flow quality, capital structure, and assumptions.

When should investors not use WACC?

WACC can be the wrong tool when the cash flows belong only to equity holders, when a project has a different risk profile from the company, when the capital structure is unstable, or when unusual financing claims make the standard formula incomplete.