Lifetime value is the estimated revenue, gross profit, or contribution a customer may generate over the full customer relationship. For investors, lifetime value is useful only when the assumptions behind retention, churn, margin, acquisition cost, and customer behavior are credible.

Definition: Lifetime value, often shortened to LTV or customer lifetime value, estimates what a customer is worth over the expected life of the relationship. The metric can be built on revenue, gross profit, contribution margin, or discounted cash-flow logic, so the version being used matters as much as the headline number.

Key Points

- Lifetime value measures expected customer economics over a relationship, not the value of the whole company.

- Revenue-based LTV can look stronger than profit-based LTV because it may ignore gross margin, servicing cost, or cash conversion.

- LTV becomes more useful when retention, churn, acquisition cost, cohort quality, and expansion revenue are visible.

- A high LTV estimate does not prove business quality unless the inputs are durable and the company can acquire customers at an acceptable cost.

What Lifetime Value Means

Lifetime value answers a narrow customer-economics question: how much economic value can one customer relationship produce before that relationship ends or becomes uneconomic?

The term is common in subscription, software, app, ecommerce, and recurring-revenue businesses because those models depend on customers staying long enough to justify acquisition and service costs. In fundamental analysis, the same idea is useful as a business-quality input because it helps investors judge whether customer relationships are durable, profitable, and supported by evidence.

The important boundary is that LTV is not a standalone investment signal. The number can change sharply if churn rises, margins compress, acquisition costs increase, or newer customer cohorts behave differently from older cohorts.

