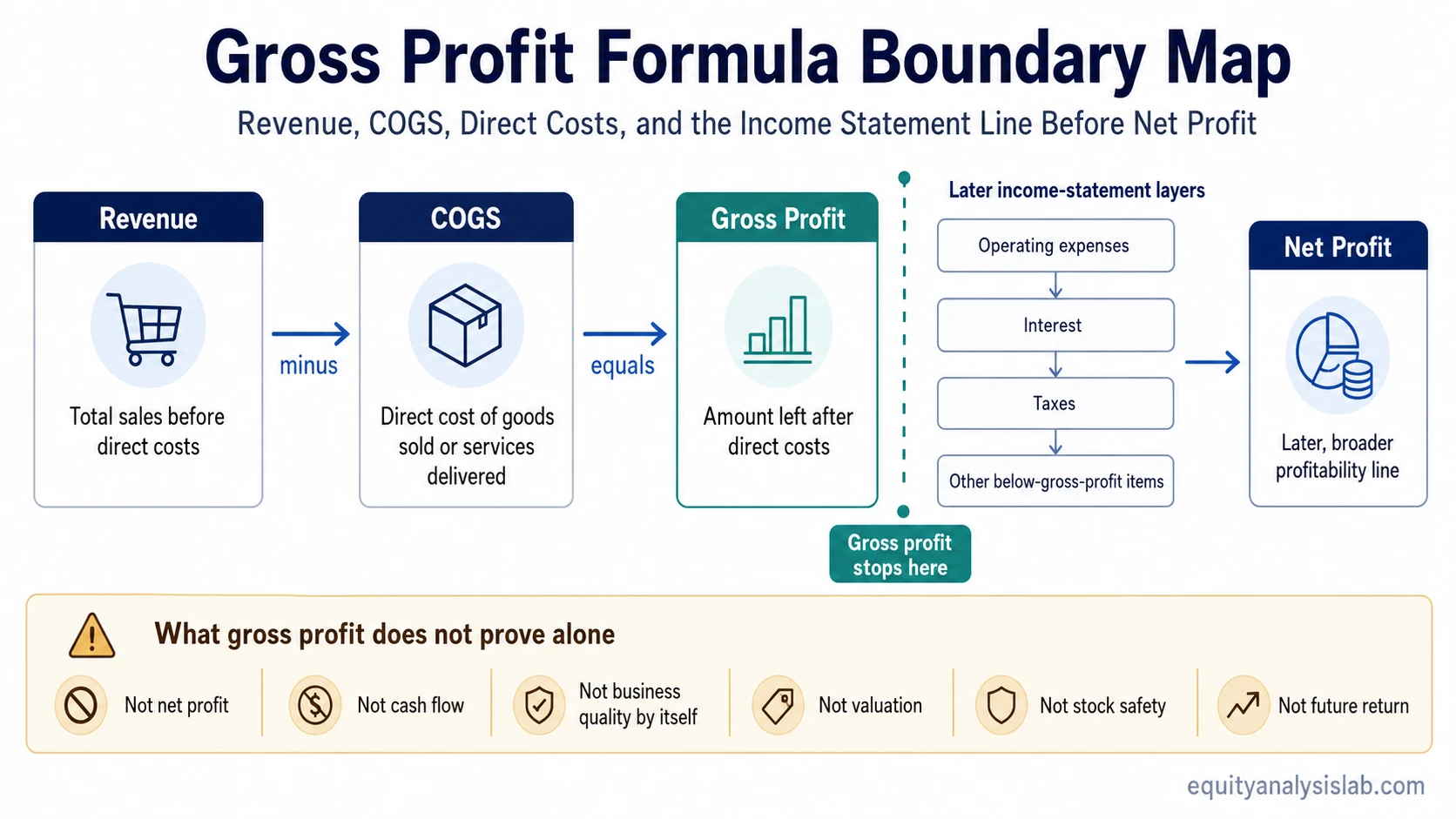

Gross profit is revenue minus cost of goods sold, or COGS. It shows how much profit remains after the direct costs of producing or delivering a product or service, before operating expenses, interest, taxes, and other later income-statement items are included.

Gross profit = Revenue – Cost of goods sold

As an investor-facing accounting line, gross profit is useful because it isolates the direct-cost economics of the business before the rest of the cost structure enters the picture. It is not the same as net profit, cash flow, business quality, valuation, or future stock return.

What gross profit means

Gross profit measures the amount left after a company subtracts costs directly tied to producing or delivering what it sells. For a product company, that may include materials, production labor, and manufacturing-related costs. For a service or software company, the exact cost categories can differ, but the same boundary matters: gross profit comes after direct delivery costs and before broader operating costs.