How Lifetime Value Is Calculated

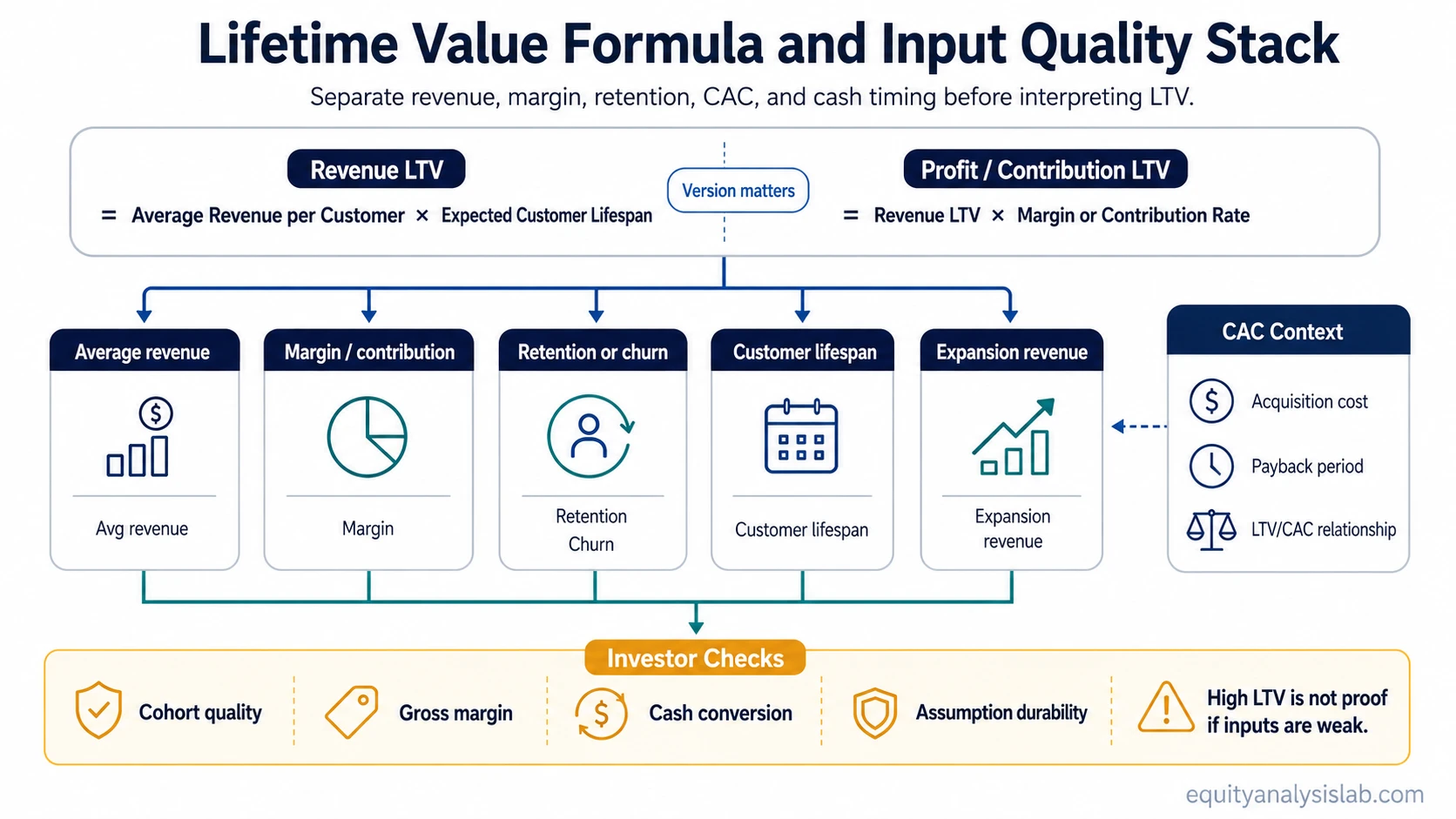

There is no single universal lifetime value formula. The simplest version estimates customer revenue over time. Stronger versions adjust for margin, churn, retention, acquisition cost, and the time value of money.

Simple revenue view: LTV can be estimated as average revenue per customer multiplied by expected customer lifespan.

Profit or contribution view: LTV can adjust that revenue by gross margin or contribution margin so the estimate is closer to economic value rather than sales volume.

Investor view: The most useful version connects revenue, margin, retention, acquisition cost, and cash conversion without hiding weak assumptions inside a single attractive number.

A subscription-style shortcut often connects average customer revenue with churn. That can be useful for orientation, but it can overstate quality when churn is backward-looking, margin is weak, or customer acquisition costs are rising.

Which Inputs Make Lifetime Value Useful

Lifetime value is only as reliable as its inputs. Investors should focus less on the headline LTV number and more on the assumptions that create it.

| Input | What it means | Why investors care | What can distort it |

|---|---|---|---|

| Average revenue per customer | The revenue a typical customer generates over a period. | It shows the revenue base used in the LTV estimate. | It can be inflated by a small number of large customers or by temporary upsells. |

| Gross margin or contribution margin | The portion of revenue left after direct costs or customer-level costs. | It separates sales volume from economic contribution. | Revenue LTV can look strong even when margin-adjusted LTV is weak. |

| Churn / retention | The rate at which customers leave or remain active. | Retention drives the length and durability of the customer relationship. | Older cohorts may retain better than newer cohorts, making blended retention misleading. |

| Customer lifespan | The expected length of the customer relationship. | Longer expected relationships usually raise estimated LTV. | Small changes in lifespan assumptions can create large changes in LTV. |

| Acquisition cost | The cost required to acquire a customer. | LTV has limited meaning if the company must spend too much to acquire the customer. | Paid marketing inflation, channel saturation, or sales-force expansion can raise acquisition cost over time. |

| Discount rate or time value assumption | The adjustment for cash received later rather than today. | It matters when expected customer value arrives over many years. | Ignoring time value can make distant customer cash flows look too valuable. |

| Expansion revenue / net revenue retention | The additional revenue generated from existing customers over time. | Expansion can make customer economics stronger when existing customers buy more. | Expansion assumptions can be overstated if net dollar retention is weak or deteriorating. |

Revenue LTV vs Profit or Contribution LTV

The cleanest distinction is whether lifetime value measures revenue or economic contribution. Revenue LTV answers how much sales volume a customer may produce. Profit or contribution LTV asks how much value remains after the costs needed to serve that customer.

That distinction matters because two companies can report similar customer revenue but have very different economics. One company may have high gross margins, low servicing costs, and stable retention. Another may have lower margins, heavy support costs, and customers that require constant discounts. The revenue LTV may look similar, but the shareholder value created by each customer can be very different.

Investor interpretation: When a company highlights LTV, check whether the metric is revenue-based, gross-profit-based, contribution-based, or cash-flow-based. A revenue-based number is usually less useful for investor analysis unless it is paired with margin, churn, and acquisition-cost evidence.

How Investors Should Interpret Lifetime Value

Investors should treat lifetime value as a lens for business quality, not as proof of quality. A credible LTV estimate can support the idea that a company has durable customer relationships, repeatable demand, and attractive unit economics. A weak LTV estimate can hide the opposite.

The strongest interpretation usually comes from connecting LTV with acquisition cost, retention, and margin. If a company can acquire customers efficiently, keep them for a long time, and earn high contribution from each relationship, LTV can support a stronger business-quality case. If acquisition costs keep rising or retention weakens, the LTV estimate may become less reliable even if the reported number still looks high.

This is why LTV should be read beside customer acquisition cost rather than in isolation. Customer value matters only if the cost of acquiring and retaining that value does not consume the economics.

When Lifetime Value Can Mislead

Lifetime value can mislead when the metric compresses uncertain assumptions into one clean-looking number. The risk is highest when a company presents LTV as evidence of customer quality without showing the underlying cohort, churn, margin, or acquisition-cost pattern.

Limitation: LTV can overstate business quality when churn is understated, gross margin is ignored, acquisition cost is excluded, payback periods are too long, expansion revenue is assumed without evidence, newer customer cohorts are weaker than older cohorts, or revenue LTV is used when investors need profit or cash-flow contribution.

Illustrative scenario: A subscription company may report high LTV because customers appear to stay for years. The number becomes less convincing if gross margin is low, newer cohorts churn faster, or the company must keep spending more to acquire the next customer. In that case, reported LTV may not translate into durable shareholder value.

The common mistake is reading a high LTV estimate as a complete answer. It is only the starting point for a better question: are the customer economics strong after margin, retention, acquisition cost, and cash timing are considered?

How Lifetime Value Connects to CAC, LTV/CAC, and Retention

Lifetime value becomes more useful when it is connected to the surrounding customer-economics system. CAC shows what the company spends to acquire the customer. Retention shows whether the customer relationship lasts long enough to matter. Expansion revenue shows whether existing customers become more valuable over time.

Use LTV for customer value: Lifetime value estimates the value side of the customer relationship.

Use CAC for acquisition efficiency: Customer acquisition cost shows the spending required to create that relationship.

Use LTV/CAC ratio for the relationship between the two: The ratio can help frame whether customer value appears high enough relative to acquisition cost, but it still depends on input quality.

Use retention metrics for durability: Retention and expansion metrics show whether the customer value is likely to persist.

For broader company analysis, LTV belongs inside unit economics. It is one part of the customer-level model, alongside pricing, cost to serve, retention, acquisition efficiency, and cash conversion.

FAQ

Is lifetime value the same as customer lifetime value?

Usually, yes. Lifetime value, LTV, customer lifetime value, and CLV are often used to describe the expected value of a customer relationship over time. The exact meaning depends on whether the calculation uses revenue, gross profit, contribution margin, or discounted cash-flow logic.

Is lifetime value based on revenue or profit?

It can be based on either. Revenue LTV estimates customer sales over time, while profit or contribution LTV adjusts for margin and customer-level costs. For investor analysis, profit or contribution-based LTV is usually more informative than a revenue-only estimate.

Why can lifetime value mislead investors?

Lifetime value can mislead investors when churn, margin, acquisition cost, payback period, or cohort quality is not visible. A high LTV estimate may look attractive even when the company spends too much to acquire customers or earns too little contribution from each relationship.

How does lifetime value connect to CAC?

Lifetime value estimates the value of a customer relationship, while CAC estimates the cost of acquiring that customer. The two metrics should be interpreted together because high customer value has limited meaning if acquisition cost consumes the economic benefit.