That placement makes gross profit an early profitability line on the income statement. It appears before selling, general and administrative expenses, research and development, depreciation treatment where reported separately, interest expense, taxes, and non-operating items.

Gross profit formula

The basic formula is:

Gross profit = Revenue – Cost of goods sold

If a company reports revenue of 100 and cost of goods sold of 60, gross profit is 40. That 40 is not net income. The company still needs to subtract operating expenses, interest, taxes, and any other relevant items before reaching the final profit line.

What counts as COGS

Cost of goods sold usually includes costs that are directly connected to producing, acquiring, or delivering the goods or services sold during the period. The exact label can appear as cost of goods sold, cost of sales, cost of revenue, or a similar line depending on the company and industry.

The important boundary is direct cost. Gross profit does not normally include every expense needed to run the company. Sales teams, headquarters costs, corporate salaries, financing costs, taxes, and many other items typically appear below gross profit.

Gross profit vs gross margin

Gross profit is a currency amount. Gross margin is a percentage. A company can report gross profit in dollars, euros, or another reporting currency, while gross margin percentage shows gross profit as a share of revenue.

Gross profit: the amount left after COGS.

Gross margin: gross profit divided by revenue, usually shown as a percentage.

This distinction matters because two companies can report very different gross profit amounts simply because one is larger. Gross margin helps compare direct-cost profitability across companies or periods, while gross profit shows the absolute amount available before later expense layers.

Gross profit vs net profit

Gross profit stops after direct costs. Net profit comes much later. Net profit reflects the impact of operating expenses, interest, taxes, and other below-gross-profit items, so it gives a broader view of final accounting profitability.

A company can have positive gross profit and still report a net loss if operating expenses, financing costs, taxes, or other charges exceed the amount left after COGS. That is why gross profit should not be read as complete profitability.

How investors use gross profit

Investors can use gross profit to separate direct business economics from the rest of the income statement. It helps answer a narrow question: after the company delivers what it sells, how much remains before broader overhead and financing costs?

The number is most useful when read with revenue trends, gross margin, operating expenses, cash flow, and the company’s business model. Rising gross profit can reflect higher sales, better direct-cost control, price increases, product mix changes, or scale effects. It can also grow while margins weaken, if revenue rises faster than direct-cost pressure but not enough to preserve percentage profitability.

What gross profit does not prove

Gross profit does not prove that a company generates cash, earns attractive net income, has a high-quality business model, trades below intrinsic value, or offers a safe future return. It is one income-statement line, not a complete investment conclusion.

The common mistake is treating gross profit as if it answers questions that belong to later analysis. Cash conversion, operating leverage, reinvestment needs, debt costs, taxes, dilution, valuation, and competitive durability all require separate review.

Gross profit compared with nearby profit measures

| Measure | What it subtracts | What it helps interpret | What it does not prove |

|---|---|---|---|

| Gross profit | Cost of goods sold or direct delivery costs | Direct-cost economics before broader expenses | Net profitability, cash flow, valuation, or stock safety |

| Gross margin | Uses gross profit as a percentage of revenue | Direct-cost profitability relative to sales | Final profit quality or investment attractiveness |

| Operating profit | Operating expenses after gross profit | Profitability after core operating costs | Final profit after interest, taxes, and non-operating items |

| Net profit | Broader expenses, financing, taxes, and other items | Final accounting profit after most expense layers | Cash flow quality or future stock return by itself |

Common mistakes when reading gross profit

Confusing amount with percentage. Gross profit is the amount. Gross margin is the percentage relationship between that amount and revenue.

Stopping before later expenses. Positive gross profit does not mean the company is profitable after operating expenses, interest, and taxes.

Treating the line as a stock signal. Gross profit can support company analysis, but it does not tell an investor whether a stock is undervalued, safe, or likely to produce a future return.

FAQ

What is gross profit?

Gross profit is revenue minus cost of goods sold. It shows the amount left after direct production or delivery costs, before operating expenses, interest, taxes, and other later items.

What is the gross profit formula?

The formula is gross profit = revenue – cost of goods sold. Some companies may use labels such as cost of sales or cost of revenue, depending on their reporting format.

Is gross profit the same as gross margin?

No. Gross profit is a currency amount. Gross margin is gross profit divided by revenue and expressed as a percentage.

Does gross profit show net profit?

No. Net profit includes more expense layers than gross profit, including operating expenses, interest, taxes, and other items that appear later in the income statement.